Does the bank check the apartment when applying for a mortgage?

Content

Banks organize only a minimal verification of documents; the buyer will have to take care of the legal purity of the transaction on his own. Before executing a mortgage agreement, the lender is presented with documents that he studies:

- Preliminary purchase and sale agreement (PSA).

- Extract from the Unified State Register of Ownership of the seller.

- Technical passport.

- The document on the basis of which the seller acquired the right of ownership: an old deed of ownership, a certificate of inheritance, an agreement of exchange, rent or gift.

- Other documents depending on the situation: consent of the seller’s spouse for the sale, permission from the guardianship authority.

Important! The submitted documents are checked by the bank's lawyers. If everything is in order with them and the apartment is without encumbrances, the deal will be approved. It makes no difference to the lender whether the seller used capital to purchase the home, whether shares were allocated, or whether there are third parties who can lay claim to it.

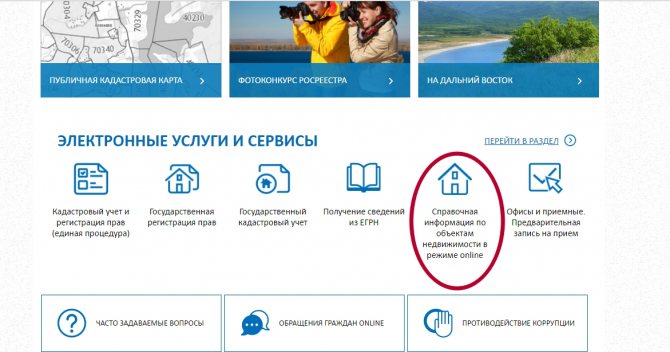

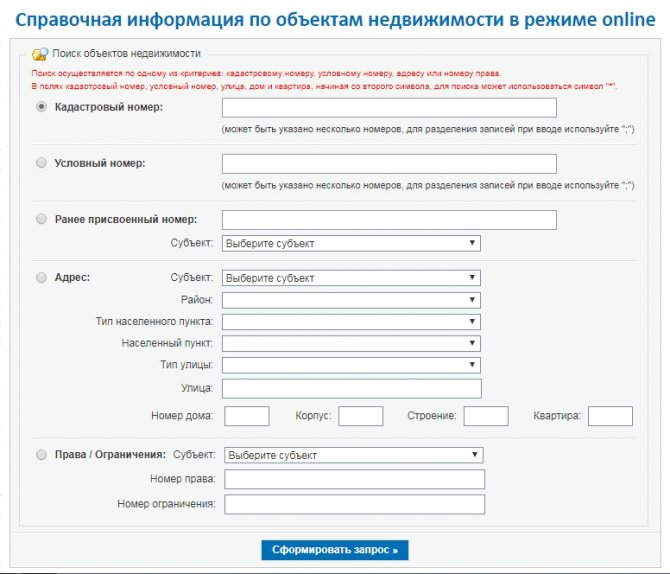

How to properly check an apartment in Rosreestr via the Internet: step-by-step instructions

To quickly check a property via the Internet, you must perform the following steps:

- Go to the official website of the Rosreestr body, scroll down a little and click on the inscription: “Reference information on real estate objects online.”

- On the page that opens, check the box, selecting the option for which you want to find information. The search is carried out by cadastral or conditional number, apartment address or license number. Click the “Generate request” button.

After this, information about the property will be released immediately.

How does Sberbank check an apartment for a secondary mortgage?

Sberbank and most other banks do not check the legal purity of the transaction. Usually only a few things become clear:

- Market value of real estate. An appraisal is performed to determine the size of the mortgage. Usually, no more than 80% of the price of the apartment is given, the rest must be paid by the borrower from the down payment.

- Submitted documents. Authenticity and absence of encumbrances are checked.

- Redevelopment. If they are not legalized, the mortgage will be refused.

- The seller's ownership of the home. This is confirmed by an extract from the Unified State Register.

In fact, the bank checks only superficially the mortgaged property; a detailed check of the owner (seller) is not carried out. He will not be asked for a certificate from a psychoneurological dispensary; they will not find out whether he is involved in the bankruptcy procedure, they will not check the history of the transfer of ownership.

How long does it take for the bank to verify an apartment's mortgage?

Let's consider how much the bank checks the apartment and the borrower for a mortgage:

- First, the borrower submits an application. The response is received within 5-30 minutes, the mortgage is pre-approved.

- The client brings his own documents to the lender, they are checked immediately. But it also happens that the answer is given only after 2-3 days.

- The property is located, the documents for it are submitted to the bank. The verification takes on average 5-7 days. At this time, the market value is also assessed.

- If everything is fine, the lender approves the transaction and the main contract is signed.

In total, obtaining a mortgage and purchasing real estate takes one month. On average, it takes 7 days to check the apartment itself.

What do banks not check when issuing a mortgage?

The bank checks the apartment with a mortgage only for obvious violations, in which case it cannot approve the transaction. For example, if the redevelopment is not legalized or the property is pledged. There are other disadvantages that lenders do not pay attention to:

- Debt for housing and communal services.

- Registered citizens.

- Condition of the house.

Let's look at how to check everything yourself.

Debts for housing and communal services

If the seller has utility debts, they will not be transferred to the new owner. But he may encounter problems: for example, resource-providing organizations do not care that the debt was not caused by the buyer, and his water or electricity supply may be turned off.

It’s easy to check an apartment for the absence of debts; just ask the seller for a certificate from the HOA or management company. The bank does not require it.

Registered citizens

Registration in an apartment gives the right of residence. If the seller does not register relatives before or after the transaction within the established time frame, the buyer will have to come to terms with their presence in the premises, or have the registration canceled through the court.

To check the absence of registered persons, you need to request an extract from the house register from the seller. It is registered in the HOA or management company.

Condition of the house

It is important for the bank that the house is not considered to be in disrepair: by law, mortgages on apartments in dilapidated buildings are prohibited, and besides, this is a risk for the lender. If the apartment is not in a dilapidated building, but the electricity is constantly cut off, pipes are leaking, there is no hot water supply, these are just troubles for the borrower: the bank is not interested in such shortcomings.

You can check the condition of the house yourself. There is no point in asking the seller: his goal is to sell the home, and he will only show the positive aspects. You can ask your neighbors or invite a specialist who understands the technical details and can identify possible shortcomings.

The best home in the eyes of the lender

When applying for a mortgage, Sberbank carefully assesses the borrower’s solvency and also thoroughly checks the collateral, most often a mortgaged apartment. If a citizen refuses to repay the debt, the organization will sell the apartment or house at auction to recover their money and lost profits. The lender is always interested in an easy and quick sale of the property.

What should new buildings be like?

Only a liquid object can become the object of mortgage lending.

In case of force majeure, the lender or owner must easily find a buyer. If a new building is purchased, Sberbank carefully studies the financial statements of the developer and issues accreditation only if it is highly reliable. Applications to purchase housing on a foundation pit are approved in rare cases. Banks prefer to deal with properties whose construction will soon be completed, or housing on the secondary market.

If one of the parties to the transaction is a developer, the manager of the lending department will ask to provide construction documentation - all permits, plans, projects. Sberbank lawyers will check the equity participation agreement for compliance with current legal standards. If the developer is on the list of accredited ones, information about him is posted on the bank’s official website and the subsidiary resource Dom Click.

Best Features of Resale Homes

When assessing the liquidity of living space in a secondary building, both the quality of construction and infrastructure are taken into account.

The foundation of the house, interfloor ceilings, height, and the need for major repairs play an important role. Important!

Sberbank is reluctant to lend to buyers of apartments in old panel and block buildings if they are not located in the very center of the city.

When you can’t do without a mortgage, it’s better not to buy real estate from the old housing stock. Don’t be surprised if the specialist asks for a certificate from the management company stating that the house will not be demolished or reconstructed in the near future.

And when the wear and tear of the building exceeds 60%, you shouldn’t even submit an application and ruin your credit history - it will be rejected. The expert will assess the location of the property, its condition, the size of the kitchen, and the need for repairs. If the property is located in the city center and does not require investment, Sberbank will be happy to take out a mortgage on the apartment.

According to the standards, the apartment must contain or be installed:

- pipes with hot and cold water supply;

- essential plumbing equipment;

- heating appliances depending on the type of heating network;

- high-quality glazing, doors, ceilings;

- electric or gas stove.

It is important that the apartment belongs to the category of residential premises, and not to commercial objects.

A refusal will come if you want to take out a mortgage for a basement, attic or equipped basement. Country real estate must have the infrastructure necessary for life - shops, a hospital, a kindergarten. You will not be able to get a mortgage if you plan to:

- purchasing a room in a communal apartment, with the exception of the purchase of the latter into the ownership of one buyer;

- purchase of housing for a small family;

- acquisition of a wooden structure;

- too cheap or expensive housing.

How do banks check a mortgage borrower?

Unlike checking an apartment for a mortgage, potential borrowers are given much more attention.

What does the bank do:

- Checks credit history. If it is not there at all, there is a chance that the mortgage will not be approved, or the minimum amount will be issued. If your credit history is damaged, the likelihood of a positive decision is close to zero. It is optimal when the client already had loans and all of them were repaid on time.

- Examines debt load. If there are outstanding loans, they are taken into account when calculating the total mortgage amount and monthly payments. Banks try to ensure that in total, no more than 50% of their salary is spent on repaying all loans from clients. If there are too many loans, your mortgage may be denied.

- Checks the salary level. It is confirmed by certificates, for individual entrepreneurs – by tax returns. The amount of monthly earnings is important in determining the mortgage amount.

- Client participation in bankruptcy proceedings. If he is already bankrupt or less than five years have passed since he was declared bankrupt, the mortgage will be denied.

Note! After submitting an application for a mortgage, the client undergoes a scoring check, which takes 5-10 minutes. The system analyzes his credit history and determines his reliability based on the completed questionnaire. After this, the potential borrower receives pre-approval. The final decision is announced only after a check by the security service, which examines not only the credit history, but also the submitted documents.

Legal advice: Some banks offer mortgages without proof of income. You shouldn’t count on this: the creditor will still make a request to the Pension Fund to find out whether the person pays insurance premiums. If not, this indicates that he is not officially employed. This system has been used instead of income verification for several years. But for a large amount they will still require income certificates and a certified copy of the work record book.

Decision to issue a mortgage loan

If all of the above verification stages have been successfully completed, then the mortgage application with the assessment results is transferred to the bank’s credit committee, which makes a decision.

It must be borne in mind that a positive decision to issue a mortgage has an “expiration date” and is valid for 90 days. If the borrower has not yet looked for a suitable property, then during these three months he needs to find it and also undergo a check of the collateral. Thus, the decision of the credit committee is not yet final.

The real estate for which the loan is issued will be carefully checked by the bank for the presence of encumbrances; its collateral value is determined and correlated with the loan amount, the amount of insurance is determined, and technical documentation is checked. And only after this the transaction date is set, and the applicant can breathe a sigh of relief.

Of course, in most cases, applicants already know what kind of real estate they need a loan for, so the time limit of 90 days is, in principle, not terrible. The process is also simplified if bank clients want to purchase housing in a new building and consult with the developer’s credit manager and contact partner banks.

But you need to keep in mind that even in this case, the verification of potential borrowers is also carried out carefully, and it should be approached with the utmost seriousness.

What happens if a mortgage real estate transaction is challenged?

Everything is simple here: the bank will lose the collateral, the borrower will lose the apartment. But this will not free you from debt obligations; the mortgage will have to be paid in any case.

During legal proceedings, the borrower can appeal Art. 302 of the Civil Code of the Russian Federation, according to which he is considered to be in good faith if he did not know and could not know about the circumstances under which the transaction could be challenged:

- The sudden appearance of heirs who did not have time to enter into inheritance.

- The property was sold under a power of attorney, which the principal canceled before the day of the transaction.

Important! Recently, courts have not canceled transactions, but obligated sellers to compensate the share of persons who challenge the contract. Buyers are left not only with housing, but also with frayed nerves due to lengthy legal proceedings.

How to check an apartment when applying for a mortgage yourself?

The buyer can check the property himself before purchasing with a mortgage, or contact a lawyer. If the transaction is accompanied by a specialist, the risks are minimized, so the second option is preferable.

There are a few things you can and should check before purchasing:

- Is the seller the owner of the property?

- Are there any encumbrances?

- Is the power of attorney valid?

- Does the seller's spouse have consent to the sale?

- Have you received permission from the guardianship authority to sell the child’s home?

- Are there third parties who can lay claim to the property?

- Are shares in the ownership allocated if the apartment was purchased with capital?

Let's look at the nuances in more detail.

Owner verification

You can check the owner by ordering an extended extract from the Unified State Register yourself. When ordering on the Rosreestr website, it will cost 350 rubles, and will be sent by email within three days after submitting the application.

The statement will include information about the property and owner. It is important that the information about the owner matches the passport details of the seller.

Checking for encumbrances

You can find out about the presence or absence of restrictions in the form of bail or arrest in the extract, or check the information yourself on the Rosreestr website. Just enter the address of the apartment, and the information will appear on the screen in a few seconds.

Legal advice: it is better to order an extended extract. Online information may not be current because... The database on the site is updated extremely rarely, approximately once a month. During this time, the seller could take out a loan secured by real estate, or receive a decree banning registration actions from the FSSP.

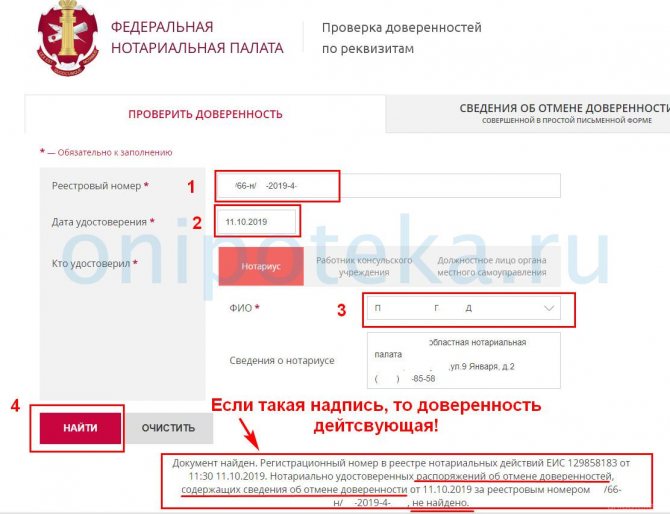

Verification of power of attorney

For real estate transactions, a notarized power of attorney is required (Article 185.1 of the Civil Code of the Russian Federation). The principal could give it to the attorney, and then cancel it before the transaction. You can check whether the power of attorney is valid on the FNP website. It is enough to enter the date of certification, registration number and information about the notary.

Verification of inherited real estate

The riskiest transactions are with real estate received by inheritance. If a person did not have time to enter into an inheritance for good reasons, then he will be able to restore the deadlines and challenge the policy. There is no way to check whether third parties can claim the apartment, even through a notary.

Legal advice: the deadline for accepting an inheritance can be restored within three years from the moment it became known about the death of the testator. It is optimal if the apartment has been owned by the seller for 7-10 years: this way the risks for the buyer are significantly lower.

Verifying Spouse's Consent

If the apartment was purchased during marriage, the seller must obtain the notarized consent of the spouse before the transaction (Article 35 of the RF IC). Otherwise, he will be able to challenge the sale within a year from the moment he became aware of it.

It’s easy to check whether the seller is married: just look at his passport and check the date of marriage with the date of registration of ownership of the home. If it is purchased during marriage, he must present the notarized consent of the spouse to the buyer.

If the apartment of a minor or incapacitated person is sold

The real estate of a child or incompetent citizen can be sold only with the permission of the guardianship authority. You can find out information about the owner in the extract from the Unified State Register of Real Estate. If he is under 18 years old, he must request guardianship permission from the seller.

Maternity capital was used to purchase an apartment

The most common and dangerous transactions for buyers are with real estate, for which maternity capital was used to purchase or pay off the mortgage. According to Art. 10 Federal Law dated December 29, 2006 No. 256-FZ “On additional measures to support families with children”, all family members must be allocated shares if maternity capital is spent for this.

Some sellers ignore these rules and buy housing and then sell it without allocating shares to all family members.

Important! The buyer's risk when purchasing real estate for which the seller has used capital is the possible challenge of the transaction. This can be done by the Pension Fund of the Russian Federation, the prosecutor's office, the spouse, or the children themselves upon reaching adulthood.

To check the use of maternity capital by the seller, just ask him for a passport and see if he has children born in 2007. If there is any, maternity capital definitely stood out. It is necessary to request from the seller a certificate about the balance of funds under the certificate: if it has not been spent, it means that the capital was not used to purchase housing.

For your information: the amount of maternity capital for the first child in 2020 is 466,617 rubles. Another 150,000 rubles are allocated for the second one if both were born after 01/01/2020. Previously, the certificate was given only for the second child.

Mortgage - checking the apartment by the bank

In order to protect itself from losses, the bank carefully checks the seller of the property for which it issues a mortgage. Key points:

- seller's ownership;

- legal capacity of the seller;

- power of attorney for revocation;

- the presence of the consent of the spouse or a statement that the property was not purchased during marriage;

- the presence of other uncalled heirs;

- permission of guardianship - if the owner is a minor;

- list of registered persons in the living space.

Next, we will consider each position in detail.

If the title belongs to the seller or several owners

The apartment can be sold by the owner or another person with a power of attorney. If there are several owners, all of them must participate in the transaction for the sale of the apartment. Therefore, the bank will require a document with information about the homeowners. Until 2020, there was a certificate of ownership for these purposes.

Later, they began to issue an extract from the Unified State Register of Real Estate, where all real estate objects and their movement are entered. During the inspection of the apartment when purchasing with a mortgage, the bank will identify all owners of the apartment using this document. The persons indicated in it, as home owners, must participate in the transaction and sign the purchase and sale agreement. In addition to information about the owners, these documents contain information about the basis for acquiring the right and the date.

Checking the seller's capacity

Typically, the seller’s capacity is determined by a bank specialist during a personal conversation, when the bank inspects the apartment for a mortgage. If a specialist has suspicions, he can request certificates of legal capacity - they are issued at the psychoneurological dispensary (PND) at the seller’s place of residence and contain information about registration. If the seller is not registered with the PND, this is the main confirmation of his legal capacity.

It is worth noting that such certificates are not mandatory when completing transactions, but they reduce the risks of terminating contracts in the future. Since banks always reduce their own risks, it would not be surprising to require such a certificate.

Power of attorney for revocation

There are often cases when an apartment is sold not by the owner himself, but by a person representing his interests. This person acts under a general power of attorney from the owner.

A power of attorney is issued for a certain period, but during this period it may lose its force.

The owner can revoke the power of attorney, for example, by changing his mind about selling the apartment. If a party with a power of attorney is present during the sale of an apartment, the bank will definitely check whether it has been revoked. To do this, just check it on the website - https://reestr-dover.ru/, which certified the power of attorney.

Recommended article: Buying an apartment through assignment of a mortgage

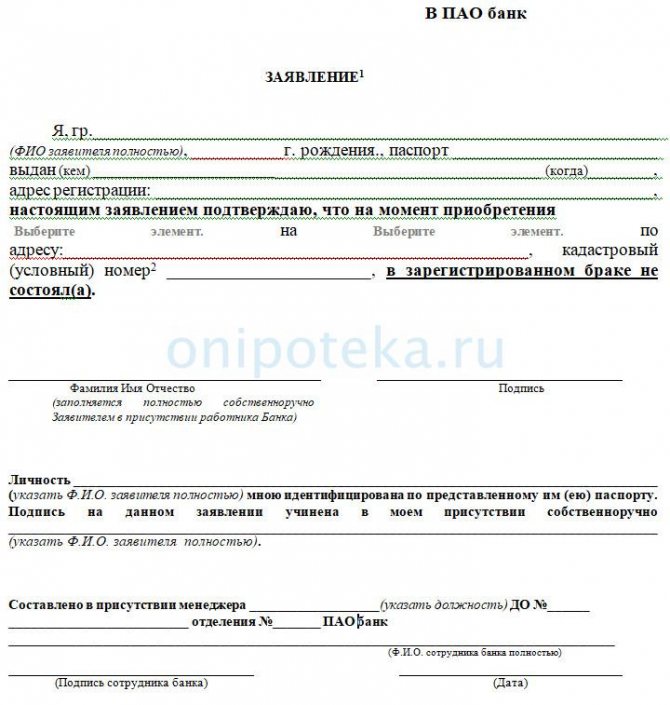

The presence of the consent of the spouse or a statement that the apartment was not purchased during marriage

Based on the laws of the Russian Federation, an apartment acquired by spouses during marriage is jointly acquired and belongs to both parties on equal terms (). When selling an apartment with a mortgage, one of the spouses inspects the apartment before the mortgage, where they will consider the issue of jointly acquired housing. A notarized consent of the second spouse for the sale will be required.

If the seller is not burdened by family ties, then the bank may request from him a notarized statement stating that at the time of purchasing the apartment he was not married.

And the notary, in turn, will demand from the person all the evidence of the fact that a bachelor purchased the apartment. Reducing its own risks, in any unclear situation the bank is more likely to refuse to purchase an apartment.

The presence of other uncalled heirs

Another risk area is inherited housing. If, when checking an apartment under a mortgage, the bank discovers that it was acquired by inheritance, the bank will most likely insist on additional title insurance. Especially if less than three years have passed since the date of acquisition (). The fact is that during this period you can challenge the entry into inheritance.

In any case, even after this period, the bank may request a certified will in order to identify hidden conditions for entering into an inheritance. Additionally, you may need a certificate of family composition at the time of receipt of the inheritance, as well as copies of any documents certifying the absence of unidentified heirs.

Resolution of guardianship when selling an apartment with a mortgage

Recently, it is common to find homeowners who have not reached the age of majority, having their own share on an equal basis with adults. When checking when purchasing a secondary apartment with a mortgage, the bank will require a decision from the guardianship authorities on compliance with the rights of the owners of minors. Children cannot be deprived of property in the form of a share of the right to an apartment or the opportunity to live in an apartment.

The guardianship makes a decision on the basis of certificates about future housing or the place where the children will be registered. A positive answer will be provided that the interests of the children do not change for the worse.

How to obtain guardianship permission is described in the article - Mortgage guardianship

Verification of registered persons

An important part of checking the legal purity of a mortgage is a certificate of people registered in the apartment. Since Russian legislation allows the sale of an apartment with registered people, the bank will definitely request a copy of the apartment registration card from the HOA or an extract from the house register. These documents will reflect the real situation regarding the registration of registered persons who are required to check out of the apartment before the sale or after a certain time (usually 14 days).

Lawyer's answers to private questions

Can I get a mortgage if I don’t have a residence permit? Will the bank check it?

Yes, permanent registration is required to obtain a mortgage. The bank will check it, like other information from the passport. If there is no registration, the mortgage will not be issued.

Does the bank check the allocation of shares to children if a mortgage with capital is used to purchase an apartment?

No, this is beyond the competence of banks. All checks on the expenditure of maternal capital are carried out by the Pension Fund.

What to do if, after checking the apartment, the bank refused a mortgage?

If a preliminary contract has been signed and a deposit has been transferred, and the bank’s refusal is considered a force majeure circumstance, the seller must return the money to the buyer. You will have to look for another property that the lender will approve.

Is it possible to speed up the inspection time for an apartment when applying for a mortgage?

No. Some deadlines are established by law, some by the bank’s internal rules. The borrower cannot influence this in any way.

How to protect yourself from challenging the purchase and sale agreement for an apartment purchased with a mortgage?

There are no guaranteed methods. Even after a full legal review, third parties may appear who have rights to real estate. But you can get title insurance against loss of title. If the deal is contested, the insurance company will pay the money.