What papers does the bank require to apply for a mortgage loan: list

A borrower who has chosen VTB 24 Bank for a home loan is required to present the following documents:

- Passport.

- SNILS or INN.

- A certificate reflecting the level of income in the form of a bank or 2-NDFL. An alternative option is the last year's tax return.

- Employment history. If the original cannot be provided, a certified copy of the document is required.

- Young people under the age of 27 inclusive must have a military ID with them.

Currently, VTB gives its clients the opportunity to participate in the “Victory over formalities” program. According to its terms, the borrower must show bank employees only SNILS and passport. When using such a benefit, 0.7% will be added to the base interest rate.

Clients who have reached retirement age, in addition to the completed application form, must present the following documents:

- a certificate reflecting the amount of old-age pension payments;

- an extract from an individual pension account;

- pensioner's ID.

If a client takes out a mortgage secured by housing owned by him or his relatives, an additional package of documents must be attached to the application form:

- A purchase and sale agreement, gift or other document confirming the emergence of ownership rights.

- Certificate of family composition.

- Certificate of ownership or certificate from Rosreestr.

- Report of the assessment commission on the value of the collateral object. The paper must contain those mentioned in Art. 11 Federal Law No. 135 dated July 29, 1998 details.

When purchasing secondary real estate, the bank requests the following documents:

- A copy of the cadastral passport.

- Certificate of family composition of the owner of the living space.

- Description of the apartment according to form No. 7. It must be taken from the passport office at the owner’s place of residence.

- The result of real estate valuation.

- Copies of passports of all property owners.

Important! If there are minors among the sellers of secondary real estate (for example, a child receives a share of the living space when part of its cost is paid off with maternity capital), the transaction can only be completed with the permission of the guardianship authorities.

When guarantors participate in a transaction, the list of securities depends on whether their total income was taken into account when determining the loan amount:

- If the solvency of a guarantor who is not married to the borrower has been taken into account, he must bring to the bank the same package of papers as the applicant.

- If the client refuses to assess the total income, it is enough for the guarantor to provide a passport.

- If the borrower is married and there is no prenuptial agreement between the spouses, the applicant's husband (wife) can become a co-borrower. The applicant's spouse needs to bring SNILS and a passport. Also, if the other half participates in the transaction, notarized consent for the purchase of a specific living space on a mortgage and a marriage registration certificate will be required.

List of additional documentation

VTB 24 Bank has the right to request additional documents from a client who does not take out a military mortgage and refuses to take part in the “Victory over formalities” program:

- certificates of unclosed loans that were taken out from other financial institutions indicating their amount;

- statements from savings and savings bank accounts;

- marriage contract.

It is not necessary to show the following documents, but their presence may increase the chance of getting approved for a home loan:

- diplomas confirming successful completion of educational institutions;

- an employment contract concluded with the main employer;

- extracts from Rosreestr for real estate owned by the borrower;

- documents for the car.

What kind of income certificate does the bank request?

A bank certificate is a form for an official income statement approved by a financial institution. The bank requests it if the borrower cannot bring form 2-NDFL.

What should be reflected in it, where can I get it?

VTB 24 Bank requests from its clients a certificate of income for the current and past calendar years.

The paper should reflect the following data:

- Full name and position of the client;

- information about the employer;

- salary after taxes;

- Full name of the company director and chief accountant, as well as the phone number of the accounting department.

We do not recommend completing the documents yourself. Save time - contact our lawyers by phone:

+7 (499) 938-90-71Moscow

Required documents

It will not be a secret to anyone that in order to fully and successfully implement the operation of obtaining a mortgage loan, the borrower will have to provide certain documents to a VTB Bank employee. So, only after all the “papers” and certificates have been provided, the mortgage agreement can be signed by the parties (the list of documents can be found out in advance by visiting the VTB website).

- Application form;

- passport of a citizen of the Russian Federation;

- work book (alternatively, you can provide a certificate in the form of a bank or a certificate in the form of personal income tax-2);

- a copy of the employment contract (if there is one);

- SNILS;

- taxpayer identification number;

- pension certificate or extract from the Pension Fund on the amount of the monthly pension (for persons who have reached retirement age);

- military ID (for persons under the age of 27 years).

( 5 ratings, average: 2.80 out of 5)

Borrower mistakes when collecting documentation from the list

In an effort to quickly collect all the necessary papers, VTB 24 clients often make the following mistakes:

- Attach to the application form 2NDFL with incorrect personal data or other errors.

- The sheets of the work book are not sewn together, there are no numbering, seal and signature of the notary on each page.

- A certificate of income level, a photocopy of the contract with the employer and the work record book were transferred to the financial institution after the expiration of these documents, equal to 45 days.

Features of a mortgage agreement

According to Art. 9 No. 102-FZ, a mortgage agreement is a type of agreement concluded by the parties in accordance with the Civil Code of the Russian Federation, which specifies the conditions under which real estate is left as collateral, as well as the permissible amount of obligations and the period for their repayment.

Where and by whom is it compiled?

As stated in clauses 2.10 and 2.17 of the Rules for the issuance of mortgage loans at VTB 24 Bank (“VTB 24 IMC”), the provisions of the mortgage and the standard mortgage agreement are drawn up by the financial organization itself. The agreement is concluded at a bank branch, which corresponds to Art. 444 Civil Code of the Russian Federation.

Points and content

The VTB 24 Bank mortgage agreement contains the following clauses:

- Information about the borrower and the mortgagee, played by the bank.

- Home loan amount, interest rate, monthly payment amount, period for which payments must be made.

- Penalties imposed in case of late payments.

- Information about collateral.

- Information about the additional object of mortgage lending (under an agreement secured by other real estate).

- Information about guarantors.

- List of risks that must be insured.

- Conditions for the bank to fulfill its obligations to provide a loan.

- Responsibilities of the borrower.

- The provisions on the basis of which a mortgage is issued.

- Final loan price.

We do not recommend completing the documents yourself. Save time - contact our lawyers by phone:

+7 (499) 938-90-71Moscow

When and by whom is it signed?

The mortgage agreement must be signed after the financial institution approves the questionnaire completed by the potential client. This rule is in accordance with Art. 403 and 405 of the Civil Code of the Russian Federation.

As stated in Part 1 of Art. 1 Federal Law No. 102, the parties to the mortgage are:

- creditor (financial organization);

- borrower (mortgagor).

Grounds for termination

A mortgage agreement can be terminated for several reasons:

- Art. 821 Civil Code of the Russian Federation . The bank is confident that the borrower will not be able to repay the finances within the established time frame. Such assumptions must be supported by strong arguments.

- Art. 12 Federal Law No. 102 . There are rights of third parties to the subject of the mortgage.

- Art. 4.1.2 “PVIC VTB 24” and art. 77 Federal Law No. 102 . The purchased housing did not go through the state registration procedure when concluding the purchase and sale agreement.

- Clause 4.1.1 “PVIC VTB 24” . No checking account for mortgage down payment and monthly payments.

- Clause 4.1.3 “VTB 24 PVIK” . The property insurance contract has not been concluded.

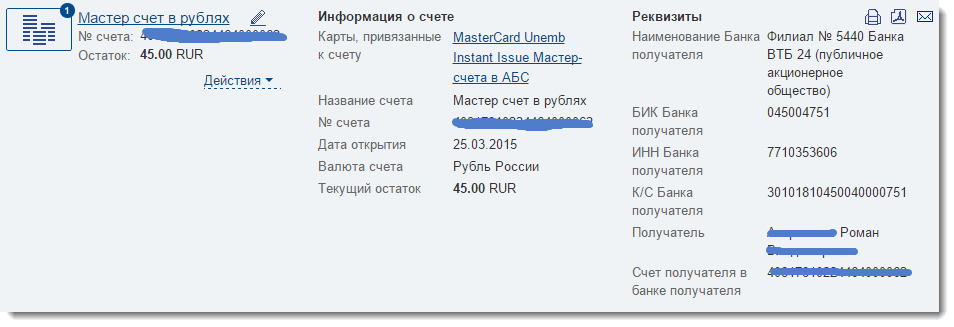

Master account features

Immediately after concluding the agreement, a master account is opened in three currencies: rubles, dollars and euros. It becomes active the same day. Persons who have opened a master account, in addition to standard financial transactions, can buy compulsory health insurance, mutual fund units and currency, as well as exchange it at the most favorable rate.

Additionally, the client is issued a ruble card from the Visa or MasterCard payment system. It is the main tool for carrying out key income and expense transactions. With its help, you can pay for purchases in a store, withdraw cash, or transfer funds to another card.

Cash deposits and withdrawals

You can top up your master account in various ways. However, the fastest and most convenient is to use VTB Internet banking. To complete the transaction, follow the following step-by-step instructions:

- Log in to the VTB Internet banking system by entering your username and password.

- In the main menu, open the “Payments and Transfers” section.

- Select "Transfer using bank details".

- Fill out the form, indicating the BIC and TIN of the financial organization, account number and other data.

- Please indicate the transfer size.

- Confirm the transaction with a unique code that will be sent to your phone.

Another way is to use a bank transfer system. Just come to the VTB Bank cash desk and give the operator your details and cash. Wait until he issues a receipt for payment. You can also use various services that provide money transfers. In Russia, the most popular are Unistream, Qiwi and Euroset. You can withdraw funds through an ATM using an instant withdrawal card linked to your account, or you can order cash at a VTB branch.

Comprehensive services from VTB have many undeniable advantages. The main thing is that the client has access to an extensive package of banking services free of charge. Additionally, a master account is opened in three currencies and a plastic card is issued, for the use of which no commission is charged.

Pitfalls of the agreement

VTB 24 Bank clients should pay special attention to the features of applying for a home loan in this financial institution:

- Within 2 weeks from the moment of signing the mortgage agreement, the borrower is obliged to conclude a purchase and sale agreement with the developer and register it in the Unified State Register of Real Estate.

- The mortgage note must be drawn up on the day the purchase and sale agreement is signed.

- Registration of agreements and mortgages in Rosreestr occurs with the participation of a bank manager who has the appropriate authority.

- The guarantor and the bank are required to enter into an agreement before the funds are transferred to the home seller.

- Before issuing a loan, the client must insure himself and the purchased property against the risks mentioned in the text of the contract. The responsibility for timely renewal of the contract with the insurance company rests with the client.

- The borrower does not have the right to unilaterally terminate a previously concluded contract with an insurance organization if the insured risks meet the lender’s requirements.

- It is allowed to enter into an agreement only with an insurance company that VTB 24 Bank has recognized as reliable.

Attention! In order to avoid getting into an unpleasant situation, you need to study in detail the bank’s requirements regarding early repayment of a mortgage based on a violation of the terms of the loan.

VTB 24 Bank provides its clients with favorable mortgage lending conditions. You can save time on collecting papers by participating in the “Victory over formalities” program, and it is convenient to confirm your income level through a certificate on the bank form. If the application is approved, the borrower has 14 days to select suitable living space.

What to consider before signing a mortgage

Insurance

- can the borrower independently choose an insurer, or does he have the right to choose only within the list of companies provided to him by the bank;

- the amount of insurance to understand how much this expense increases the loan, and what is more profitable to get a “discount” of 1% from the bank rate and pay for a voluntary insurance policy, or refuse insurance and increase the rate by one percent.

Requirements for a collateral apartment

All credit organizations, including VTB 24 and Sberbank, have tightened the requirements for their borrowers in terms of their disposal of residential properties that are pledged.

This applies to the use of living space and the rights of the owner to register other persons in the apartment, both on a permanent basis and as temporary residents.

Registration of new residents is prohibited

In particular, VTB 24 in its agreements prohibits the borrower from registering new tenants in the apartment. This provision applies to both family members and strangers. The exception is newborn children. If the borrower plans to get married and register a spouse after taking out a mortgage, it is advisable to clarify this issue before signing the loan agreement.

Renting is allowed if it is not specified in the contract

Quite often, citizens purchase housing on credit and immediately rent it out. This is possible if the mortgage agreement does not prohibit this, or the document does not contain any provision about this at all. Currently, in the VTB 24 standard agreement, renting a mortgaged apartment is expressly prohibited. This is explained by the fact that if the borrower fails to pay the debt and the apartment is repossessed in favor of the bank, the latter does not have the right to terminate the lease agreement until its expiration date.

Banks monitor the implementation of this point by their clients.

The borrower may use the mortgaged property only for his or her family's residence. If the borrower plans to rent, it is better to discuss this issue with the bank before concluding an agreement and stipulate this possibility in it, for example:

- with the consent of the bank,

- for a period of no more than 11 months without the right of automatic renewal.

Many citizens, despite their obligations, continue to rent out apartments in violation of the contract and without the written consent of the lender. This entails additional risks for them, up to and including termination of the mortgage by the bank. Taking into account that she is now taking out a mortgage, the repossession of housing occurs according to a simplified scheme.

Redevelopment is prohibited

For the entire term of the contract, the borrower does not have the right to carry out repair work or redevelopment of the housing. Exceptions include planned capital repairs of multi-apartment residential buildings.