Mortgage calculator

When deciding to purchase real estate on credit, a potential borrower must first calculate the monthly mortgage payment in order to understand the level of long-term credit load. The amount of payments should not exceed a certain proportion of the potential borrower’s monthly income, most often no more than 50%. Knowing the possible level of payments, a potential borrower can independently calculate the maximum mortgage size, loan term and overpayment. To calculate mortgage parameters, a special calculator is used, available to everyone.

A mortgage loan calculator is a program that contains a set of mathematical formulas and is used to determine the essential parameters of a loan. Calculating mortgage payments is the most important function of a mortgage calculator. In addition to the payment, the program allows you to calculate the mortgage amount, term, overpayment and other key conditions.

The cost of the mortgage, also calculated on the calculator, is affected by the interest rate on the loan, possible commissions and fees, and the amount of the down payment available to the borrower. For a more accurate calculation of the mortgage calculator, it is advisable to find out the interest rate and information about the presence of commissions for a suitable loan program.

A mortgage calculator is easy to find online.

It is convenient to use a mortgage calculator located on the websites of many banks. Often, such services take into account the category of the borrower, the desire to connect to an insurance program or refuse it, the type of housing being purchased, and a suitable loan program. Thus, mortgage loan calculators on bank websites allow you to find out the individual interest rate, calculate mortgage payments and other loan terms that are relevant for a particular borrower.

However, online calculators located on specialized Internet portals will help you calculate your mortgage. Such mortgage calculators calculate loan parameters based on user-specified conditions. An online mortgage calculator is an excellent opportunity to pre-calculate the size of the mortgage and the amount of overpayment without visiting the bank.

It must be remembered that the mortgage calculation obtained from a loan calculator located on third-party sites is not final.

You can also calculate your mortgage directly at the bank. The manager will give professional advice and calculate the mortgage for the desired apartment or other real estate.

Thus, those wishing to purchase a home can first assess their strengths and capabilities using a mortgage calculator.

Before taking out a mortgage for an apartment, potential borrowers should know the amount of monthly expenses. Professional employees of banks or real estate agencies calculate the loan amount based on the client’s monthly income, which is usually divided by 2. Thus, the maximum amount of monthly annuity payments is obtained. When calculating a differentiated payment, the scheme is slightly different: when divided by 2, the amount to be repaid in the initial lending period is obtained. The size of the payment under a differentiated schedule gradually decreases and becomes less than half of the monthly income, thus, free funds can be sent for early repayment. Now, according to the law, all loans are issued with early repayment without restrictions and commissions.

Calculating payments on a military mortgage does not make sense, since all payments are made by the state.

Potential borrowers can use the Banki.ru universal calculator to understand how much money they will be given for a mortgage. The service allows you to calculate the amount of your salary payment using the calculation method described above. Also, using the Banki.ru search, you can choose a loan for the required amount, with a specific down payment. In 2014, there were enough offers on the mortgage market without a down payment.

Requirements for the borrower

The minimum requirements for a borrower applying for a mortgage from VTB 24 for a plot of land or construction of housing as part of non-targeted lending for the construction of a private house are as follows:

- Work experience at the current place of work is at least one month after the probationary period with a total experience of at least one year.

- Sufficient creditworthiness of the client with the ability to confirm it with documents.

- No damaged credit history.

- Russian citizenship is not required.

- Any registration within the country.

- Age from 21-65 years.

The bank does not have strict requirements for the place of work. A potential client can be employed either in any company in the Russian Federation or in branches of TNCs abroad.

If the borrower’s income level does not allow the mortgage application to be approved, the bank may recommend attracting co-borrowers under an agreement (no more than 4 people).

The living space pledged to VTB 24 is carefully checked by the bank and must also meet a number of strict requirements regarding the absence of debts for utility bills, encumbrances, arrests, illegal redevelopment, the presence of all necessary life support systems, and the absence of persons (especially minors) registered in the apartment. Additionally, the bank may impose requirements on the location of the object, its wear and tear, technical and other characteristics.

How to apply

An application for a mortgage to build a house at VTB 24 is submitted in two available ways: online on the lender’s official website or by visiting a mortgage department in person.

In the first case, the client will have to fill in the following basic information about himself:

- personal information (full name, date of birth);

- contacts (phone number and email address);

- passport details;

- data on the employer (TIN, name, amount of income per month, length of service);

- information about the required loan (purpose of lending, amount, repayment period);

- city where the loan was issued.

After filling out this form, a specialist from VTB 24 will contact the client almost immediately to clarify the information and schedule a day convenient for the borrower on which he can visit the authorized mortgage center. During the meeting, the client will sign the submitted application and give the manager a package of pre-collected documents.

Important point! To increase your chances of getting a mortgage, we recommend applying to several banks at once here.

General mortgage terms VTB 24 for 2020

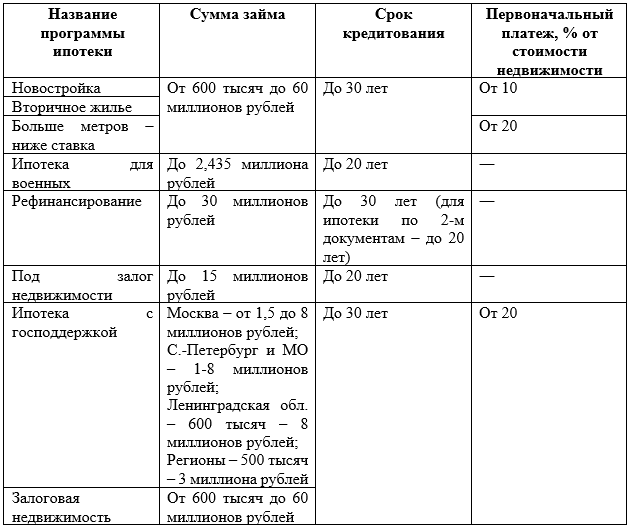

In 2020, VTB 24 operates 8 mortgage programs. Key conditions for them are presented below.

According to standard mortgage programs at VTB 24 (“New building”, “Resale housing” and “More meters - lower rate”), the borrower will be able to buy real estate worth up to 60 million. This is the maximum amount of borrowed funds issued by the bank.

Programs that provide financial support from the state are characterized by a fairly low mortgage amount: up to 12 million for a family mortgage and up to 2.84 million rubles for a military mortgage.

Is it possible to use maternity capital?

A VTB 24 mortgage for a plot of land or the construction of a private house, issued with a loan secured by an apartment, allows the use of maternal capital funds to repay the existing debt on the principal debt and accrued interest. This is relevant for existing loan agreements. It will not be possible to direct this state assistance towards an initial payment for the program under consideration, since it does not imply its availability.

Any manipulations with maternity capital are carried out only with official consent from the Pension Fund. To do this, the borrower will need to obtain a certificate from VTB 24 about the status of the loan debt and copies of the loan documentation.

The Pension Fund will also require documentary and payment confirmation of the intended expenditure of borrowed funds under this agreement. That is, you should collect all receipts, contracts for the provision of services/works and contracts that were concluded for construction, repair, finishing and other work on the construction of your own home. Matkapital will be transferred to pay off the mortgage only if the Pension Fund is convinced that the money was spent exclusively on improving the family’s living conditions.

According to Russian legislation, it is possible to use maternity capital to pay off an existing mortgage without waiting for the child to reach the age of 3, who is entitled to receive such assistance from the state.

We wrote more about building a house with the help of maternity capital earlier.

How to get a mortgage without a down payment in VTB 24: procedure for an overstated scheme

Since it is impossible to obtain a standard mortgage from VTB without a down payment, you can get around the lack of such a program by using a scheme to inflate the cost of the purchased housing.

The bottom line is this:

- the buyer agrees with the seller of secondary housing to inflate the price of the property by the amount of the down payment required by VTB 24 and stipulates it in the purchase and sale agreement;

- the seller writes a receipt confirming receipt of a specific advance amount from the buyer;

- VTB 24 lends to the borrower for the remaining amount, which unofficially amounts to 100% of the actual price of the property for the buyer.

IMPORTANT! It is highly recommended to make two receipts. One is written by the seller and confirms the fact of receiving an advance from the buyer. The second is for the buyer to return the advance received to the opposing party. This will protect both parties to the transaction from possible risks. We talked about this in more detail when we talked about overpriced mortgages.

Pitfalls you need to be aware of

The volume of documents is quite large. If you have no experience working with banks, then it is quite difficult to study all the material. The client may not understand all of its provisions and miss important information. To avoid any unpleasant surprises later, you need to pay attention to the following points:

- Insurance – you must pay for the policy throughout the entire loan term. If this condition is not met, then the bank increases the rate by 1%.

- Without the bank's permission, only close relatives can be registered in the purchased apartment.

- In order to rent out an apartment or carry out redevelopment in it, you need to obtain permission from the mortgagee.

- If all the terms of the agreement are not met, the bank may demand early repayment of the entire debt amount.

- Every year, the client must provide documents on his income, papers on payment of utilities, mandatory payments and taxes. The lender must ensure that the individual does not have any debts. Their presence may lead to the seizure of the collateral by third parties.

If the applicant still has any questions, they can be asked to a bank employee. But the manager is a stakeholder, so his answer may be biased. It is advisable to consult with an experienced lawyer. This way, the client will be confident that there are no pitfalls in the agreement.

You can also get a free online consultation from our qualified specialists. Ask questions and get answers instantly.

We wrote a lot of useful information about mortgage lending in this article.