What is a mortgage

A mortgage is a form of collateral in which the debtor transfers real estate to the creditor. Subsequently, the lien holder can get his money back through the sale of the property.

In the financial dictionary, the term stands for putting real estate as collateral to obtain a bank loan. The common man is accustomed to understanding the word “mortgage” as housing lending. There is another interpretation, “mortgage is slavery,” with which one cannot but agree. Especially when it comes to foreign currency loans.

A mortgage, like a bank loan, is issued to any citizen of the Russian Federation who meets all the requirements of a financial organization and has a sufficient level of income. Moreover, to obtain a loan, it does not matter whether the borrower owns another residential premises. A mortgage can be applied for a second or third time (depending on desires and capabilities).

The mortgage period is... What is the Mortgage period?

Mortgage period Mortgage period Mortgage period is the period of time from the receipt of applications from potential mortgage borrowers to the sale of loans.

In English: Mortgage pipeline

Financial Dictionary Finam.

.

- Mortgage

- Mortgage market

See what “Mortgage period” is in other dictionaries:

- Mortgage period - The period of time from the receipt of an application from potential mortgage borrowers to the sale of loans ... Investment Dictionary

- Mortgage crisis in the USA (2007) - The mortgage crisis in the USA (eng. subprime mortgage crisis) is a financial and economic crisis, the characteristic manifestations of which were an increase in the number of non-payments on high-risk mortgage loans, an increase in cases of foreclosure... ... Wikipedia

- Mortgage crisis of 2008 - The global financial crisis of 2008 and the recession of the late 2000s is a financial and economic crisis that manifested itself in 2008 in the form of a deterioration in key economic indicators in most countries, and the global crisis that followed at the end of the same year... ... Wikipedia

- Mortgage crisis - (Mortgage Crisis) Definition of the mortgage crisis, causes of the crisis in the USA Information on the definition of the mortgage crisis, causes of the crisis in the USA Contents Contents Definition in (2007) Losses Estimates Causes in the USA Chronicle of the US mortgage crisis and... ... Investor's Encyclopedia

- Mortgage loan - A mortgage is a pledge of real estate. A pledge, in turn, is one of the ways to ensure the fulfillment of the obligation of a monetary claim of the creditor of the pledge holder to the debtor (pledgor). As a way to ensure proper execution... ... Wikipedia

- Mortgage bank - Headquarters of the mortgage bank Vorarlberger Landes und Hypothekenbank in Bregenz ... Wikipedia

- DUAL RATE MORTGAGE DRM An inflation-protected mortgage, the first payments on the rom are made at a lower rate, and then gradually increase in accordance with the rate of inflation (if any) so that annual payments ... ... Encyclopedia of Banking and finance

- A mortgage loan is a loan secured by real estate. The simplest form of mortgage, which existed in Ancient Greece in the 7th and 6th centuries. BC e. Under the slave and feudal system, K. and. was a type of usurious loan, carried in... ... Great Soviet Encyclopedia

- A non-delivery option is an additional hedge with respect to the mortgage period together with a forward or replacement sale. In English: Option not to deliver See also: Mortgage period Financial Dictionary Finam ... Financial Dictionary

- Mortgage period risk is the risk associated with receiving applications from potential mortgage borrowers who may then refuse to accept the advertised mortgage rate during a specified grace period. In English: Mortgage pipeline risk See also: Risks... ... Financial Dictionary

dic.academic.ru

What types of mortgages exist

It is customary to distinguish several types of mortgages:

- Standard. It is issued on conditions common to all.

- Social. Focused on low-income citizens and provided with government support.

- "Young family". Designed for persons whose age does not exceed the established threshold of 35 years. It is also provided on preferential terms with financial support from the state.

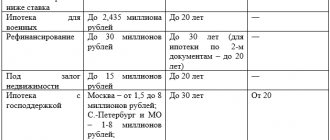

- Military mortgage. A special banking product for military personnel. Here, too, it could not have happened without the help of the state, because... NIS funds are involved in the loan project.

Additionally, mortgage loans can be classified depending on the purpose for which financial resources are requested: the purchase of residential premises in a new building or on the secondary market, a plot of land or the construction of a house.

Mortgage loan - what is it?

Differential payment is constantly changing. The most common option is that the principal amount is fixed for the entire loan term, and interest is charged on the remaining debt. Due to this approach, the monthly loan payment decreases slightly each time.

The interest rate is based on the key rate of the Central Bank of the Russian Federation (another name is the refinancing rate), which in 2020 is 7.25%. The credit institution adds a small percentage of margin (i.e., profitability) to the indicator established by the Central Bank. In some cases, the target mortgage rate may be lower than the key rate. This situation applies to the same special programs in which part of the obligations is financed by the state.

Types of mortgage payments

To repay a target mortgage, there are 2 types of payments: constant (annuity) and variable (differentiated).

The annuity payment remains unchanged throughout the entire loan period. In its composition in the first months, interest for using the loan predominates, and only a small part falls on the body of the loan. Over time, the proportions of interest and the debt itself change and by the end of the term the borrower begins to pay off the principal debt. If you choose Sberbank for lending, the payment will be exactly like this.

Differential payment is constantly changing. The most common option is that the principal amount is fixed for the entire loan term, and interest is charged on the remaining debt. Due to this approach, the monthly loan payment decreases slightly each time.

This approach is rarely used in mortgage lending, since in the first months the load on the family budget turns out to be unbearable. Rosselkhozbank is one of the few that still practices processing such payments as part of a mortgage.

Along with this, there are other types of differentiated contributions:

- A schedule that implies an increase in payment. Established for borrowers who are temporarily in a difficult situation, but over time will become solvent enough to pay higher premiums.

- Balloon payment. A large payout is used at the end of the term. For example, for the entire term of the loan, the borrower paid only interest, and in the last month he must pay back the amount of the principal debt. Or vice versa - interest is paid as part of the last installment. There are also cases of combined payments: for several years the client pays the bank part of the principal loan and part of the interest, and the remaining amount is still paid in a lump sum at the end of the term.

- With variable interest rate. It is used mainly within programs with government support. At first, a lower rate is set, and then it increases to the general level. For the period when the interest rate is lower, the state pays the bank the lost profit.

General concept of interest calculation

The concepts of fixed and floating mortgage interest rates most often raise questions among potential loan recipients. This is quite profitable for banks who make profits from ill-informed customers.

Fixed method

The first step is to understand the fixed interest rate. Everything here is quite simple: regardless of any circumstances, the percentage remains the same, equal to what was specified in the contract when it was signed. For example, if at the time of receipt of funds the contract specified a rate of 11%, then it will remain so until the end of its validity under any circumstances.

This type of lending is the safest for bank clients, because the guarantee of stability allows you to properly plan your budget and repay all debts on time. This is practically impossible with a floating rate loan, since with a long term of the contract (for example, 30 years for a mortgage), the likelihood that events will occur that will affect the change in the percentage of overpayment for the service is quite high.

When receiving a loan with a fixed interest rate, the client immediately receives the entire repayment schedule for the entire period. If there is a delay, the schedule will be recalculated. Thus, the payment procedure is as transparent as possible for the client and he does not have any thoughts about possible fraud on the part of the bank.

In addition, the fixed rate on the loan allows you to repay the money in differentiated payments, which imply an identical repayment amount for each month. The amount of payments in this case is calculated using the formula:

P = OST / KM + OST * PM, where

- P - monthly payment amount;

- OST - the balance of funds required for repayment;

- KM - the remaining number of months or other periods that are designated by the client and the bank in the agreement as settlement, until the end of all payments;

- PM - interest on the loan per month (obtained by dividing the annual interest rate by 12).

As an example, consider one situation. A resident of a small provincial town took out a loan in the amount of 100 thousand rubles with a fixed interest rate of 15% per annum. The client plans to repay it in full in 12 months through 12 equal payments. In this case, the table of differential payments will look like this:

| Payment number | Balance of debt, rub | Amount of interest paid in this period, rub. | The amount of the principal part of the debt that was paid in this period, rub. | Total payment amount in this period, rub |

| 1 | 100 000 | 1250 | 8333,3 | 9583,3 |

| 2 | 91 666,7 | 1145,8 | 8333,3 | 9479,2 |

| 3 | 83 333,3 | 1041,7 | 8333,3 | 9375 |

| 4 | 75 000 | 937,5 | 8333,3 | 9270,8 |

| 5 | 66 666,7 | 833,3 | 8333,3 | 9166,7 |

| 6 | 58 333,3 | 792,2 | 8333,3 | 9062,5 |

| 7 | 50 000 | 625 | 8333,3 | 8958,3 |

| 8 | 41 666,7 | 520,8 | 8333,3 | 8854,2 |

| 9 | 33 333,3 | 416,7 | 8333,3 | 8750 |

| 10 | 25 000 | 312,5 | 8333,3 | 8645,8 |

| 11 | 16 666,7 | 208,3 | 8333,3 | 8541,7 |

| 12 | 8 333,3 | 104,2 | 8333,3 | 8437,5 |

Thus, within one year, the client will fully repay the loan, and the payment amount will decrease slightly each month: the first payment is almost 9,600 rubles, and the last is almost 8,500 rubles.

The main disadvantage of this type of interest calculation is the lack of attractive offers from banks. As a rule, most options involve payments under a floating system. And if you come across a fixed rate, then the percentage itself is too high. Because of this, most people have to choose another option.

Floating option

Once the term fixed rate is disassembled and understood, you can move on to floating. Here everything works much more complicated. The bulk of loans issued at this rate are mortgages.

The floating mortgage rate consists of two parts that are summed up: a constant and a variable component. The first part is the percentage set by bank representatives. It is prescribed in the contract and does not change during its validity. As a rule, the bank's margin is no less than 0.5% and no more than 5%.

The variable term depends on the current value of funds:

- The refinancing rate, which is approved by the Central Bank of the Russian Federation. Directly depends on the economic situation within the country.

- Indicative rate for providing loans according to the Moscow Prime Offered Rate. This is an independent organization that analyzes the Moscow money market and announces its rate.

- European Interbank Offered Rate is an average interest rate obtained based on interbank loans in European currency.

- London Interbank Offered Rate is the average value of the overpayment percentage, which is obtained from statistics on interbank lending on the exchange in London.

Depending on the bank, one of the above values will be used. Then the bet level is determined by one of the following formulas:

- Indicator from the Central Bank of the Russian Federation +% of the bank;

- Indicator from Moscow Prime + % of the bank;

- Indicator from EUR Interbank +% of the bank;

- Indicator from London Interbank +% of the bank.

The main advantage over fixed rates is the bank’s rather low margin.

In other words, if the country has a stable economic situation and there are no difficulties in the development of the financial market, then the interest will remain small for the entire period.

If financial market problems arise and the economy begins to collapse, then the interest on the loan can seriously increase, up to unaffordable amounts. Therefore, those who agree to an adjustable rate mortgage are risking their financial freedom.

In the case of a fixed rate, such problems are impossible, because it remains the same in any market situation. However, it itself is quite higher compared to floating.

In general, interest rates with a floating rate do not change much. In the 90s, in our country, the SR from the Central Bank of the Russian Federation reached more than 200% per year. Today this figure is 8.75%. However, no one can guarantee that this will not happen again, especially in the long term.

Combined method

There is also a combined interest rate, which includes the principles of two standard ones. Such agreements with the bank imply that the entire repayment period is divided into two parts. In the first few years the percentage will be fixed, after which it will begin to change.

An excellent example of a combined rate is the mortgage program from VTB24 bank. In it, the overpayment interest is calculated according to the table:

| An initial fee, % | Maximum rate during 1st year, % | Maximum rate for 2nd year, % | Interest limit for the 3rd year, % | Formula for determining the rate in subsequent years of repayment |

| More than 60 | 8,9 | 9,7 | 9,9 | 3% + SR (Central Bank refinancing rate) |

| From 40 to 60 | 12,25 | 13,05 | 13,25 | 3% + CP |

| From 20 to 40 | 12,75 | 13,55 | 13,75 | 3.5% + SR |

A loan with a combined rate is an average option that includes the advantages and disadvantages of standard methods. There remain risks of an unforeseen situation in the financial market, as a result of which the interest rate will be greatly inflated. The client's protection from this is valid only for the first 3 years, after which interest is calculated according to the standard formula.

However, such a loan is also much more profitable than a fixed one, provided that the interest is not greatly inflated. It is recommended to agree to such conditions if you plan to complete all payments and close the issue within the first few years. Otherwise, the risks will increase.

Sberbank is the most popular bank in Russia. Therefore, most citizens tend to apply for lending services here.

Most offers from Sberbank imply a fixed percentage. Several years ago, information appeared in the media that the bank plans to implement a floating rate when providing mortgage lending services, as well as for standard credit cards. However, this has not yet happened.

What is the mortgage interest rate

Interest rate is the fee for using someone else's money. It is established as an annual indicator. For example, if the bank claims 13% per annum, then the client will pay exactly 13% of the debt amount for the year. Moreover, every year the amount of interest in monetary terms will change, because the main debt is gradually repaid.

Some credit organizations, wanting to get a client, announce interest rates without “per annum.” Such proposals should be taken critically: perhaps the stated fee will be charged not per year, but per month.

Most often, such dishonest attitude can be found in microfinance organizations. Banks try to be honest and open about their conditions (with rare exceptions).

The interest rate is based on the key rate of the Central Bank of the Russian Federation (another name is the refinancing rate), which in 2020 is 7.25%. The credit institution adds a small percentage of margin (i.e., profitability) to the indicator established by the Central Bank. In some cases, the target mortgage rate may be lower than the key rate. This situation applies to the same special programs in which part of the obligations is financed by the state.

What does the dynamics of mortgage market development say?

Credit market specialists say that the key trend in the development of the mortgage market today is to soften the conditions for mortgage loans. This situation is largely due to the pursued policy of the Central Bank aimed at reducing the key rate. Its previous value was set at 7%, but already on October 25, 2020, at the next meeting of the Board of Directors, a decision was made to further reduce it to 6.5%.

In August, a significant number of banks responded to the decision to reduce the key rate by announcing changes in lending conditions for mortgage offers. The reduction under the programs for new buildings in April 2020 remained at 10.13%, and in September it already dropped to 9.12%. For the first time in recent memory, rates on secondary market products have dropped below 10%.

At the same time, inflation is projected to decline below the target level of 4%, which suggests that there is potential for an even greater reduction in lending rates. The passport of the national project “Housing and Urban Environment” sets the goal of achieving a mortgage rate of 7.9% by 2024.

The expected trends in the lending market should be:

- reduction in interest rates;

- growth in lending volumes;

- cooperation between developers and banks;

- easing loan conditions.

Indicators of the volume of demand for the purchase of residential real estate using a mortgage mechanism depend on the level of interest rates on loans. The observed dynamics of their decline should create effective demand for housing. He will support the launch of new projects by developers, taking into account the latest changes in project financing and the use of escrow accounts.

What is the subject of a mortgage

The subject of the mortgage is the property that is planned to be pledged. Article 5 of Law No. 102-FZ “On Mortgage” strictly regulates the list of property that can be pledged under a mortgage:

- land;

- buildings, structures, enterprises;

- residential real estate (apartments, houses, rooms);

- garages, dachas, garden houses;

- aircraft and ships;

- parking spaces.

If the real estate is owned by the borrower on a leasehold basis, the law allows for the pledge of these rights. Property can be encumbered only in its entirety, together with all available accessories, and private houses and detached buildings - exclusively together with the plot of land on which they are located.

What is Title Insurance for a Mortgage?

Often a phenomenon occurs, the result of which becomes the reason for the occurrence of an insured event. This happens quite often, since it is impossible to check all the information within the time frame given for processing a mortgage transaction. What does a title insurance policy mean in a specific case?

The question of how much title insurance costs for a mortgage is considered an integral part of the transaction. Each insurance company determines the cost independently. Most often, the range varies from 0.3-1.5% of the loan size. In general, the price of such protection is comparable to the cost of life and health insurance for a mortgage. Insurance is selected individually for each borrower. The cost of title insurance for a mortgage (amount of insurance premium) depends on the following factors:

What is the title period

In the case of purchasing housing on the primary market, the concept of the title period is applied. This is the period of time that began at the time of registration of ownership of the housing purchased with a mortgage and continues until the end of the loan agreement.

Before the borrower acquires ownership rights, there is a phase of construction and commissioning of the building. This period is called the investment period.

Typically, the interest rate decreases during the title period. However, along with a reduction in interest, the bank may require so-called title insurance. That is, insurance is issued for the risk of “loss of property rights.”

What is the investment period in a mortgage?

INVESTMENT ANALYSIS - Income. A natural criterion for comparing investment alternatives is the rate of return, or rate of return (yield), calculated as the ratio of the change in value to the original cost. Algebraically it can be expressed as follows... Collier's Encyclopedia

- Unlike standard lending to individuals, the bank does not check the borrower himself, but the competitiveness of his project, which is why the key document influencing the bank’s approval is a feasibility study - a feasibility study of the measures.

- The investment loan is subject to restrictions for the bank. Thus, the bank cannot demand a percentage that exceeds the profitability of the project and provide a loan for a period shorter than the payback period of the project (the desire of an entrepreneur to repay the loan as early as possible can play a cruel joke on his business). The presence of such limits forces banks to review the feasibility study and investment project even more carefully.

- An entrepreneur can use a grace period for repayment, that is, pay only interest on the loan without reducing the principal portion of the debt. He begins to repay the loan in full after the facility is put into operation.

- Investment loans are strictly targeted. Funds are spent exclusively on reconstruction or modernization. Lenders carefully monitor to ensure that the money is not “spent” on other needs. In some cases, credit institutions even assist entrepreneurs themselves in financial settlements in order to organize timely receipt of monthly payments.

This is interesting: Belgorod help for a single mother

Is it possible to cash out a mortgage?

As a general rule, the loan amount is transferred to the account of the seller or developer. Therefore, the only way to legally cash out a conventional mortgage is to take advantage of the appropriate bank offer. Some financial institutions allow you to withdraw cash from a loan account and independently make payments to the seller. But in this case, in order to properly secure the loan, the client will be required to provide collateral for other, non-purchased, real estate.

Military personnel have another way to legally cash out. If a NIS participant retires from military service after completing the required length of service, he is legally entitled to receive mortgage funds. All the money accumulated by that time in a special account is issued in person.

Important! All other offers that can be found on the Internet are fraudulent schemes, each of which has its own article in the Criminal Code.

Do I need to insure my mortgage?

If you are aiming to take out a mortgage, then you should be interested in the question - is mortgage insurance required or not? All borrowers ask this question, because insurance is not cheap, especially since it must be renewed annually. But its cost is sometimes included in the mortgage amount, which means you will also pay interest on its amount. By obliging borrowers to insure their mortgage housing, banks ensure repayment of the loan. Therefore, insurance is required . But insurance exists in several forms, each with its own nuances.

How to make money on a mortgage

At first glance, the question sounds strange: calling a mortgage slavery, are you trying to make money on it? However, there are really real and legal ways to make money here. True, there are only two of them:

- Renting out purchased real estate. It is important here that the rental amount covers not only the loan itself and utility bills, but also the borrower’s additional insurance costs. Therefore, when purchasing an apartment for this purpose, it is important to study the prices on the rental housing market in advance.

- Resale of housing. This implies the purchase of an apartment at the excavation stage at the minimum price and its subsequent resale after the house is put into operation. Here, the opportunity to earn money can last for many years and there is a risk of ending up in a long-term or unfinished project. In addition, it is worth considering the amount of bank interest. In some cases, the total amount paid to the bank is enough to purchase two similar apartments.

Title insurance of real estate: what is it?

The existing right of ownership of real estate can only be challenged through the courts. If one of the former owners of the apartment decides to do this, you will receive a summons to do so. This situation will need to be reported to the insurance company immediately. This must be done; notification periods will be specified in the title insurance contract.

This is interesting: How much does one day in the garden cost 2020 in Serpukhov 8 hour day

In this case, force majeure will be considered, for example, the loss of rights to real estate as a result of military action or its confiscation by the state. The consequences of man-made or natural disasters also fit this definition. By the way, keep in mind that title insurance does not cover damages you incur as a result of property destruction. In this case, you lose the property, but not the right. These situations are resolved with the help of property insurance.