What documents are needed for a mortgage at VTB? The answer is everything that confirms your financial condition and your credit history . You will need income certificates, tax returns for entrepreneurs, work books for employees, etc. In addition, your identity must be confirmed with a passport and any other document. There are also a number of nuances - for example, if the applicant is married, the consent of the spouse is required to purchase real estate, etc. In this article we will explore in more detail the documentary issue of obtaining a mortgage, possible nuances and solutions to problems.

General list of documents for obtaining a mortgage

VTB is the second bank in the country after Sberbank. And, like any other large bank, VTB is very selective in issuing large loans. Mortgage loans, in turn, are considered almost the largest loans in Russia issued to individuals and legal entities in a “line-by-line” mode.

Therefore, a general list of documents has been established that bank employees will require in any case when the applicant applies.

Help: those who want to understand the topic of mortgage lending in depth are recommended to study Federal Law No. 395-1 “On Banks and Banking Activities” and the Federal Law “On Mortgages (Pledge of Real Estate)” dated July 16, 1998 N 102-FZ. It is these legislative acts that list the rights and obligations of banks when issuing mortgages. Based on these laws, you can understand which documents the bank has the right to require and which ones it does not.

So, the package of documents required in any case looks like this :

- Original internal passport of the Russian Federation. Accordingly, VTB does not issue mortgage loans to foreign citizens, even if they have obtained a residence permit in Russia;

- Any other document proving the identity of the applicant. For example, a driver’s license, SNILS, TIN, etc. will do;

- A document confirming the applicant's employment. As a rule, an employment contract is accepted in this capacity, but a civil law contract can also be accepted.

Please note: you may bring copies of your passport. But in this case, all pages of the document must be scanned, including its blank parts. Otherwise, the applicant’s documents will not be accepted until all copies or the original passport are provided.

As can be seen from the list above, documents for obtaining a mortgage at VTB are required by the bank in order, firstly, to establish and verify the identity of the borrower, and secondly, to ensure his solvency. Therefore, documents confirming the applicant’s fulfillment of the first and second conditions should be treated with special attention.

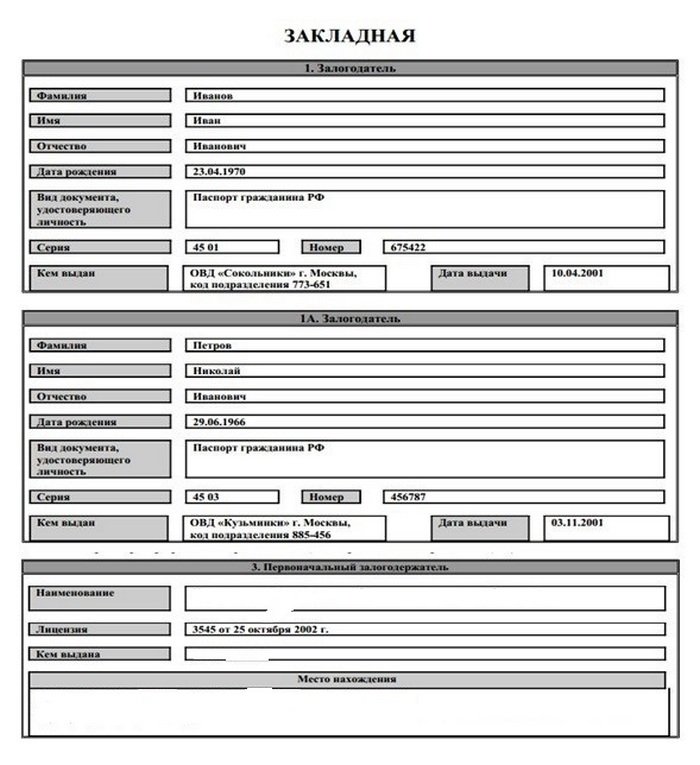

VTB mortgage note: mandatory clauses in the document

Despite the fact that VTB employees are involved in processing the mortgage, the borrower is obliged to check its correctness, since he puts his signature on it.

A mortgage is a personal document. It contains the personal and passport details of the mortgagor. Even competent bank employees can make mistakes in filling out, so the mortgagor is advised to carefully check the relevant fields of the document.

The mortgage includes a number of mandatory items, the presence of which is verified by the mortgagor. This:

- Title of the document;

- Mortgage agreement number;

- Complete information about the pledgor and pledgee;

- Information about the borrower’s credit obligations (the size of the loan, the rate, etc.);

- Indication of the term of the mortgage agreement;

- Information about the mortgaged apartment, allowing it to be identified;

- Information about the estimated value of the mortgaged apartment;

- Confirmation of the absence of encumbrances on the mortgaged apartment (except for the mortgage being issued);

- Title documentation (purchase and sale agreement, DDU);

- Data on the registration of the transfer of rights to the pledged object;

- date of document preparation;

- Signatures of the pledgor and the pledgee;

- Bank stamp.

The mortgage is issued for a two-week period. However, in Moscow and St. Petersburg, the registration period can reach 30 days due to the high demand for housing in these cities.

Documents for different groups of borrowers

Conventionally, these groups can be divided into two categories:

- Entrepreneurs;

- Wage-earners.

Depending on the type of activity, the documents for obtaining a mortgage at VTB differ. Let's take a closer look at them separately.

For entrepreneurs

The general essence of the papers required from entrepreneurs comes down to the following: the bank needs to prove that your company has sufficient turnover to pay off the loan. That is why the list of required documents is quite lengthy, because in addition to the main list, you need to present to bank employees:

- A certificate from the register of shareholders or from the Unified State Register of Legal Entities. The certificate must confirm that the applicant is an individual entrepreneur or founder of an enterprise. The validity period of the certificate is limited to 45 days from the date of issue, so it should be taken immediately before submitting the papers for consideration;

- Tax return for the last 12 months or for the current reporting period;

- For current accounts opened in other banks, certificates of no debt must be provided;

- Certificate of tax registration of your company. Accordingly, the document is issued at the territorial branch of the Federal Tax Service if for some reason you have lost the original document;

- A certificate from the Federal Tax Service about the state of your enterprise, the amount of taxes paid and annual turnover. Also, instead of this document, an accounting journal is accepted;

- If your business is based on licensed activities, you will need a copy of the state license.

On the one hand, the list of documents required for a mortgage at VTB 24 is quite extensive. On the other hand, it is entrepreneurs who, if they prove their solvency, have the greatest breadth of choice: they are provided with the most profitable and large loans. This also applies to mortgage loans, especially if they are issued for commercial purposes.

For employees

You will need:

- Certificate of income in form 2-NDFL. You can obtain this document from the employer, and it must be signed by the head of the enterprise and the chief accountant. In addition, the certificate must bear the employer's stamp;

- A copy of the work book with notes on the total work experience for the last five years, at least one year, and for the last 6 months, at least three months. The copy must be certified by the head of the employing enterprise.

Please note: Military and law enforcement personnel working under a contract must present a certified copy of the latest contract and a certificate of length of service in place of the above documents. You can obtain these papers either at the district commissariat or at your place of service.

Separately, it should be clarified that VTB payroll clients are not required to provide documents confirming their solvency. The bank already knows about all the client’s financial movements related to his official employment.

List of documents for completing the application

To obtain a loan from a bank to purchase real estate, you first need to submit an application.

In this case you will need to provide:

- Application forms.

- Civil passports of borrowers.

- SNILS (for Russian citizenship of applicants).

- Documents confirming income: for an individual - certificates in form 2-NDFL or in the form of a bank, for an individual entrepreneur - a declaration for the last year. These items are skipped for payroll clients.

- Work record book (duly certified copy) or certificate (extract) from it.

- Military ID (if the borrower is a man within the conscription age range).

- Migration documents (for foreign citizens).

The bank has the right to request additional documents necessary to make a decision on issuing a loan or refusing to provide it.

General additional documents

There are times when a slightly expanded package of documents is required. The most common situations are:

- For male applicants under 27 years of age, a military ID is also required;

- If a third party is involved in the purchase and sale as a representative of the applicant, a notarized power of attorney is required;

- If the applicant has a spouse, firstly, a notarized consent to purchase an apartment on a mortgage is required, and secondly, the original marriage certificate;

- If any share of real estate belongs to a minor, permission from the guardianship and trusteeship authorities to change living space will be required.

List of documents for purchasing real estate

The essence of the mortgage is that the borrower does not receive money, but the bank transfers it directly to the seller of the real estate.

In order for the money to be credited to the seller’s account, he needs to prepare the following list of documents:

- personal passport;

- an extract from the Unified State Register of Real Estate confirming ownership of the property (valid only for one month);

- title papers, that is, documents on the basis of which the seller received ownership rights to the object;

- cadastral passport;

- an extract from the housing office confirming that there are no debts to pay utility bills;

- conclusion of the appraised value of real estate.

Attention! If the apartment or house being sold fully or partially belongs to a minor child, then the parents cannot freely dispose of the housing. It can be sold only after receiving written permission for the transaction from the guardianship and trusteeship authorities.

Documents for registering property rights

You will have to try a lot, because... Rosreestr is very demanding about the package of papers for registering a change of right. Briefly, the list looks like this:

- Mortgage lending agreement signed by an authorized VTB employee;

- A contract for the purchase and sale of real estate, which specifies the condition of the encumbrance (pledge) of the property;

- Statement;

- Receipt for payment of state duty.

Contrary to popular belief, the transfer and acceptance certificate is completed after registration of the right, and not before registration.

When can a mortgage be collected?

After the mortgagor has fulfilled his debt obligations, VTB Bank is obliged to return the mortgage to him. The client applies to Rosreestr, where the encumbrance is removed from the mortgaged apartment. The mortgagor, who has fulfilled all the terms of the agreement, thus returns all rights to the apartment in respect of which the mortgage was drawn up.

See on the same topic: Rating of banks for mortgage lending for [y] year

From the above it follows that the debtor can pick up the mortgage in two cases:

- If he repaid the loan in full and on time;

- If the full payment of the loan was made by him ahead of schedule.

Good afternoon We bought a new building in 2020, part of the amount was taken from VTB 24.

In April 2020, we received an apartment under a transfer and acceptance certificate, and on April 19, at our own expense, we ordered an assessment of the apartment. In order not to violate the legislation of the Russian Federation, as well as the terms of the concluded Loan Agreement, on April 28, 2020, I contacted the VTB branch with a complete package of documents to prepare a mortgage. A VTB employee (in the office located at the address: Moscow, Entuziastov Boulevard, 2) accepted all the documents.

Also, an employee of VTB Bank informed me that a mortgage can be drawn up by a certain recommended notary and in response to my question: “On what basis and where is it written?”, the authorized employee said that this turns out to be our desire, and if we don’t want it, then the mortgage will be prepare 45 days (due to the high workload of VTB managers) from the date of receipt of the apartment assessment report.

To my question: “Can they provide me with a written document (justification) on the basis of which it will take so long to prepare the mortgage?” the authorized employee replied that they could not provide me with anything.

The registration options are as follows: 1. registration by a notary for 3200, the mortgage will be ready within 5 business days. days 2. The bank prepares the mortgage, but the time frame is then 1.5 months 3. You draw up the mortgage yourself, after the mortgage is submitted, the initial inspection takes 2 weeks, and then how lucky.

Also, having studied the information on the Bank’s website: www.vtb24.ru, in the “Memo to the borrower when registering ownership of an apartment acquired during the construction phase” in clause 3 “Drawing up a mortgage” it is stated that it is prepared within 3 working days from the date receipt of the assessment report and if all necessary documents are available. There is not a word in this document about notarization of the mortgage. Moreover, Law 102-FZ “On Mortgage (Pledge of Real Estate)” also does not stipulate that the mortgage must be drawn up in notarial form. I would like to note that such an unreasonable requirement as drawing up a mortgage in notarial form grossly violates my rights as a consumer of a financial service.

Considering that after registering the property with Rosreestr, the loan agreement provides for a reduced interest rate, I believe that VTB is specifically preventing the timely preparation of the mortgage (as a result of which I am not able to contact the bank to review the interest rate).

I really hope that VTB will take prompt measures to resolve this situation and, through the bank’s employees, will issue me a mortgage within 5 working days, and I am expecting a written response.

Why take out a mortgage?

A mortgage is an agreement concluded between the buyer of an apartment, who is also the borrower, and the bank that issued the mortgage for the purchase of housing. It involves the transfer of rights to the purchased property to the bank until the mortgage is fully repaid, that is, provision of the purchased property as collateral for a loan.

If the borrower does not comply with the terms of the loan agreement, VTB 24 will be able to dispose of the apartment at its discretion in order to compensate for losses incurred as a result of delays or complete refusal of payments by the client.

Registration of a mortgage with VTB 24 is a mandatory condition for taking out a mortgage. If a person refuses to sign an agreement, then the banking organization risks incurring significant losses in the event of non-payment by the client, which there is nothing to compensate for.

For a mortgage agreement, collateral in the form of the purchased apartment is necessary, and the mortgage is only a document confirming the fulfillment of this loan condition.

A mortgage note also helps the client if he loses the loan agreement, since it fully specifies all the conditions for providing a mortgage loan to a specific person by VTB 24 Bank.

This is also a guarantee that the bank will not begin to independently manage the apartment without the knowledge of the client, if he regularly complies with the terms of the mortgage specified in the document in question. If the bank wants to illegally use the property, the borrower will be able to sue and, based on the mortgage, win the case if all the necessary documents are available.

Video: