An official document that regulates the financial and property relations of the borrower and the credit institution is a mortgage agreement. Registration of the document is mandatory. It contains complete information about the subject of the agreement, the pledged property, mutual settlements between the client and the bank (or other lending organization), assigned rights, obligations, and responsibilities of the parties to the transaction.

Let us consider in detail the procedure for preparing and registering such documents after signing at the bank, as well as the information contained in mortgage lending agreements.

Types of mortgages and features of transactions

A mortgage is a convenient and quite comfortable way to improve your living conditions without long-term accumulation of savings. There is a peculiarity here - unlike consumer loans and installment plans, housing loans imply the registration of collateral, which can be purchased or owned real estate.

Agreements with financial institutions must include a detailed description of the collateral (collateral), which, in turn, significantly reduces the lender’s risks in case of non-payment of the mortgage loan or complete refusal to repay the debt.

Attention: a mortgage agreement can be drawn up by force of law - if the buyer purchases living space on a mortgage or in installments from a private person, as well as by virtue of an agreement for ordinary housing loans, which is concluded between the parties to the transaction.

Concept and form of a mortgage agreement

The basis of the document is the collateral object, which can only be real estate. The mortgage agreement clearly distributes the participants - on the one hand, the mortgagee (in a conventional loan, this is the bank), which has the right to satisfy financial claims, on the other, the borrower, who transferred the property as collateral as a guarantor of full payment of obligations.

Important! If the mortgagor has other loan agreements, the mortgagee receives priority in the distribution of income to repay the debt.

Federal Law No. 102 “On Mortgage” defines the following features of such agreements:

- the contract is concluded only in writing;

- mandatory state registration is required;

- the document gains legal force only after registration actions;

- Joint revision and changes to the initial conditions are allowed as agreed by the parties.

The document also contains information about the body that registered the mortgagee’s right to the subject of mortgage (real estate), determines the borrower’s right to use the living space during the period of settlement of contractual obligations.

Possible terms of the mortgage agreement. Subsequent mortgage

In addition to the essential conditions, the parties, at their discretion, have the right to provide for the following conditions in the DI:

- Possibility of foreclosure on the collateral out of court.

- The procedure for the sale of pledged property in the event of foreclosure on it by a court decision.

- Mortgage clause.

- Condition on the possibility of a subsequent mortgage.

IMPORTANT! If the mortgagor transfers the property into a subsequent mortgage in violation of the prohibition established by the DI, the subsequent mortgage agreement may be declared invalid by the court at the claim of the first mortgagee.

It does not matter whether the second mortgagee knew about the existence of the original DI or not. The previous mortgagee must prove that the subsequent mortgage violated his rights (see the decision of the Kuibyshevsky District Court of St. Petersburg dated October 23, 2017 in case No. 2-5811/2016).

Subject and parties of the agreement

The main element of such a document is the real estate that is pledged. Such an object is the subject of a mortgage, which must necessarily belong to the borrower (or be jointly owned). Additionally, the mortgagor’s right to live in the mortgaged property with minor children or elderly parents (and other relatives) is prescribed.

Here are the prohibitions:

- mortgaged living space is not subject to donation, bequest, or resale;

- in six out of seven cases, the mortgage does not allow registering (registering) new residents without the approval of the bank;

- It is prohibited to rent out residential property and make redevelopments.

The agreement contains complete information about the subject of the pledge - cadastral number, location address, detailed description (house, apartment), individual characteristics.

Attention: a mortgage excludes the actions of the borrower aimed at deteriorating the condition of residential real estate, which reduces its market price (liquidity level).

Regarding the obligations and rights of the parties, the document includes the following paragraphs and sections:

| For the borrower | For a financial institution (or private lender) |

| The procedure for repaying the principal debt and accrued interest in accordance with the stated rates | Procedure for compensation for failure to fulfill contractual obligations |

| Procedure for compensation for losses caused by failure to fulfill obligations | Rules and procedure for alienation of collateral in case of complete refusal to repay obligations |

| Payment of fines, accrued interest in case of violation of repayment terms, refusal to pay the mortgage | The procedure for terminating a mortgage agreement and canceling a mortgage upon full repayment of the mortgage |

| Reimbursement of legal costs when transferring debt to court | Conditions for the collection and sale of real estate during alienation |

| Payment of debt in case of misuse of funds (misappropriation) | Rules for making changes to the current mortgage agreement, issuing complete information about the property during any mortgage repayment period |

Attention: unlike an apartment, a residential building requires registration of the land plot on which the property is located as collateral. In this case, the agreement also contains information about the cadastral number, size and other characteristics of the land.

What is a subsequent mortgage?

This is a re-mortgage of real estate or other property that acts as collateral for a mortgage that has already been issued, but has not been fully repaid. The property will act as security under the new agreement.

Important! The lender can be the same bank or third-party financial institutions.

The priority of creditors is established in accordance with the records in the cadastral chamber - registration of the owner of the rights to real estate. If property is pledged, it becomes the subject of a subsequent pledge to secure new claims.

Documents required for registration of a mortgage agreement

After signing the main mortgage document, the borrower and the bank submit a joint application to the registration authority to initiate the amendment procedure. If before 2014 an agreement was registered directly, then after changes in legislation citizens record only changes in ownership rights to a certain residential property.

Termination procedure

The agreement terminates upon payment of the loan. Early termination of a mortgage agreement can occur for two reasons:

- at the initiative of the bank. Occurs when the borrower violates debt obligations. The order of such a procedure must be indicated in the text of the document;

- by mutual agreement. Termination is possible if the borrower and the bank find a compromise solution.

The agreement can also be terminated in court. In the event of repayment of the mortgage or early termination of the contract, the entry from Rosreestr is canceled subject to applications from the bank and the borrower.

Was the article helpful?

0 0

Features of a mortgage agreement

Legally, such an agreement between the borrower and the lender comes into force only after the data on the encumbrance is entered into the Rosreestr. Therefore, a loan agreement concluded with a bank by agreement of the parties can be considered preliminary.

It is important to understand that the parties to the contract are required to follow the points specified in the document.

If the borrower is largely responsible for the timely payment of the mortgage and the safety of the real estate pledged as collateral, then the financial organization receives the following obligations:

- in the absence of a mortgage, at the client’s request, execute and issue a security;

- at any time, upon request of the mortgagor, provide information on partial or complete fulfillment of contractual obligations;

- after repayment of the debt, do not interfere with the cancellation of the mortgage and the registration of the borrower’s ownership of the real estate.

Important! The mortgage document is terminated upon full fulfillment of obligations, destruction of the subject of the agreement, or sale after alienation.

Essential and additional terms of the mortgage

The mortgage loan agreement may be supplemented with other clauses, depending on the chosen financial institution. It is difficult to collect one standard sample document that would include all the necessary information and points.

However, all agreements are additionally provided with the following information:

- in the event of a threat of damage or destruction (destruction) of property, the mortgagor is obliged to inform the creditor of this fact;

- an obligation is prescribed to insure the property within 5 days (more often the insurance policy is issued simultaneously with the mortgage);

- The mortgagee has the right to inspect the condition of the property at any time throughout the entire term of the mortgage.

Attention: banking structures also have the right to request additional documents about the financial, labor or other activities of the borrower, which is also stated in the agreement.

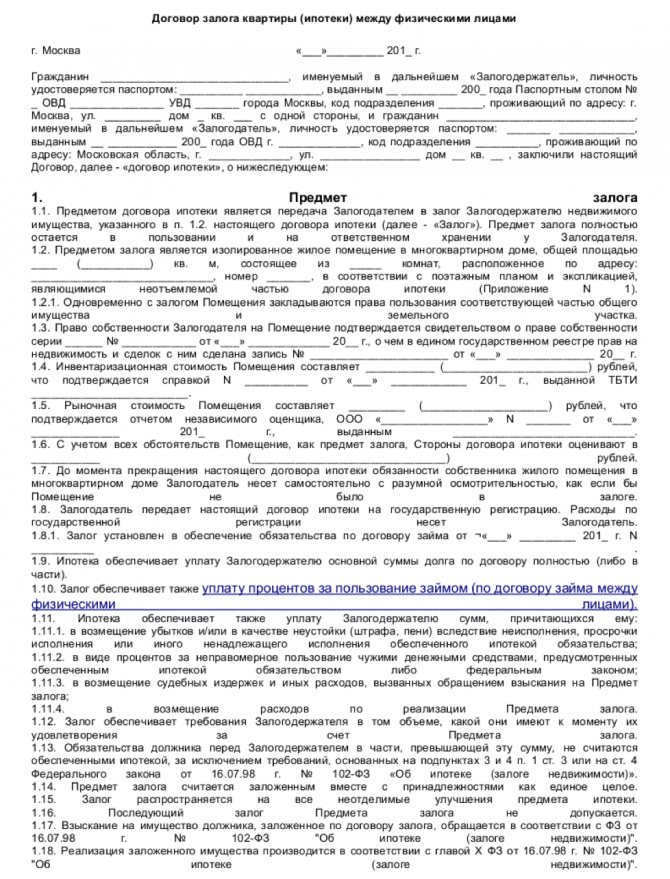

Sample mortgage agreement

The basic form of a mortgage agreement, according to the law, is as follows:

Attention: the document in any case contains information about the market and expert (estimated) value of the real estate in national currency. In the agreement, the total amount of the debt is outlined point by point: the body of the loan, interest, fees and other charges, depending on the financial institution where the loan is issued.

Mortgages in Russian banks

When choosing a loan program, you should pay attention to:

- Down payment amount;

- Credit term;

- Loan interest;

- Interest calculation scheme - classic or annuity.

Below are the conditions for mortgages from two banks - Sberbank and VTB 24:

| Criteria | Sberbank | VTB 24 | ||

| Primary housing | Secondary housing | Primary housing | Secondary housing | |

| Interest | From 10.4% (electronic registration) From 10.9% (regular rate) | From 10.25% (electronic registration) From 10.75% (regular rate) | From 10.9% | From 11.25% |

| Credit term | Up to 30 years old | Up to 30 years old | Up to 30 years old | Up to 30 years old |

| Contract fee | Absent | Absent | Absent | Absent |

| Maximum amount | 3.2 million rubles | 25 million rubles | 90 million rubles | 75 million rubles |

| Minimum amount | 300 thousand rubles | 300 thousand rubles | 600 thousand rubles | 600 thousand rubles |

| Down payment | From 15% | From 20% | From 10% | From 10% |

Many banks have the option of filling out a mortgage application online, and they even reduce the interest rate along with it.

There are some requirements for people taking out a mortgage

- Citizenship of the Russian Federation;

- Age from 18 to 60 years;

- Work in Russia;

- Residence in the Russian Federation;

- High level of income, except in some cases;

- Work experience of at least six months;

- Clean credit history.

State registration of a mortgage agreement

As we indicated above, it is not the document that is registered, but changes in property rights. That is, the fact of encumbrance is entered into Rosreestr with the transfer of property to the lender on the basis of a mortgage agreement. The simplified procedure requires a minimum package of documents, and also does not require entering information about additional agreements between the borrower and the banking institution concluded during the period of repayment of the mortgage loan.

Important! The fee must be paid whenever changes are made to the information about the property. When registering a mortgage for various properties, the fee is paid as many times as the number of properties pledged.

Mortgage by force of law

A mortgage by force of law (legal mortgage) arises as a result of the occurrence of circumstances specified in the federal law (Article 1, paragraph 2 of the Federal Law of July 16, 1998 N 102-FZ “On Mortgages”) (hereinafter referred to as Law N 102-FZ) . Such a mortgage arises exclusively with a targeted loan for the purchase of housing, and therefore its registration is necessarily accompanied by a change in the owner of the property.

In simple words : a mortgage by force of law is when an apartment purchased with credit funds is registered as the property of the buyer-borrower and when the same apartment becomes collateral for the loan taken (which is a standard scheme for providing a mortgage loan).

Example : a borrower takes out a targeted loan from a bank to purchase an apartment, which becomes collateral for this loan.

Russian legislation provides for the following grounds for the emergence of a legal mortgage:

- Mortgage of residential houses and apartments. Residential premises (residential houses and apartments) purchased or built using loan funds from a bank (or any other credit organization) are pledged to the lender from the moment of state registration of the mortgage (Clause 1, Article 77 of Law No. 102-FZ). The same applies to the purchase of land (clause 1 of Article 64.1 of Law N 102-FZ), as well as the acquisition and construction of non-residential premises (Article 69.1 of Law N 102-FZ).

- Sale on credit. Unless otherwise provided by the purchase and sale agreement, the goods sold on credit from the moment of its transfer to the buyer and until payment are recognized as pledged by the seller (clause 5 of Article 488 of the Civil Code of the Russian Federation). The same rules apply to the sale of goods on credit, with the condition of payment in installments (clause 3 of Article 489 of the Civil Code of the Russian Federation).

- Annuity (lifetime maintenance with dependents). When transferring any real estate for payment of rent, the recipient of the rent, as security for the payer’s obligation, acquires the right of pledge on this property (clause 1 of Article 587 of the Civil Code of the Russian Federation).

Registration of a mortgage by force of law

State registration of a mortgage by force of law occurs simultaneously with the registration of a purchase and sale agreement. That is, in the certificate for the apartment you purchased, in the “encumbrances” section, it will already be indicated that the housing was purchased using credit funds and cannot be sold without the consent of the lender (bank).

A legal mortgage is registered on the basis of an application from the mortgagee (borrower) or the mortgagor (creditor), or a notary who certified the agreement that led to the emergence of this type of mortgage (Clause 2 of Article 20 of Law No. 102-FZ). Read more about mortgage registration here.

Note! For state registration of a mortgage arising by force of law, no fee is charged (clause 6, clause 3, article 333.35 of the Tax Code of the Russian Federation).

Questions and answers

We gave an example of a mortgage agreement, studied all the points, but in addition we will answer the most “burning” questions of readers.

What determines the period for registering a contract?

Directly from the package of documents required to be submitted to the registration authority. If you have a mortgage and loan agreement (plus copies), a joint application with the mortgagee and a receipt, go to Rosreestr or MFC - the documents will be accepted, changes will be made within 15 days.

Is it necessary to register an agreement when purchasing under a DDU?

In this case, the sample mortgage agreement provides for a pledge of claims against the developer. That is, the equity participation agreement itself is subject to mandatory registration, otherwise it has no legal force and cannot be used as an actual claim against the residential real estate construction company.

The procedure for preparing and registering a mortgage

The typical procedure for concluding a mortgage agreement includes three steps:

- Selecting an object for mortgage lending.

- Selecting a lender bank

- Preparing a package of documents, filling out standard forms and signing an agreement.

First of all, you need to choose the property for which you want to take out a loan. Banks issue loans for the purchase of three types of objects. These are new multi-apartment buildings, properties on the secondary real estate market, as well as detached houses and townhouses. The easiest and most profitable way is to get a loan for a new building. This is due to the high degree of standardization of contract work. The objects are standard, the developers are certified, the contracts are standard.

The next step is choosing a partner bank. Write an online application to a dozen different banks. Get as many approvals as possible and carefully compare the draft agreements sent to you. Look at the pledge agreement and the subsequent mortgage agreement. Don't skip the small stuff, you're signing up for half the rest of your life.

To obtain a mortgage, the borrower must meet certain bank requirements:

- Be a citizen of the Russian Federation.

- Be between 18 and 75 years of age.

- Have a sufficient stable income.

It is important that sufficiency is assessed by the bank, and stability is the concern of only the client. All risks are on your side. If you unexpectedly lose your job, the bank won't be too upset. He has your home as collateral. He will sell this property and the fact that you have no other property will not stop the bank.

The terms of the loan depend on the bank’s credit program used, the loan term, the presence or absence of government support, and a large white salary confirmed in Form 2-NDFL. And the interest rate will decrease if you are willing to insure your life and health, if you can pay a significant down payment.

The mortgage agreement is concluded in writing. But, contrary to popular belief, a notary is not a mandatory requirement. If there is such a desire, then the parties, of course, can provide for notarization of the mortgage agreement, but the law does not insist on this. The mortgage agreement between individuals and the bank must be duly registered with the local government authority. Registration of a mortgage agreement will require the provision of a package of documents, including:

- borrower's application;

- creditor's statement;

- mortgage pledge agreement;

- mortgage loan agreement;

- receipt of payment of state duty;

The mortgage registration procedure takes up to 10 business days. The transaction is registered with a special entry in the Unified State Register of Rights to Real Estate (USRE). If an entry is not made in the Unified State Register, this means the agreement is invalid.