Summary

- In 2019, the mortgage market did not reach the record of 2018, showing a decrease in the volume of issuances by 5%, to 2.8 trillion rubles.

- At the end of 2020, the mortgage rate reached a minimum of 9%, however, from the second quarter of 2020, it is highly likely that it will begin to increase.

- The stagnation of real incomes of the population and the decline in interest rates led to an increase in the average size of a mortgage loan and the average loan term.

- The concentration of the mortgage market on state-owned banks decreased in 2020 due to a decrease in Sberbank's loans and increased lending by private players.

- In 2020, the mortgage segment is highly likely to show a decline of at least 10% due to rising rates and falling real incomes.

- The decline in economic activity amid the coronavirus and rising inflation threatens the solvency of borrowers and may lead to an increase in mortgage arrears.

- Banks and mortgage borrowers may need government support in 2020.

conclusions

After such statistics, it is quite easy to draw conclusions - mortgages are indeed becoming one of the drivers of the entire Russian economy. The growth is so significant that the question of a “mortgage bubble” involuntarily arises. A strange situation also adds fuel to the fire: in 2017, wages increased everywhere, however, the income of the population even decreased. This says one thing - we began to receive more, but we began to spend even more given the current inflation.

As for mortgages, here too the Central Bank adds its “fly in the ointment”. It turns out that such a boom in mortgage lending also caused an increase in debt on it. By January 1, 2020, Russian citizens owed 5.2 trillion rubles for mortgages , which is 15.5% more than a year ago, more than 750 billion.

However, experts also calculate such an indicator as the cost of risk of a mortgage loan. So this figure in 2017 decreased by 2 times over 2 years - in 2020 it was 1.2%, in 2017 - only 0.6%.

Numbers, numbers! Anyone setting off on this long mortgage voyage must accustom themselves to maneuvering in such “digital” waves. If you don’t know how and don’t want to learn this, then you shouldn’t even rush into the journey, trouble cannot be avoided. If you know exactly what you want, you know how to observe what is happening around you and analyze it, then feel free to “stand under the wind” while it is inflated by the “sails of state.”

Methodology

The conclusions of analysts at Expert RA JSC are based on public data, statistics from the Bank of Russia as of January 1, 2020, and the results of a survey of banks.

For the purposes of the study, residential mortgage loans mean housing loans provided in accordance with Federal Law No. 102-FZ of July 16, 1998 “On mortgage (real estate pledge).” This approach completely coincides with the methodology used by the Bank of Russia.

During the survey, we asked banks to indicate data on their mortgage loan portfolio in accordance with reporting form 0409316. Data verification was used based on calculating the compliance of the information provided with that reflected in the balance sheet (reporting form 0409101) of banks.

In total, 45 banks and the housing development financial institution JSC DOM.RF took part in the study, which, according to agency estimates, accounts for more than 99% of the mortgage market in terms of issuance volumes.

We express our gratitude to all banks for their interest in our research.

Interprogressbank

Interprogressbank offers mortgages under the following conditions:

- interest rate – from 8.25% when purchasing housing in a new building and from 8.75% when purchasing real estate on the secondary market;

- loan term – 3-30 years;

- the maximum loan amount is 20,000,0000 rubles for Moscow and the region, as well as for St. Petersburg. For the Leningrad region, a limit of 10,000,000 rubles has been established;

- The amount of the down payment is from 20% of the cost of the purchased property.

The higher the share of own funds, the lower the interest rate. If the down payment is equal to:

- 20-29%, then the rate reaches 9%;

- 30-49% - 8.75% per annum;

- more than 50% - the cost of the loan will be 8.5%.

These values increase by 0.25% when purchasing housing on the secondary market. Also, the cost of a mortgage increases by 0.7% if life and health insurance is waived and by 0.5% if income is confirmed with a bank certificate.

Business owners, including individual entrepreneurs, must provide a down payment of at least 50% of the cost of housing.

Citizens of the country over 21 years of age, but under 65 years of age, taking into account the expiration date of the contract, can apply for a mortgage. Temporary or permanent registration is required.

Experience requirements:

- general - at least 1 year;

- at the last employer - at least 6 months.

Advantages:

- if you have three or more children, the bank will provide a discount of 0.25%.

Flaws:

- the indicated rates are relevant only for participants in the “Individual Rate” program, according to the terms of which borrowers must pay a commission in the amount of 2% of the loan amount. If you refuse to participate, the cost of the loan increases by 0.5%;

- the bank operates only in the Moscow and Leningrad regions, in the cities of Moscow and St. Petersburg;

- large minimum down payment.

Results of 2020

In 2020, the market failed to reach the record values of 2018: banks issued almost 1.3 million mortgage loans totaling 2.8 trillion rubles, which is 14% less than in 2018 in quantitative terms and 5% in monetary terms. (see chart 1). The main reasons for the decline in mortgage lending include higher interest rates, which were observed during most of last year, rising real estate prices and a decrease in the volume of loans with low down payments.

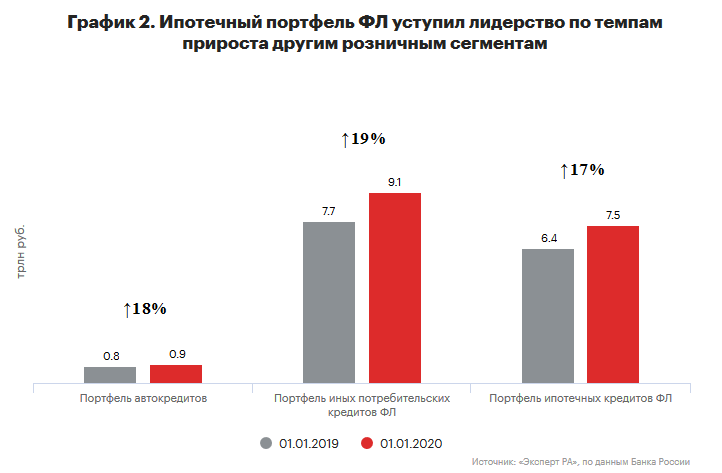

A consequence of the decrease in mortgage lending volumes was a slowdown in the growth rate of the mortgage portfolio in 2019 – to 17% versus 24% a year earlier, and the volume of total mortgage debt approached 7.5 trillion rubles as of 01/01/2020. Mortgage, which traditionally led in growth rates, gave way to other segments of retail lending in 2020 (see Chart 2). The main reasons for the active growth of unsecured consumer lending and car loans are the realization of pent-up demand from the population against the background of minimum rates in the entire history of the development of the Russian market and the increased interest of banks in retail due to the compression of other profitable segments, in particular, corporate lending. In addition, the car lending market was supported by the implementation of state programs for the purchase of cars.

At the beginning of 2019, the market observed an increase in the cost of mortgage loans after the key rate was raised again in December 2018. Despite the active reduction of rates since the summer and the minimum of 9% reached at the end of 2019 (see Chart 3), during the year the level of rates was higher than in 2018 (by an average of 0.4 percentage points) , which was one of the reasons for the slowdown in the mortgage market. We expect mortgage rates to increase in 2020: against the backdrop of rising OFZ yields and funding costs for banks due to volatility in financial markets, mortgage interest rates are likely to exceed 10% in the first half of the year.

The second reason for the weakening demand for mortgages was the increase in real estate prices. During 2020, there was an increase in the cost of both primary and secondary housing, but prices for new buildings, against the backdrop of changes in the financing mechanism for developers, grew more actively, which led to an increase in the gap in the prices of “primary” and “secondary” (see Chart 4). According to our forecasts, in the medium term, the upward dynamics of real estate prices will continue: in 2019, developers switched to bank funding and work through escrow accounts, which will lead to a gradual increase in construction costs as projects that are currently being completed are completed. old rules. In addition, the rise in prices for new buildings will be driven by increased costs for developers on imported materials and equipment due to a jump in exchange rates in 2020. Also, against the backdrop of high volatility in financial markets at the beginning of 2020, investment demand for real estate as a means of preserving savings may increase, which will support housing prices throughout the year.

Despite the more intensive growth in prices for new buildings, loans for the purchase of primary and secondary real estate showed comparable dynamics (-5%), as a result, the share of loans for the purchase of “primary” property remained at the level of a third of the lending volume. However, the agency notes that in the long term, the new mechanism for financing shared construction will increase confidence in the primary housing market, which will have a positive impact on the demand for mortgages in this segment. The “primary” market will also be supported by the gradual deterioration of the secondary housing stock and the development of lending within the framework of state programs that are focused primarily on the primary market.

Despite the continued interest of borrowers in purchasing housing in new buildings, the volume of housing commissioned in multi-apartment buildings increased slightly. In 2019, the total commissioning volume showed positive dynamics for the first time in four years (+5%) and amounted to 79.4 million sq. m. m1 (see Chart 5), however, the main contribution to the increase was made by individual housing construction (+11%, up to 35.9 million sq. m). The commissioning of housing in apartment buildings showed a slight increase (+0.5%, to 43.5 million sq. m).

In 2020, a significant increase in the volume of housing commissioning is not expected. According to Mikhail Goldberg, head of analytical, in the first half of February 2020, more than 100 million square meters were built in Russia. m of multi-apartment housing, of which about 45 million sq. m should be introduced in 2020. Another approximately 35 million sq. m in 2020 will be the volume of individual housing construction.

The situation in the construction industry remains difficult. In 2020, the volume of overdue debt of companies engaged in the construction of buildings and structures increased by 9%, and its share - from 17.3 to 21.3%. Issuance of loans to companies for the construction of buildings and structures in 2019 decreased by 9% compared to 2018. The decrease in lending volumes is due to the fact that the new project financing mechanism has not yet become fully operational and developers are still completing most projects according to the old rules. As the industry fully transitions to the new financing mechanism, it will consolidate amid the cessation of activities of small developers who will not be able to meet the tougher requirements.

Against the backdrop of a higher level of interest rates, which was observed during most of 2020, the share of issuances for refinancing mortgage loans, according to the Expert RA rating agency, decreased from 11 to 7%. Taking into account the projected increase in mortgage rates, we do not expect a recovery in demand for this product in 2020.

The rise in real estate prices in the context of stagnating real incomes of the population led to an increase in the average size of a mortgage loan - by 10% in 2020, from 2 to 2.2 million rubles. Although mortgage loans up to 3 million rubles are still the most popular among borrowers, their share in 2020 decreased significantly - from 64 to 57% of loans issued (see Chart 6). The segment of loans ranging from 5 to 10 million rubles showed significant growth in 2019 – from 11 to 14%.

Against the backdrop of an increase in the average loan size, borrowers are choosing longer loan terms in order to limit the increase in debt burden and create a comfortable repayment schedule - in 2020, the average mortgage loan term increased by 1.5, to 18.2 years. At the same time, the share of mortgage loans with a term of over 25 years increased sharply – from 12 to 17% of the volume of issues (see Chart 7).

Despite the limited effective demand of the population for mortgages, the trend towards a decrease in the size of the down payment, which was observed during 2020, ended in 2019. From January 1, 2020, the Bank of Russia re-increased risk ratios for mortgage loans with a down payment of less than 20%. A number of banks responded to this measure by introducing interest rate surcharges at the beginning of 2019 when paying less than 20% as a down payment. Although this measure did not prohibit the issuance of such loans, their attractiveness for borrowers decreased. As a result, according to the agency, the share of loans issued with a down payment of up to 20% decreased from 45 to 41% (see Chart 8).

Although there has been a general relaxation of requirements for mortgage borrowers over the past three years, in 2019 banks were less willing to issue loans to clients from low-income groups. Thus, the share of borrowers with incomes up to 30 thousand rubles decreased from 15 to 10%, and with incomes over 100 thousand rubles, on the contrary, increased from 27 to 33% (see Chart 9). This change in the structure of mortgage borrowers by income can be explained by the fact that in 2019, of the top 10 mortgage regions, only Moscow, which traditionally has a higher salary level, showed a positive increase in issuances (see Chart 12 in Appendix 1).

Mortgage rates in 2020

The following are the conditions for the main mortgage programs for 2020 by the “first five” banks:

Sberbank

| View | Sum | Term | Bid |

| Housing under construction | from 300,000 ₽ | up to 30 years old | from 8.5% |

| Secondary market | from 300,000 ₽ | up to 30 years old | from 10.2% |

| Mortgage refinancing | from 300,000 ₽ | up to 30 years old | from 10.9% |

| For families with children | up to 8,000,000 ₽ | up to 30 years old | from 6% |

| Building your own home | from 300,000 ₽ | up to 30 years old | from 11.6% |

| According to the renovation program | from 300,000 ₽ | up to 30 years old | from 10.5% |

| For the military | up to 2,502,000 ₽ | up to 20 years | 9,5% |

»» More information about mortgage rates at Sberbank.

VTB

| View | Sum | Down payment | Bid |

| New buildings | Up to 60 million rubles. | from 10% | from 9.7% |

| Secondary market | Up to 60 million rubles. | from 10% | from 9.7% |

| Refinancing | Up to 30 million rubles. | — | from 10.1% |

| Mortgage with state support for families with children | Up to 12 million rubles. | from 20% | 6% |

»» More information about mortgage rates at VTB Bank.

Gazprombank

| View | 1st installment amount | Sum | Bid |

| Housing under construction | from 10% | up to 60,000,000 ₽ | from 10.5% |

| Secondary market | from 10% | up to 60,000,000 ₽ | from 10.5% |

| Refinancing | — | up to 45,000,000 ₽ | from 10.5% |

| Mortgage with state support for families with children | from 20% | up to 8,000,000 ₽ | 6% |

»» More information about mortgage rates at Gazprombank.

Alfa Bank

| View | 1st installment amount | Term | Bid |

| Housing under construction | from 15% | up to 30 years old | from 9.99% |

| Secondary market | from 15% | up to 30 years old | from 9.99% |

| Refinancing | — | up to 30 years old | from 10.29% |

Raiffeisenbank

| View | Sum | Term | Bid |

| Housing under construction | up to 26,000,000 ₽ | up to 30 years old | from 9.99% |

| Secondary market | up to 26,000,000 ₽ | up to 30 years old | from 9.99% |

| Refinancing | up to 26,000,000 ₽ | up to 30 years old | from 9.99% |

| With maternal capital | up to 26,000,000 ₽ | up to 30 years old | from 9.99% |

At the moment, the most optimal proposals for reliability, conditions and the possibility of refinancing loans are offered by the first “state construction” : Sberbank, VTB and Gazprombank.

Private Alfa-Bank offers an average market rate , but very carefully checks a potential client, periodically requesting additional documents - which is often inconvenient for nonresidents.

Raiffeisenbank is more flexible in terms of its rate policy, but does not provide the opportunity to take out a loan for a larger amount , unlike its competitors. Raiffeisenbank will only be able to borrow up to 26 million rubles.

The checks are also quite strict. Raiffeisenbank has always been highly suspicious even with debit accounts.

Other banks often attract clients with regional preferential programs, which need to be monitored separately.

For example, even Alfa-Bank (a federal bank) strictly limits the maximum loan amounts for Moscow, St. Petersburg (and their regions) and for the rest of Russia - 8 and 3 million rubles, respectively.

»» More information about loans from Alfa-Bank.

Market participants and competition

The dynamics of mortgage issuance by banks from the top 20 at the end of 2020 varied significantly - from an almost twofold drop in lending volumes to an increase of more than three times (see Chart 14 in Appendix 1). The highest growth rate was shown by Alfa-Bank (+203%), which allowed it to enter the top five, moving from 11th to 4th position in the ranking (see Table 1). Promsvyazbank (+138%) and FC Otkritie Bank (+118%) showed more than double growth in mortgage issuances.

In 2019, there was a decrease in the total volume of mortgage issues from state-owned banks (see Chart 10), mainly due to a reduction in lending to the market leader, Sberbank. At the same time, against the backdrop of increased lending by private banks, there was a decrease in the concentration of the mortgage market on players with state participation - their share in loans decreased from 87.5 to 85.1%.

Where do optimistic forecasts come from?

The information provided by analysts is very reasonable. It is planned that the mortgage rate in the future will be about 6%. Only a sharp economic downturn can have a negative impact on this, but the likelihood of this is quite low. The Central Bank will also reduce the cost of mortgages, the indicators will drop below 10%.

The main players in this field will be directly interested in increasing the volume of issued credit funds through the most favorable terms of cooperation. Naturally, the population will react positively to this state of the economy.

Considering the current state of affairs, we note that in 2020, mortgage lending indicators will be better than before the crisis, even without government support. This is why, obviously, a considerable number of families will decide to take out a mortgage in 2020. A very important role will be played by the growth of incomes of the country's citizens, as well as a decrease in interest rates on loans.

Consumer mood may worsen due to changes in information about the economic crisis. Of course, in this case the volume of housing purchased with a mortgage will change. But once the crisis passes, many people are again willing to begin solving their housing problems, and accordingly, they will be able to take on obligations in the long term.

Forecasts promise to be optimistic

In fact, experts say that there is a certain risk of such an approach to buying houses or apartments in 2020, despite the fact that mortgages with state support are becoming available to virtually everyone.

Table 1. Ranking of banks by volume of mortgage lending in 2019

Open table in new window

Swipe across table

| Place in the ranking based on the results of 2020 | Place in the ranking based on the results of 2020 | Name of the bank | License number | Rating from "Expert RA" as of March 15, 2020 | Volume of issued mortgage housing loans, million rubles. | Growth rate (2019 / 2020), % | |

| 2019 | 2018 | ||||||

| 1 | 1 | PJSC Sberbank | 1 481 | — | 1 285 046 | 1 562 017 | -17.7 |

| 2 | 2 | VTB Bank (PJSC) | 1 000 | ruAAA | 675 440 | 672 292 | 0.5 |

| 3 | 3 | Bank GPB (JSC) | 354 | ruAA+ | 106 068 | 149 986 | -29.3 |

| 4 | 11 | JSC "ALFA-BANK" | 1 326 | ruAA | 91 763 | 30 321 | 202.6 |

| 5 | 9 | PJSC Bank "FC Otkritie"* | 2 209 | ruAA- | 91 699 | 42 123 | 117.7 |

| 6 | 4 | JSC Rosselkhozbank | 3 349 | — | 89 251 | 128 004 | -30.3 |

| 7 | 6 | PJSC ROSBANK** | 2 272 | ruAAA | 76 625 | 72 017 | 6.4 |

| 8 | 13 | PJSC Promsvyazbank | 3 251 | ruAA- | 64 263 | 26 972 | 138.3 |

| 9 | 5 | DOM.RF Group*** | 2 312 | ruA | 61 242 | 61 245 | -0.0 |

| 10 | 7 | JSC Raiffeisenbank | 3 292 | ruAAA | 58 074 | 63 441 | -8.5 |

| 11 | 8 | JSCB "Absolut Bank" (PJSC) | 2 306 | ruBBB- | 51 890 | 48 103 | 7.9 |

| 12 | 10 | PJSC "BANK URALSIB" | 2 275 | — | 29 510 | 30 533 | -3.4 |

| 13 | 12 | Bank "Vozrozhdenie" (PJSC) | 1 439 | ruA- | 25 405 | 28 768 | -11.7 |

| 14 | 14 | PJSC "Bank" Saint-Petersburg" | 436 | ruA- | 23 505 | 24 152 | -2.7 |

| 15 | 20 | PJSC JSCB "Svyaz-Bank" | 1 470 | ruA+ | 12 528 | 8 937 | 40.2 |

| 16 | 15 | PJSC "AK BARS" BANK | 2 590 | ruA- | 12 495 | 23 199 | -46.1 |

| 17 | — | PJSC "CREDIT BANK OF MOSCOW" | 1 978 | ruA | 10 557 | 8 445 | 25.0 |

| 18 | 18 | TKB BANK PJSC | 2 210 | — | 10 458 | 10 939 | -4.4 |

| 19 | 16 | PJSC CB "Center-invest" | 2 225 | — | 9 345 | 14 108 | -33.8 |

| 20 | 22 | JSC AB RUSSIA | 328 | ruAA | 7 852 | 6 859 | 14.5 |

| 21 | 17 | JSC "SMP Bank" | 3 368 | ruA- | 7 499 | 13 039 | -42.5 |

| 22 | 21 | PJSC SKB Primorye "Primsotsbank" | 2 733 | ruBBB+ | 6 502 | 7 188 | -9.5 |

| 23 | — | Bank "RRB" (JSC) | 3 287 | ruAA | 5 297 | 5 097 | 3.9 |

| 24 | 23 | Bank "Levoberezhny" (PJSC) | 1 343 | ruA- | 4 733 | 5 713 | -17.2 |

| 25 | 24 | CB "Kuban Credit" LLC | 2 518 | — | 3 557 | 4 029 | -11.7 |

| 26 | — | PJSC "MTS-Bank" | 2 268 | ruBBB+ | 3 456 | 2 759 | 25.3 |

| 27 | 30 | Bank "KUB" (JSC) | 2 584 | ruA+ | 2 291 | 2 413 | -5.1 |

| 28 | 27 | PJSC "CHELINDBANK" | 485 | ruA+ | 2 289 | 2 488 | -8.0 |

| 29 | 28 | "Asian-Pacific Bank" (PJSC) | 1 810 | — | 2 269 | 2 600 | -12.7 |

| 30 | 29 | PJSC KB "UBRD" | 429 | — | 2 077 | 2 448 | -15.2 |

| 31 | 25 | PJSC "BANK SGB" | 2 816 | ruA- | 1 574 | 3 408 | -53.8 |

| 32 | 31 | PJSC JSCB "Ural FD" | 249 | ruBBB- | 1 542 | 2 254 | -31.6 |

| 33 | 34 | PJSC "CHELYABINVESTBANK" | 493 | ruA | 1 456 | 1 221 | 19.3 |

| 34 | 33 | JSCB "Investtorgbank" (PJSC) | 2 763 | — | 1 330 | 1 466 | -9.3 |

| 35 | 32 | LLC Bank "Avers" | 415 | ruA- | 1 043 | 1 671 | -37.6 |

| 36 | — | JSC "TATSOTSBANK" | 480 | ruBB+ | 911 | 926 | -1.6 |

| 37 | 35 | JSCB "Almazergienbank" JSC | 2 602 | ruBB | 900 | 1 153 | -21.9 |

| 38 | 40 | "SDM-Bank" (PJSC) | 1 637 | ruA- | 549 | 470 | 16.9 |

| 39 | 38 | JSCB "Energobank" (JSC) | 67 | — | 516 | 609 | -15.3 |

| 40 | 42 | JSC "PERVURALSBANK" | 965 | ruBB- | 315 | 273 | 15.4 |

| 41 | 43 | JSC "NS Bank" | 3 124 | ruB | 285 | 241 | 18.4 |

| 42 | 41 | JSC "Databank" | 646 | ruBB- | 250 | 340 | -26.5 |

| 43 | 44 | JSCSB "KS BANK" (PJSC) | 1 752 | ruB- | 118 | 141 | -16.8 |

| 44 | — | KB "Novy Vek" (LLC) | 3 417 | ruB | 111 | 41 | 167.3 |

| 45 | 45 | LLC "Zemsky Bank" | 2 900 | — | 94 | 65 | 43.2 |

| Source: “Expert RA”, based on the results of a survey of banks | |||||||

| * Hereinafter: the data is given taking into account PJSC B&N Bank, which in 2020 was merged with PJSC Bank FC Otkritie | |||||||

| ** Hereinafter: the data is indicated taking into account JSC Commercial Bank DeltaCredit, which in 2020 was merged with PJSC ROSBANK | |||||||

| *** Hereinafter: the DOM.RF group includes JSC "Bank DOM.RF" and JSC "DOM.RF" | |||||||

At what interest rates do Russian banks give mortgages in 2020?

Mortgage interest rates of rating Russian banks for the purchase of finished and under construction housing

| Name of the bank | % rate for the purchase of finished housing with a mortgage (% per annum) | % rate for the purchase of housing under construction with a mortgage (% per annum) |

| Sberbank | 11-12,6 | 8,8-12,1 |

| VTB | 10,1-12,1 | 10,1-12,1 |

| Rosselkhozbank | 9,75-12,75 | 9,3-12,4 |

| Gazprombank | 9,5-9,8 | 9,5-10,8 |

| Raiffeisenbank | 9,9-11 | 9,9-11 |

| "Absolut Bank | 11,75-16 | 11,75-16 |

| Bank opening" | 9,6-11,9 | 9,6-11,9 |

| Bank "Uralsib" | 10,7-11,9 | 10,3-11,5 |

*both in the primary and secondary real estate markets (approximate values). The exact terms of the loan must be clarified with each specific bank in more detail.

Market development forecast

In 2020, the Russian mortgage market may come under pressure amid slowing economic growth and inflation risks due to falling oil prices and the coronavirus pandemic. Due to significant uncertainty in the market, the agency is considering three scenarios for its development: positive, moderately negative and crisis.

The positive scenario of the Expert RA rating agency assumes that an agreement on oil production volumes will be reached in a short time, and a jump in exchange rates in March will not lead to a significant increase in inflation risks. As a result, changes in the monetary policy of the Bank of Russia will occur only in terms of suspending the cycle of reducing the key rate, but will not lead to its growth. If this scenario is implemented, the volume of mortgage issuance at the end of 2020 could increase by 10–15% and reach 3.1–3.2 trillion rubles, and the weighted average rate could decrease to 8.5% by the end of 2020. The main contribution to the reduction in the average rate will be made by the development of lending within the framework of state programs, the rates for which are in the range of 2–5%. Market support factors in this scenario will be a gradual reduction in rates and the development of lending within the framework of government programs. At the same time, the possible introduction of personal income tax for mortgage loans and rising real estate prices may have a negative impact on the market.

We consider the most likely scenario to be a moderately negative one, which assumes that in 2020 there will be an increase in inflation above the target of 4% per annum and, as a consequence, an increase in the key rate to 7–7.5%. We consider its implementation likely at an average annual price of Brent oil of 40–45 US dollars per barrel. The volume of mortgage issuances in this case will be lower than last year’s values by 10–12% and will amount to 2.5–2.6 trillion rubles (see Chart 11). The main negative impact on the volume of loans will be from an increase in mortgage rates to 10% per annum and a decrease in real incomes of the population. In 2020, banks will face serious challenges in managing the quality of their mortgage portfolio, associated with a decrease in the solvency of the population against the backdrop of a general economic downturn and rising prices, as well as job cuts in a number of industries most susceptible to the impact of coronavirus. Risks in retail, which have been actively growing over the past two years, will be superimposed on the negative impact of negative revaluation of securities and the deterioration in the financial position of corporate clients on the quality of banks’ assets. The agency expects an increase in the volume of overdue mortgage debt within the range of 5–10% during the year, but its share will not exceed 1.5% of the portfolio. At the same time, in the next two to three years, a more significant increase is possible due to some of the borrowers who received loans during the mortgage boom going into default. However, the quality of the portfolio will be supported by the introduction into law, starting in 2020, of the possibility of mortgage holidays for borrowers who find themselves in difficult life or financial situations, which in the long term will increase confidence in mortgages in general.

The crisis scenario of the Expert RA rating agency assumes a significant deepening of negative phenomena in the economy, the absence of new agreements on the OPEC+ deal, a drop in the average annual oil price to $35 per barrel, a refusal of foreign exchange interventions by the Central Bank and a significant depreciation of the ruble, an increase in inflation to 7– 8% at the end of the year. With this development of events, the key rate will increase to 9–10%, and mortgage rates will approach 12%. Banks will increase requirements for new borrowers (limiting or stopping lending to customers off the street, increasing down payment requirements), and the demand for mortgage loans will decrease significantly. If the crisis scenario is realized, the volume of mortgage issuances will fall by 20–25% and amount to 2.1–2.2 trillion rubles. With this development, the state can offer preferential lending programs for a wide range of borrowers, similar to the rate subsidy program in 2015–2016 to maintain the level of issuances. This scenario also assumes a fall in real household incomes, which will put pressure on the solvency of borrowers and could lead to an increase in overdue debt in the portfolio by more than 10% in 2020.

Maximum mortgage interest

As for the maximum mortgage percentages, which you really don’t want to fall into. Here you need to proceed from the minimum ones already given. In any case, the maximum is those offers that you will not agree to, this is just food for thought and an impetus for further searches.

Here are some of these types of proposals:

- 13.35% - Tinkoff Bank - here 100 million rubles for a new apartment for 20 years, but this is an independent offer from the bank, no partners, and now the entire business basis of the enterprise of the former owner of a professional cycling team from the world's best twenty is clear. The down payment is 10%, but no proof of income is required.

- 11.25% - DeltaCredit Bank - mortgage on a separate house, but the down payment is not less than 40%.

- 10.25% - also Tinkoff Bank - for 25 years with a 20% down payment, a separate new house.

Strictly speaking, what we need to proceed from when determining the maximum percentage is the latest information from the Central Bank, which at the beginning of February 2018 issued a press release about the achievements of mortgages in 2017.

So:

If in 2016 the average percentage in December was 11.54%, then in December 2017 it was already 9.79%.

In 2017, the volume of mortgage loans issued increased by 37.2% and amounted to more than 2 trillion rubles.

In total, 1 million 100 thousand loans were issued.

Moreover, what’s interesting is that the whole year the “swell” of mortgages only grew, and in December it reached its apogee - 151 thousand loans were issued in the amount of more than 290 billion rubles. For comparison, in December 2016, 103 thousand loans were issued for 184 million.

Market support measures

Taking into account the threats to the solvency of the population due to a decrease in economic activity and rising inflation amid the risks of the spread of coronavirus infection and falling oil prices, the mortgage market may require government support. These measures should concern both existing mortgage borrowers who may face financial difficulties, and support for future issues when interest rates rise and banks tighten their risk policies in turbulent conditions.

Thus, if the coronavirus pandemic spreads to Russia, the mortgage holiday mechanism in force since 2020 will need to include additional opportunities for those citizens whose income has decreased due to the infectious situation, in particular, due to a long stay in quarantine, sick leave in case of infection with the virus or suspension of activity/bankruptcy of the borrower’s employer due to the pandemic. At particular risk are borrowers employed in industries most affected by the pandemic (tourism, air travel, services and entertainment), as well as those working unofficially or receiving “gray” salaries, which will not allow them to fully rely on compensation from the employer in case of illness or quarantine. In addition, if citizens are in arrears due to the current force majeure situation, it is important to prevent their credit history from deteriorating so as not to limit access to borrowed funds in the future. In turn, for banks, which in 2020 will have to face a decline in the quality of almost all types of assets, it is important to provide a mechanism for deferring the formation of reserves for loans to borrowers whose financial situation has worsened due to the pandemic.

Along with measures to assist borrowers, there may be a need to support the mortgage market as a whole in order to maintain citizens’ access to improved housing conditions. The most likely mechanism, which worked well during the last crisis of 2015–2016, is a state program to subsidize mortgage rates for a wide range of borrowers purchasing apartments on the primary market. Its implementation will also help support the construction market, which will be under pressure due to a possible increase in lending rates by banks and rising prices for imported materials and equipment.

Mortgage - primary housing, Sberbank

The primary real estate market is the name given to housing that is located in new buildings or houses under construction. New buildings in Moscow are quite an expensive purchase, and it is very difficult to save up for it. This explains the consistently high demand for mortgage lending.

In relation to real estate on the primary market, Sberbank of the Russian Federation offers mortgages with a rate of 7.4 percent. On the website of the credit institution you can study the list of developers participating in the subsidy program. These construction organizations have been inspected by the Russian Security Service and have proven themselves to be reliable partners. This reduces the risk of losing your investment to almost a minimum. The main advantages of purchasing apartments on the primary market with a mortgage loan from Sberbank:

- the possibility of purchasing completed and not yet commissioned housing;

- You can invest money in purchasing real estate of a higher level of comfort. The cost of apartments in a building under construction can be equal to the price of an apartment on the secondary real estate market. The only limitation is waiting for the facility to be put into operation;

- a SB client can buy real estate with a mortgage without reference to the deadline for its delivery;

- the possibility of making mutual settlements on loans using letters of credit.

Among the conditions of mortgage programs regarding housing in the primary market, it is worth noting the possibility of a phased transfer of funds: the amount required for issuance to the borrower is divided into 2 parts: the first is transferred immediately after the conclusion of the DDU (equity agreement), the second - no later than 2 years from the date of transfer of the first tranche, necessarily before signing the deed of transfer of real estate. The timing of money transfers is prescribed in the DDU.

A mortgage for living space in a new building or a facility under construction is issued in the national currency of the Russian Federation (rubles), relative to the loan amount - from 300,000 rubles, the issuance limit is 85% of the agreed value. Moreover, this cost is an assessment of the apartment by independent experts. The duration of mortgage lending is from 5 (on general terms) to 7 (subsidy programs) years. Down payment - starting from 15% if the borrower provides a certificate of income and from 50% - in the absence of this document. Sberbank does not charge a fee for issuing a mortgage.

Security for a mortgage loan can be:

- pledge on the real estate being loaned or owned;

- during the period of registration of a pledge for the housing space being financed, a guarantee from a spouse or another individual, or a pledge of property will be required;

- In the case of a private house being pledged, the land plot under this object becomes a measure of guarantee.

Mortgage loans contain a mandatory condition for insuring all collateral property; only land plots are not insured against the risks of loss.

Important: if Sberbank makes a positive decision on the mortgage, the borrower must submit documentation for the purchased property to the Bank’s credit department within 3 months

Table 2. Ranking of banks by mortgage portfolio size as of 01/01/2020

Open table in new window

Swipe across table

| Place in the ranking as of 01/01/2020 | Place in the ranking as of 01/01/2019 | Name of the bank | License number | Rating from "Expert RA" as of March 15, 2020 | Portfolio volume (balance of debt), million rubles. | Growth rate (2019 / 2020), % | |

| 01.01.2020 | 01.01.2019 | ||||||

| 1 | 1 | PJSC Sberbank | 1 481 | — | 4 072 001 | 3 621 970 | 12.4 |

| 2 | 2 | VTB Bank (PJSC) | 1 000 | ruAAA | 1 685 253 | 1 403 912 | 20.0 |

| 3 | 3 | Bank GPB (JSC) | 354 | ruAA+ | 383 941 | 348 912 | 10.0 |

| 4 | 4 | JSC Rosselkhozbank | 3 349 | — | 273 184 | 242 625 | 12.6 |

| 5 | 5 | DOM.RF Group | 2 312 | ruA | 231 698 | 213 186 | 8.7 |

| 6 | 6 | PJSC ROSBANK | 2 272 | ruAAA | 203 403 | 181 873 | 11.8 |

| 7 | 11 | PJSC Bank "FC Otkritie" | 2 209 | ruAA- | 160 817 | 84 654 | 90.0 |

| 8 | 7 | JSC Raiffeisenbank | 3 292 | ruAAA | 140 713 | 117 565 | 19.7 |

| 9 | 16 | JSC "ALFA-BANK" | 1 326 | ruAA | 111 417 | 35 495 | 213.9 |

| 10 | 14 | PJSC Promsvyazbank | 3 251 | ruAA- | 95 972 | 45 280 | 112.0 |

| 11 | 8 | JSCB "Absolut Bank" (PJSC) | 2 306 | ruBBB- | 89 890 | 82 289 | 9.2 |

| 12 | 10 | PJSC "BANK URALSIB" | 2 275 | — | 74 855 | 69 899 | 7.1 |

| 13 | 9 | PJSC JSCB "Svyaz-Bank" | 1 470 | ruA+ | 71 472 | 75 062 | -4.8 |

| 14 | 12 | Bank "Vozrozhdenie" (PJSC) | 1 439 | ruA- | 64 412 | 41 327 | 55.9 |

| 15 | 13 | PJSC "Bank" Saint-Petersburg" | 436 | ruA- | 57 561 | 49 679 | 15.9 |

| 16 | 15 | PJSC "AK BARS" BANK | 2 590 | ruA- | 46 005 | 43 077 | 6.8 |

| 17 | 18 | PJSC CB "Center-invest" | 2 225 | — | 34 665 | 32 738 | 5.9 |

| 18 | — | PJSC "CREDIT BANK OF MOSCOW" | 1 978 | ruA | 24 647 | 21 682 | 13.7 |

| 19 | 21 | JSC "SMP Bank" | 3 368 | ruA- | 20 944 | 17 711 | 18.3 |

| 20 | 22 | JSC AB RUSSIA | 328 | ruAA | 17 436 | 13 746 | 26.8 |

| 21 | 20 | TKB BANK PJSC | 2 210 | — | 12 235 | 14 859 | -17.7 |

| 22 | 23 | CB "Kuban Credit" LLC | 2 518 | — | 11 468 | 10 097 | 13.6 |

| 23 | — | Bank "RRB" (JSC) | 3 287 | ruAA | 11 394 | 8 503 | 34.0 |

| 24 | — | PJSC "MTS-Bank" | 2 268 | ruBBB+ | 10 284 | 10 349 | -0.6 |

| 25 | 24 | Bank "Levoberezhny" (PJSC) | 1 343 | ruA- | 7 574 | 6 042 | 25.3 |

| 26 | 25 | Bank "KUB" (JSC) | 2 584 | ruA+ | 6 401 | 5 474 | 16.9 |

| 27 | 27 | PJSC SKB Primorye "Primsotsbank" | 2 733 | ruBBB+ | 6 322 | 5 311 | 19.0 |

| 28 | 26 | PJSC "BANK SGB" | 2 816 | ruA- | 5 740 | 5 397 | 6.4 |

| 29 | 28 | PJSC "CHELINDBANK" | 485 | ruA+ | 5 625 | 4 721 | 19.1 |

| 30 | 30 | PJSC JSCB "Ural FD" | 249 | ruBBB- | 4 956 | 4 529 | 9.4 |

| 31 | 33 | PJSC KB "UBRD" | 429 | — | 4 952 | 3 649 | 35.7 |

| 32 | 31 | LLC Bank "Avers" | 415 | ruA- | 4 420 | 4 415 | 0.1 |

| 33 | 29 | JSCB "Investtorgbank" (PJSC) | 2 763 | — | 4 121 | 4 052 | 1.7 |

| 34 | 32 | JSCB "Almazergienbank" JSC | 2 602 | ruBB | 3 901 | 3 861 | 1.1 |

| 35 | 34 | PJSC "CHELYABINVESTBANK" | 493 | ruA | 2 858 | 2 400 | 19.1 |

| 36 | — | JSC "TATSOTSBANK" | 480 | ruBB+ | 1 754 | 1 117 | 57.0 |

| 37 | 37 | "SDM-Bank" (PJSC) | 1 637 | ruA- | 1 444 | 1 339 | 7.8 |

| 38 | 38 | JSCB "Energobank" (JSC) | 67 | — | 1 283 | 1 151 | 11.5 |

| 39 | 40 | "Asian-Pacific Bank" (PJSC) | 1 810 | — | 991 | 1 052 | -5.9 |

| 40 | 42 | JSC "NS Bank" | 3 124 | ruB | 598 | 519 | 15.2 |

| 41 | 41 | JSC "Databank" | 646 | ruBB- | 491 | 546 | -10.0 |

| 42 | 43 | JSCSB "KS BANK" (PJSC) | 1 752 | ruB- | 352 | 276 | 27.2 |

| 43 | 45 | JSC "PERVURALSBANK" | 965 | ruBB- | 286 | 189 | 51.7 |

| 44 | 46 | LLC "Zemsky Bank" | 2 900 | — | 113 | 114 | -0.6 |

| 45 | — | KB "Novy Vek" (LLC) | 3 417 | ruB | 96 | 81 | 19.0 |

| Source: “Expert RA”, based on the results of a survey of banks | |||||||

"RosEvrobank"

RosEvrobank is another lender that offers a minimum interest rate on mortgages. Its conditions:

- interest rate – from 8.75%;

- down payment – from 15% of the cost of the purchased property;

- maximum loan amount – 20,000,000 rubles;

- minimum loan size – 500,000 rubles;

- loan term – 1-20 years.

Requirements for borrowers:

- age – 23-65 years;

- The minimum length of service at your last place of employment is 4 months.

Advantages:

- to increase the loan amount, you can provide additional security in the form of a guarantee from both individuals and legal entities, as well as a pledge of securities;

- there is an opportunity to save on the final amount of payments - if you pay the bank from 1.5% to 4% of the loan amount, you can reduce the mortgage rate from 0.5% to 1.5%;

- You can refuse life insurance, insurance against the risk of loss of the collateral, but then the cost of the loan increases.

Flaws:

- restrictions on the minimum mortgage amount and the term of the contract;

- the bank operates only in the Moscow region;

- settlement of loan obligations is carried out free of charge at the offices of RosEvrobank. Many friendly merchants also accept payments, but they charge a fee.

Appendix 2. Interviews with market participants

Mikhail Anatolyevich Goldberg, head of analytical

– How do you assess the impact on the mortgage market of developers switching to working through escrow accounts? Do you expect the price per square meter to increase due to changes in the mechanism for financing housing construction and, if so, by how much?

– The transition of housing construction to project financing from July 1, 2020 made it possible to completely remove all risks from the home buyer. According to a survey conducted by VTsIOM, commissioned by DOM.RF, the presence of guarantees for the return of funds or the completion of a house increased the population’s demand for housing under construction by a third. Under these conditions, the demand for mortgage loans for the purchase of housing in new buildings will also increase.

The new model allows developers to receive bank financing for construction at lower rates. In particular, the special rate on project financing loans secured by citizens' funds in escrow accounts is about 3–4%. At the same time, developers do not need to pay a contribution to the Fund for the Protection of the Rights of Citizens - Participants in Shared Construction. As a result, the overall increase in housing costs is estimated at no more than 2–3%.

At the same time, there was no jump in housing prices during the transition to project financing. According to the Fund for the Protection of the Rights of Citizens - Participants in Shared Construction, the median cost of 1 sq. m. m of housing at the end of the year amounted to 70 thousand rubles, which is approximately 10% higher than at the beginning of the second quarter of 2020, before the transition to project financing. It is important to note that between 2020 and 2018 house prices fell by 16% in real terms (net of inflation). With such dynamics, the investment attractiveness of the housing construction market is decreasing, and therefore a slight increase in prices in 2020 is positive news.

– What volume of project financing does the bank plan to provide to developers in 2020?

– 1 trillion rubles of signed contracts as a cumulative total by the end of the year.

– What is your assessment of the dynamics of housing delivery on the market in 2020–2021? What factors, in your opinion, can increase the pace of housing commissioning?

– According to Rosstat estimates, in 2020, housing commissioning in the country amounted to 80.3 million square meters. m (+6.1% compared to the previous year). According to the Unified Information System of Housing Construction (nash.dom.rf), in the first half of February 2020, more than 100 million square meters were built in the country. m of multi-apartment housing, of which about 45 million sq. m should be introduced in 2020. Another approximately 35 million sq. m in 2020 will be the volume of individual housing construction.

The main factor in increasing construction volumes is the high demand of the population for housing. According to a survey conducted by JSC "DOM.RF" together with VTsIOM in 2020, more than 45% of Russian families need to improve their living conditions. Mortgage is the main market method of purchasing housing in new buildings: more than 50% of transactions are concluded with its help. Effective demand for housing with a mortgage will be supported by record low rates, which for the first time in history dropped below 9%. Various government support measures will also contribute to the growth in demand. The most important place among them is occupied by maternity capital, which can be invested in the purchase of housing. The expansion of this program at the proposal of the President of the Russian Federation V.V. Putin (extending it to first-born children, as well as increasing the payment for the second child by 150 thousand rubles) will affect 1.3 million Russian families annually. According to estimates by JSC DOM.RF, the contribution of this measure to the increase in demand for housing will be up to 6 million square meters. m per year.

Another effective instrument of state support is a mortgage program for families with two or more children, which allows you to obtain a mortgage at a preferential rate of 5%, and at the DOM.RF bank - at 4.7% (“Family Mortgage”). In general, taking into account the increased maternity capital, the total amount of state support that a Russian family with two children can count on today exceeds 2 million rubles. This is 40% of the total costs of purchasing an average apartment with a mortgage on market conditions. This amount takes into account tax deductions for the purchase of an apartment and interest payments, maternity capital, as well as savings due to a preferential mortgage interest rate of 5%.

Servicing a standard mortgage loan is now available to approximately 50% of Russian families. It is necessary to work out mechanisms for providing housing to citizens with low incomes who cannot purchase real estate as their own. The need for the construction of such housing, according to our estimates, is at least 30–40 million square meters. m.

– Do you consider it necessary to introduce the calculation of personal income tax on mortgage loans? How much impact do you think this innovation will have on the market if implemented? What alternatives to introducing PDN could the regulator use to avoid the formation of a “bubble” in the market?

– Mortgage remains the highest quality segment of lending to individuals: as of December 1, 2019, the share of loans with overdue payments of more than 90 days, according to the Bank of Russia, was less than 1.4%. The share of other loans to individuals overdue for more than 90 days was 7%. The transition to assessing the borrower's debt burden will further improve the quality of mortgage loans, however, when introducing it, it is necessary to take into account the practice of banks in assessing the creditworthiness of borrowers.

– Do you consider it necessary to extend the current state program of preferential mortgages for families with two or more children to purchase housing on the secondary market?

– The most important priorities for the development of the housing sector in Russia are to increase the volume of housing construction and radically improve the comfort of the urban environment. The construction of new housing solves these two problems simultaneously, since houses are built in compliance with modern standards of quality and infrastructure. After the transition to a new model of financing housing construction, the rights of citizens buying housing on the primary market are fully protected. Purchasing housing on the secondary market still carries risks of loss of ownership due to unlawful actions of third parties, and there is a risk of fraud. It is not practical to distribute the program to the secondary market.

Demand for mortgages will continue

Despite the upcoming changes, the demand for mortgages will remain, experts are sure. It depends on the solvency of the population, the situation on the real estate market, the attractiveness and availability of housing loans.

“Yes, on the one hand, there is a demographic decline (borrowers-buyers born in the 90s are entering the market). On the other hand, this generation has a stronger desire for more comfortable housing. So one factor is compensated by another,” says the editor-in-chief of Finversia.ru, expert of the State Duma Committee on the Financial Market, member of the Council of the SPKFR, the Banking Commission of the Russian Union of Industrialists and Entrepreneurs, the Expert Council of the AFD, Ph.D. Jan Art.

In his opinion, neither rate cuts nor subsidies will fundamentally change the demand for mortgages. Only one thing can change it: when Russians earn on average more per month than the cost of one meter of housing in the city where they live. “Everything else is deceit. If you can’t afford a loan of 5 million, then it doesn’t matter so much to you whether they are willing to give you that 5 million at 7% or at 10%. You won’t take him one way or another,” says Art.

Deputy Chairman of the Board of TATSOTSBANK JSC Dmitry Kuznetsov notes that the demand for mortgages is only growing every year. “And it will continue to grow,” the expert believes. — Now there are borrowers who have two mortgages taken out at the same time; many, after paying off the mortgage, take out the next one. There will always be a demand for improving living conditions.”