An affordable mortgage with a bank certificate is an excellent alternative for citizens whose employer pays part of their salary in an envelope. To approve the application, the borrower must confirm a high level of monthly income. A free-form certificate or a bank-type certificate issued by a business owner or accountant allows you to do this informally without taking into account tax payments.

Required papers

A mortgage is a long-term loan that carries many risks for the bank. Therefore, to ensure the client's ability to repay the debt, financial institutions request an income certificate . Requirements for this document may vary from bank to bank and depending on the mortgage program. Let's look at what certificates banks accept for mortgages and in what forms.

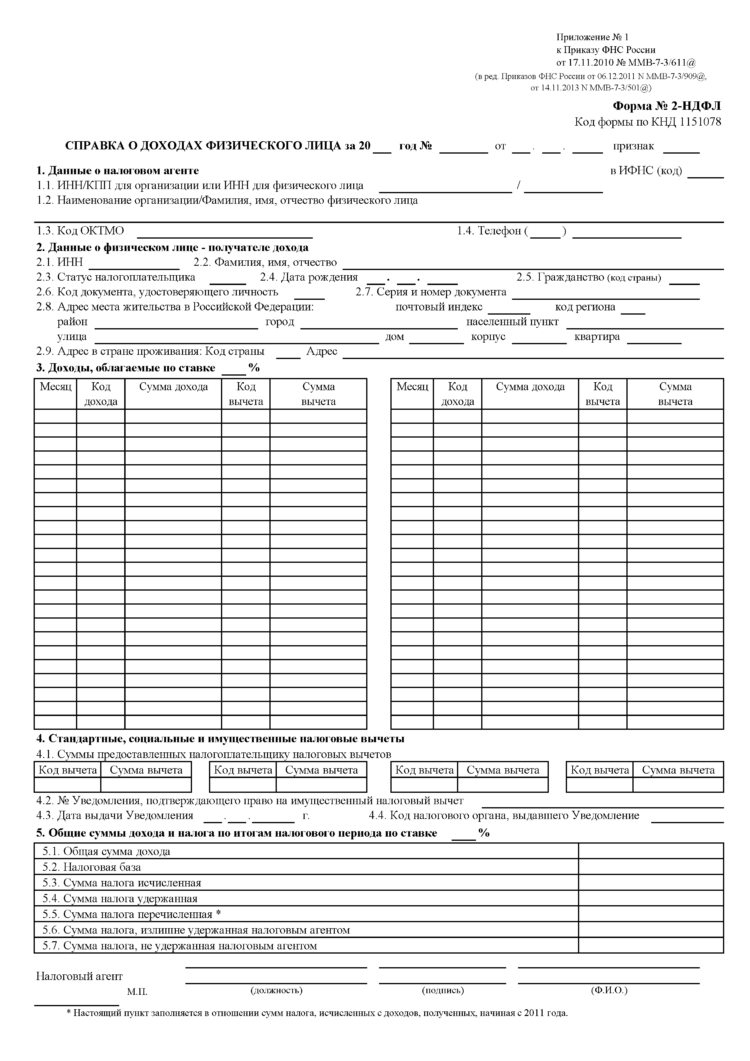

According to form 2NDFL

This is a unified document containing official data on income received and taxes paid by an individual.

It reflects the following data:

- the amount of accrued wages for each month;

- tax deduction amount;

- the total amount of income received for the billing period;

- employer information;

- information about the salary recipient.

The document is certified by the seal of the organization and the signature of the chief accountant. To confirm income with this certificate, the borrower needs to obtain it before submitting an application to the bank.

Below you can see what the 2NDFL form certificate looks like:

The document must not contain outdated information. For example, if a person takes out a loan in July, then a certificate issued in January will not be suitable.

How long it takes to do this and for what period you need a 2-NDFL certificate to take out a mortgage, we tell you in a separate article.

According to the bank form

An alternative to the 2NDFL document is a certificate in a bank form. It is filled out by the boss, accountant or the borrower himself. Information the document contains:

- Full name of the person;

- job title;

- details, name and legal address of the employing company;

- validity period and number of the employment contract;

- calculation of income by month or total earnings for a certain time.

The paper is certified by the employer's seal and the signature of the manager or accountant. Each bank sets its own validity period for the document. For example, in Sberbank it is 1 month, and in Renaissance Credit it is 2 weeks.

According to the employer's form

The document is drawn up in free form by the head or accountant of the company where the borrower works. In addition to information about the organization, income and borrower, the certificate must contain the employer’s contact information.

About declared income

This is an unofficial document. It does not contain the seal of the organization and the signature of the authorities. Compiled by hand in writing by the borrower himself.

What it says:

- information about the place of work (address, contact details of the manager, details);

- job title;

- monthly income;

- the total amount of salary received for the required period.

By filling out this document, the borrower puts his signature, thereby confirming the accuracy of the specified data. If any discrepancies are found, the bank will reject the mortgage application.

Despite the fact that a certificate of declared income is not an official confirmation of the amount of wages, it has one important advantage: the borrower has the right to indicate in it his actual, rather than official, income.

Responsibility of the borrower for providing a false certificate

Falsification of documents is punishable by law. A citizen may be brought to criminal liability in accordance with Article 327 of the Criminal Code of the Russian Federation :

- Fine up to 80 thousand rubles;

- Mandatory work up to 480 hours;

- Forced labor for up to 2 years;

- Arrest for up to six months.

To determine the reliability of the client’s information, the bank examines the correctness of filling out the 2-NDFL certificate and its compliance with the standards specified by the Federal Tax Service.

If in doubt, call the organization that provided the form.

The ability to access Pension Fund databases, which appeared recently, also greatly simplifies verification.

In addition to generally accepted measures, each bank uses its own additional methods of establishing the authenticity of documents.

Checking the authenticity of the 2NDFL certificate. We invite you to watch the video.

Didn't find the answer to your question? Find out how to solve exactly your problem - call right now:

It's fast and free!

| Share with friends: |

We also recommend reading:

If you want to get advice, then write not in the comments, but in the online consultant on the right.

Categories

| Apartments for rent |

| Mortgage |

| Taxes |

| Inheritance and donation |

| Decor |

| Purchasing apartments |

| Apartments for sale |

| Disputes with neighbors and cohabitants |

| Housing and communal services |

Average cost m2

| City | Oct 2019 | Sep 2019 |

| Moscow | 216.8 tr. | 213.5 tr. |

| St. Petersburg | 133.9 tr. | 132.7 tr. |

| Ekaterinburg | 74.4 tr. | 74.3 tr. |

| Novosibirsk | 72.5 tr. | 71.9 tr. |

| Sochi | 122.1 tr. | 121.5 tr. |

Subscription by E-mail

VKontakte subscription

Last update 2019-07-14 at 12:12

Many people face the important question of purchasing their own home. A lot of houses are being built, but the price is high. Not everyone can afford to simply buy without support. One of the financial instruments is a mortgage. For this purpose, the potential borrower prepares a package of documents for the bank, which includes a 2-NDFL certificate. Let's talk further about what requirements banks place on it.

Purpose of provision

An income certificate is provided to confirm creditworthiness. The bank’s decision, payment amount, interest rate, and loan amount depend on the size of the salary.

When reviewing documents, the lender looks at the client's monthly income and assesses his financial capabilities. Based on salary data, he sets the payment amount that the borrower can deposit into the account monthly without major damage to the family budget. After paying the payment, the borrower must have at least funds equal to the subsistence level.

Most banks require 2NDFL or a certificate in the bank's form. These two documents are official evidence that a person has a job and income. Other methods of verifying income are considered only as a last resort.

Validity period of the certificate in form 2-NDFL

There is no set validity period for a personal income tax certificate. However, the bank is interested in receiving up-to-date information about the mortgage applicant’s earnings.

Look at the same topic: Methods for urgent redemption of mortgaged apartments

Typically, banks consider the optimal validity period for a certificate to be 2-4 weeks. Upon completion, the document loses legal force, and, if necessary, the borrower will have to order a new one.

The specific validity period of the document can be found out at a bank branch or by calling customer support.

Who can provide?

The paper is drawn up by the borrower’s boss or accountant. According to Article 62 of the Labor Code of the Russian Federation, it must be provided to the applicant within 3 days after the application. You should tell the official in advance about why this document is needed and for what period, so that problems do not arise later.

If the borrower is unable to confirm his salary with an official document, then he fills out a certificate in the form of the bank. The form is issued by the financial institution where the mortgage is issued.

IMPORTANT! There are a lot of offers on the Internet for the sale of 2NDFL certificates. Any salary can be included in the certificate to increase the chances of getting a loan. However, by providing fake documents, the borrower dooms himself to the bank’s refusal to provide a loan.

A certificate on the employer's form is provided by the boss from the borrower's place of work. The document on the declared income is written by hand by the borrower himself.

Comparison of conditions

each of the 4 best mortgage lending offers separately above. Now let’s compare the conditions of all bankers in one table.

| Rosbank | Sovcombank | Eastern Bank | Home Credit | |

| How much can you get | 50 000 — 3 000 000 ₽ | 150 000 — 30 000 000 ₽ | 25 000 — 3 000 000 ₽ | 10 000 — 1 000 000 ₽ |

| For how long | 17 years | 1 – 10 years | From 13 months | 15 years |

| At what % | 10,99% — 18,99% | 11,9% — 22,9% | From 9.9% | 7,9% — 24,9% |

Thus, we come to the following conclusions:

- the minimum loan term is one year in any organization;

- the lowest mortgage interest rate at Home Credit is 7.9%;

- the longest loan term at Sovcombank is 10 years;

- the maximum possible loan amount is RUB 30,000,000 at Sovcombank.

See also: Innovative application from Tinkoff Bank for business

Do you need money in cash? In this article, we have published proven methods for obtaining a cash loan from Tinkoff Bank.

Apply for a cash loan at Tinkoff Bank

What information will be checked?

Does the bank check the data specified in the borrower’s documents and how? Personal information is verified in several stages. They are first processed by a scoring system, then checked by a credit inspector and a security service. Employees of a financial institution pay special attention to the amount of income and place of work, since the solvency and stability of the client is one of the main requirements.

How the check works:

The credit inspector checks the data specified in the application form with the information in the certificate. They must be identical. If a borrower receives one amount according to official papers, but indicates a larger amount in the application form, this may raise many questions and doubts for an employee of the institution.- The appearance of the document is assessed. If the borrower has provided a 2NDFL certificate, then it must be of the established form containing all the required data.

- The validity of the paper is checked. Employees of the institution find out whether the organization in which the client works really exists.

- If any information arouses suspicion, a bank employee contacts the employer and clarifies the details of interest.

When filling out the application, it is important to indicate the work phone number of your superiors, since if the credit manager cannot contact the employer, the application will be rejected.

Is a loan possible without proof of profit?

Not all potential borrowers are ready to confirm income for a mortgage by bringing a certificate from work.

There are reasons for this:

- the client does not have time to collect papers;

- he receives a “gray” salary.

In fact, the borrower may have a stable and high income that allows him to repay the mortgage loan. However, without 2NDFL certificates or a bank form, getting a loan several years ago was almost impossible.

In order to expand their client base, many lenders have launched mortgage programs under which salary confirmation is not required. To consider an application, only 2 documents are required - a passport and any other identification document. However, the borrower will need to provide information about the profit received, the field of activity and the organization for which he works.

A mortgage without certificates does not at all mean that banks accept applications from unemployed citizens or persons with irregular income. These programs one way or another imply further verification of the salary of a potential client and his place of work.

A mortgage without income certificates has its own characteristics:

- inflated interest rate;

- high down payment;

- short loan period.

From our separate publications you can also learn about what bank form certificates are required to apply for a mortgage in Sberbank and VTB 24.

Where can they provide it?

The following institutions issue mortgages without proof of salary:

Gazprombank : rate from 10%, down payment from 10% (only for bank clients).

- Rosselkhozbank : rate from 10.25 to 12.5%, down payment – from 40%.

- VTB24 : rate from 10.7%, down payment from 30%.

- Uralsib Bank : rate from 10.5%, down payment from 10%.

- Sberbank : rate from 7.4% (for housing under construction), down payment - 50%.

We will tell you more about which banks can provide a mortgage without proof of income in a separate publication.

Is it possible to buy certificates for a mortgage?

On the Internet, the query “buy documents for a mortgage” or the regional one “buy documents for a mortgage loan in Moscow” immediately brings up a huge number of sites that offer a wide range of different services from official employment to the provision of a whole package of papers or individual certificates (copies of employment contracts, 2-NDFL certificates, certificates of account status and other forms).

Fact! The price for providing such documents (2-NDFL, entries in the work book, etc.) for a mortgage ranges from 1,500 rubles to 5,000 rubles for a complete package of papers for a mortgage loan. Purchasing a set of documents for a mortgage in Moscow may cost a little more.

A fake work certificate is required for citizens who cannot document their own solvency, but need a mortgage loan. This leads to:

- low official wages are the same gray wages. In fact, the borrower can afford to take out a mortgage, but according to official data, his income level is considered insufficient;

- lack of official employment - part-time work, freelancing, informal employment abroad;

- failure by the employer to provide a 2-NDFL certificate for any reason;

- lack of the required level of earnings and work experience.

Since a person is interested in obtaining a mortgage loan and, having received a refusal due to confirmation certificates, he begins to look for alternative ways: he orders certificates, gets a job in “left” offices and companies (with subsequent dismissal after receiving approval).

About interest paid

According to Article 220, paragraph 1 of the Tax Code of the Russian Federation, when purchasing a home on credit, the borrower has the right to receive a tax deduction - principal and interest deduction. In order to make a refund, you will need to collect a number of documents, including a certificate of mortgage interest paid.

This document must be provided by the bank upon the client’s request. What should it contain:

- information about the borrower;

- loan agreement number;

- period;

- dates of payments;

- amount of repaid debt;

- amount of interest paid.

The document production period is 28 days. In this case, the borrower receives it for free. If you need paper urgently, the bank can provide it within 3 days for a fee. The cost depends on the bank. On average, it is 200-400 rubles.

Despite the fact that, under the terms of some programs, banks offer to apply for a mortgage without proof of income, the borrower should be aware that in this case the lending conditions will not be favorable for him. Having an official document gives banks more confidence and allows you to take out a mortgage on flexible terms.

Registration of a mortgage using two documents

Banks that agree to the following conditions:

- Tinkoff. From 15% down payment, interest rate from 6% to 14%, which depends on the type of property purchased.

- VTB. From 40% down payment when purchasing a secondary home and 30% when purchasing a primary home, rate from 9.6%.

- Sberbank. From 40% contribution and additional 0.5% to the base rate.

- "Gazprombank". From 40% contribution, rate from 10.2%.

- Rosselkhozbank. From 40% down payment, rate from 9.35%.

- "Alfa Bank". Down payment of at least 50%. Rate from 9.79%.

- DeltaCredit. 40% contribution and 8.25% rate.

- Transcapitalbank. Contribution 30%, rate 8.2%. This financial institution has a limit on the mortgage amount. For Moscow and St. Petersburg this is 12 million rubles, and for residents of other settlements - 5 million rubles.

- "Uralsib". 40% contribution and 9.4% rate.

You might be interested: What is the commission when transferring from Sberbank to Sberbank?