Would you like to consult a lawyer for free? Write to the chat on the bottom right or call the hotline, calls within the Russian Federation are free.

When buying an apartment on credit, the borrower must insure the property. This is a mandatory condition of the bank imposed on a client applying for a loan to purchase a home. The benefit of insurance for the client is that he will be able to receive a certain amount of compensation for damage or destruction of real estate. What documents are required to obtain insurance, read below.

Why do you need mortgage insurance?

The Federal Law “On Mortgage (Pledge of Real Estate)” states that each borrower is required to insure the purchased housing (house, apartment). The same real estate plays the role of not only a lending object, but also a collateral.

In addition to mortgage insurance, many lending institutions require the borrower to take out life, health and title insurance policies.

Reasons for such requirements:

- A mortgage is the most long-term type of loan, associated with a large amount of money intended to finance the purchase of a home. Since the loan repayment period is long, there is a high risk of circumstances that will prevent the bank from returning the loan amount with interest. Such cases include loss of health, disability or death of the borrower. For this reason, leading banks that practice mortgage lending require the client to take out a life and health insurance policy.

- The need for title insurance is explained by the existence of a risk of loss of ownership of the housing being financed. Insured events include double sale of an apartment (house), which was made intentionally or erroneously, errors in the real estate register, fraud, etc.

- Real estate is subject to damage or complete destruction, which is associated with a flood, fire, or destruction of the house. Because of this, there is a need for insurance when purchasing an apartment.

List of insured events:

- damage or destruction of real estate by fire, hurricane, explosion of domestic gas, steam boiler;

- falling loads on the house;

- collision with a vehicle;

- natural disasters;

- structural defects of load-bearing structures;

- intentional destruction or destruction of real estate by third parties

There is a list of cases that do not apply to insurance:

- environmental disasters caused by a nuclear explosion or the spread of radiation;

- military exercises and activities;

- Civil War;

- political crisis;

- strikes;

- destruction of the house by decision of government authorities.

If the borrower is temporarily unable to work, then this case is also not considered an insurance case.

Why do banks require apartment insurance?

According to the federal law of July 16, 1998 No. 102-FZ (as amended on August 2, 2019) “On mortgage (real estate pledge)”, Art. 31 “Insurance of pledged property. Borrower liability insurance and lender financial risk insurance": "1. Insurance of property pledged under a mortgage agreement is carried out in accordance with the terms of this agreement. An insurance contract for property pledged under a mortgage agreement must be concluded in favor of the mortgagee (beneficiary), unless otherwise specified in the mortgage agreement or in the agreement giving rise to a mortgage by force of law, or in the mortgage.”

This is due to:

- a long term mortgage loan, during which unforeseen situations may occur with the collateral (a fire or natural disaster, as a result of which the apartment may be destroyed);

- the fact that the borrower may not fully repay the mortgage loan. The bank will be forced to take away the collateral property (apartment, house), and if it is in disrepair, all costs to the bank will be covered by insurance.

It is important to understand that the borrower has the right to choose the insurance company himself. He does not have the obligation to insure the collateral property with the bank that issued him the mortgage loan. The only thing you should pay attention to are reviews of the insurance company and pricing policy.

To obtain insurance you must:

- decide with the insurance company,

- read the insurance contract,

- make a preliminary calculation of the cost of insurance of collateral property (online calculator,

- write an application to the insurance company to draw up an insurance contract.

Important!

It is necessary to draw up a mortgage insurance agreement for an apartment (house) after receiving the property.

Cost of insurance

The cost of apartment mortgage insurance depends on various factors, including:

- location of the object;

- mortgage payment amount;

- total loan amount;

- a list of insurance risks determined individually for each borrower.

It is more profitable for the borrower to purchase comprehensive insurance than to issue separate policies for different types of insurance. The price of a comprehensive policy ranges from 0.5 to 1.5% of the total market value of the housing purchased on credit.

If the borrower purchases 3 policies separately, then this figure will be higher than 1.5% of the cost of the purchased living space.

Types of insurance

Apartment mortgage insurance can be divided into 2 types:

- insurance of purchased housing;

- life and health insurance.

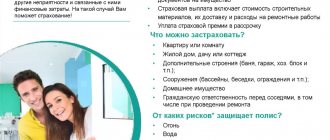

Typically, banks require first of all to insure the collateral property, namely the apartment that is purchased with a mortgage. The structure of the building (walls and ceilings) and the decoration of the premises are separately insured. To save money, some borrowers use a trick and insure only the structure of the building, which allows them to reduce insurance payments. By concluding a mortgage loan insurance agreement, the client can expect to receive payment in the following insured events:

- fire;

- earthquake;

- storms and showers;

- floods;

- tornado;

- falling of manned aircraft;

- collision with a vehicle;

- any illegal actions of third parties.

If the borrower is over 40-45 years old, when applying for a long-term mortgage, some banks require additional life and health insurance for the person being borrowed. This allows the bank to protect itself in the event of not only the death of the borrower, but also his disability, which may lead to the impossibility of repaying the mortgage loan.

Most insurance companies today offer several mortgage insurance programs for the client to choose from. The most popular insurance product remains comprehensive insurance, which guarantees protection against all the force majeure events listed above. At the same time, the selected program must be agreed upon with the bank in order to obtain approval for signing the insurance contract.

Is it possible to refuse apartment insurance?

Citizens who want to use the mortgage lending service doubt whether it is necessary or not, and want to refuse to purchase a policy, wanting to save money. But, according to the Law of the Russian Federation “On Mortgages”, the borrower is obliged to insure the collateral, which is the apartment he is purchasing. Title, health and life insurance policies are optional by law, and the borrower has the right to refuse them. Moreover, such a refusal must be issued before signing the loan agreement.

The bank may include clauses in such a document that stipulate that the borrower is obliged to take out policies other than insurance of the mortgaged property. Signing such an agreement means that the client agrees with all its points, and therefore is obliged to fulfill them.

Insurance when buying an apartment with a mortgage is a paid service, but it allows you to buy a home on credit on more favorable terms for the borrower. If the client does not fully insure the risks associated with lending, the bank will increase the interest rate on the loan. An increase in mandatory mortgage payments is compensation for the risk of non-repayment of debt, which may be associated with the loss of a permanent job, health, ability to work, or solvency by the borrower.

Title insurance for an apartment with a mortgage?

First, it is necessary to clarify that a title is a document that provides the borrower with ownership of the property.

Registering a title means protecting yourself from the risk of losing an apartment, which may be coveted by the former owners of the property or their relatives.

You need to understand that if you do not take out title insurance, you risk losing your apartment if the seller violates the procedure for buying and selling an apartment.

With this type of insurance, if the procedure for registering real estate is violated, the insurance company is obliged to reimburse the borrower for the cost of the apartment at the market price.

This type of insurance is most relevant when purchasing an apartment on the secondary real estate market. But not very popular because of its price.

Documents for mortgage insurance

A visit to the office of the insurance company will require the borrower to have an impressive package of documents. Among them:

- A completed application form for concluding a mortgage insurance agreement;

- Borrower's passport;

- Medical certificate confirming the absence of psychoneurological pathologies;

- Title documents for the apartment;

- A copy of the report completed by the appraiser;

- Cadastral passport and plan of all premises of the pledged property;

- Certificate about the cost of the apartment.

You can simplify the procedure for purchasing a policy using the Prosto.Insure online service. The buyer of an apartment will not have to visit the office of the insurer - all actions are performed on the website, and information from the listed documents is entered into a convenient electronic form.

What risks does the bank require to insure?

After the house is put into operation, ownership of the apartment (which is pledged to the bank)

passes from the developer to the shareholder. Now this is his property and he loses the right to receive compensation for risks associated with the activities of the developer. Therefore, you need to take out an insurance policy for the risks of damage and destruction of your property.

What risks does the bank require to insure? A traditional insurance contract developed by insurance companies for mortgage holders typically includes:

- Life and health insurance of the borrower;

- Property insurance;

- Title insurance.

The main requirement put forward by credit institutions regarding insurance is insurance of the “structure” - these are the walls of the building, ceilings, windows and the front door. Additionally, you can insure the finishing, the cost of which, by the way, ranges from 20% to 50% of the cost of the entire apartment (depending on the spiritual scope and financial capabilities of the owner)

.

Although the bank is not interested in the interior design of the borrower's home, and it does not require insurance for the finishing, it is best to do this, since it is the finishing that suffers in case of fires and floods.

Title insurance, as already noted, in the presence of DDU seems completely useless - there were no transactions on the apartment at all, therefore, there is simply no one to claim the rights of the owner.

Why do you need apartment mortgage insurance?

Insurance of a mortgaged apartment by the mortgagee is a legally mandated option. Its use is aimed at reducing the risks faced by bank clients and financial institutions. At the end of 2020, the average term of loan agreements concluded in Russia was 17 years. During this period, the property may be lost or irreversibly damaged. The bank will suffer losses because the collateral will lose its value, and the borrower will avoid financial responsibility under the previously concluded agreement. Settlement of losses under force majeure circumstances is carried out by a third party, which becomes the insurance company.

Many real estate agents are convinced that apartment insurance with a mortgage is a mandatory condition for cooperation between banks and borrowers. Proponents of this approach refer to Article 31 of the Federal Law “On Mortgage”. But the wording of this section of the document suggests that the insurance contract is mandatory in the absence of other conditions in the loan agreement. Those. the bank and the borrower can agree that insurance of the mortgaged apartment is excluded from the terms of their cooperation. Credit institutions rarely and reluctantly agree to such transactions - the risk of financial losses remains very high.