Which banks are better to take out a mortgage from?

Alfa Bank

from 6.5% rate per year

Go

- Amount: from 670 thousand to 20.6 million rubles.

- Rate: 6.5 - 9.29%.

- Duration: from one year to 30 years.

- Age: 21 - 70 years.

- Down payment: from 20%.

More details

Gazprombank

from 7.5% rate per year

Go

- Amount: from 500 thousand to 60 million rubles.

- Rate: 7.5%.

- Duration: from one year to 30 years.

- Age: 20 - 65 years.

- Down payment: from 10%.

- Review of the application from 1 working day.

More details

Transcapitalbank

from 7.99% rate per year

Go

- Amount: from 300 thousand to 50 million rubles.

- Rate: from 7.99%.

- Duration: from one year to 25 years.

- Age: from 21 to 75 years.

- You can get a mortgage using one passport.

- You can confirm your income with a bank certificate.

More details

Rosbank

from 7.39% rate per year

Go

- Amount: from 300 thousand rubles.

- Rate: 7.39 - 11.14%.

- Duration: from 3 to 25 years.

- Age: from 20 to 64 years.

- Down payment: from 20%.

- You can attract 3 co-borrowers.

More details

Applying for a mortgage for my husband

conclude a marriage contract or make the other half your co-borrower. This is necessary in order to protect the interests of the mortgagee in the event of a divorce and subsequent judicial division of property. To prevent such disputes from arising, banks prefer to persuade spouses to enter into a marriage contract.

If the spouse is pregnant, it is unlikely to be able to attract her as a co-borrower, since the bank understands that she will soon lose her permanent income, and the benefits received are unlikely to be enough for full compensation. Moreover, the composition of the family will change. Therefore, if you do not want problems with obtaining a mortgage, then enter into a marriage contract.

If in this case you are a co-borrower (mortgage for two), then 2 dependents will be taken into account in your spouse’s income: you and the unborn child. This option is applicable if your husband earns at least 30,000 monthly mortgage payment (with 1 pregnancy). If you already have a child, accordingly increase your spouse’s income by another 10,000.

A good option would be to find a reliable guarantor and completely avoid your participation in the transaction. But, you never know what will happen in the future... As they say, “and live happily ever after until the mortgage runs out.”

How to apply online for a mortgage?

The first step in obtaining a mortgage loan is submitting an application to the bank. The most convenient way to do this is through the official website, so as not to waste time traveling to branches and queues. On their pages, banks offer to fill out questionnaires. They indicate the desired parameters of the mortgage: term, amount, size of the down payment. You also need to enter data from your passport, information about employment, income, and marital status.

After submitting the online application, you will need to wait approximately 1 - 3 days. The exact period depends on the bank you contact. The credit manager informs about the decision made by calling the phone number specified in the application form.

Are mortgages and pregnancy compatible?

When applying for a policy, the insurance company will definitely ask if you are pregnant and if you intend to have children in the near future. Some companies do not insure pregnant women at all, some are satisfied only for up to 6 months, but the fact itself is necessarily reflected in the documents. Therefore, if you managed to hide the fact of pregnancy from Bank employees, the truth may come out at the insurance company.

Officially, no one can infringe on the rights of expectant mothers, and mortgages for pregnant women are not contraindicated, but the internal guidelines of most banks oblige managers to refuse this category of citizens (meaning, put a mark about pregnancy in the application with a pre-prepared refusal). Some credit specialists, unfamiliar with the law or just a little insolent, directly send the pot-bellied category home.

Under what conditions do banks give mortgages to pregnant women?

In 2020, loans for pregnant women are no different from loans to other categories of citizens. Pregnancy is not a reason to refuse funds for the purchase of housing. The main thing is that you must prove that you are solvent.

The collateral for the mortgage is the residential property you are purchasing or other premises that you own. Some banks also allow guarantees from other persons.

When applying for a mortgage loan, it is required to insure the property being purchased. Banks also offer to conclude a personal life and health insurance agreement. This agreement is voluntary, but for pregnant women banks sometimes make it a mandatory condition.

Other lending conditions vary from bank to bank. The size of the down payment varies from 10-30% of the value of the property (at Sberbank - from 15%). If you have maternity capital, you can make it as an initial payment.

Also read: Mortgage for maternity capital at VTB: conditions, rates and down payment

The maximum loan term is approximately 20-30 years, the minimum interest rate is 8-10% per annum, and the amount is from 300 thousand to 60 million rubles. For example, Deltacredit offers to take out a mortgage at 8.25% per annum for up to 25 years with a minimum amount of 600 thousand rubles.

Alfa Bank

from 6.5% rate per year

Go

- Amount: from 670 thousand to 20.6 million rubles.

- Rate: 6.5 - 9.29%.

- Duration: from one year to 30 years.

- Age: 21 - 70 years.

- Down payment: from 20%.

More details

Gazprombank

from 7.5% rate per year

Go

- Amount: from 500 thousand to 60 million rubles.

- Rate: 7.5%.

- Duration: from one year to 30 years.

- Age: 20 - 65 years.

- Down payment: from 10%.

- Review of the application from 1 working day.

More details

Transcapitalbank

from 7.99% rate per year

Go

- Amount: from 300 thousand to 50 million rubles.

- Rate: from 7.99%.

- Duration: from one year to 25 years.

- Age: from 21 to 75 years.

- You can get a mortgage using one passport.

- You can confirm your income with a bank certificate.

More details

Rosbank

from 7.39% rate per year

Go

- Amount: from 300 thousand rubles.

- Rate: 7.39 - 11.14%.

- Duration: from 3 to 25 years.

- Age: from 20 to 64 years.

- Down payment: from 20%.

- You can attract 3 co-borrowers.

More details

Why do banks refuse pregnant women?

Financial institutions accurately describe the reasons that force them to refuse borrowers during pregnancy. The fact is that they do not give families money due to the sharp risk of non-return. At the same time, there are two main problems that force one not to give consent to purchase an apartment on a mortgage.

- Increased family expenses;

- Decrease in total income.

Both points are obvious, but still require meaningful consideration. Some people believe that banks are biased towards potential clients. However, every family must understand that after the birth of a child, absolutely everything changes in the family. For this reason, parents themselves should first seriously think about purchasing residential real estate, as it will entail additional costs. Although it is still worth describing in detail the reasons for the bank’s refusal so that people find a way out of the situation.

Increased family expenses

The first problem is considered to be a sharp increase in family expenses. Even during pregnancy, a lot of money is required, and after childbirth, the consumer basket changes. Credit commissioners must take this point into account when calculating risks, so they prefer to refuse immediately so as not to lose even part of the loan funds.

Avoiding rejection due to this risk is not difficult. To do this, you need to provide a large and stable family income, which can easily cover the increase in expenses. In this case, bank employees will definitely take into account the current circumstances, so they will probably agree to issue a mortgage. Although there will still be many issues that require attention from the borrower.

Decrease in total income

Applying for a home loan with the participation of a co-borrower will create a different situation, which will certainly alert the credit commission. When the salary of a pregnant wife is also taken into account in the total income, then a refusal will definitely come. The fact is that maternity leave is coming, which means her profit will immediately disappear. Consequently, the bank will have to revise its own terms of the agreement.

Total income is a serious mistake that should not be made. It is better to try to find another suitable way out of the situation than to face pressure from the security service. The father must still have a large salary that fully complies with all the requirements of the financial organization, so that another problem does not happen.

What will influence the bank's decision?

In order for the bank to make a positive decision on your application, you must prove that you have a stable income that will be sufficient to repay the debt. After going on maternity leave, your income level will decrease, so it is recommended to submit an application before it begins or present a certificate of refusal of parental leave.

If you are married, your spouse will be a co-borrower. The bank will also take his income into account when considering the application. Therefore, the husband should take care of an official job and high earnings. But it is best to apply for a loan in the name of your spouse, then there will be more chances to get a mortgage.

To increase the likelihood of approval of the application, you should agree to conclude a personal insurance contract. This is a voluntary procedure, which many refuse. But if you agree, your mortgage rate will be lower. To increase your chance of getting a mortgage, we recommend finding solvent guarantors.

Do pregnant women get a mortgage at Sberbank?

General requirements are provided for all types of lending. An application for a mortgage loan is considered on an individual basis. The decision is made based on the client’s ability to fulfill debt obligations for a long time. Obtaining a mortgage for pregnant women at Sberbank is available; expecting a child is not a reason for refusal.

The issue of improving living conditions for young families becomes especially acute during the period of anticipation of a new addition to the family. In most cases, the only way to achieve your goal is a mortgage loan. The terms of the loan provide for an assessment of the solvency of potential borrowers. The legislation does not provide for restrictions on pregnant women obtaining a mortgage from Sberbank. However, in some cases, employees reject the application due to high risks. Therefore, it is worth preparing a profitable strategy in advance to minimize risks.

Requirements for the borrower

The bank has standard requirements for pregnant women:

- Age - from 21 years.

- Official employment.

- High solvency (the bank will tell you the required level of income).

- Russian citizenship and permanent registration.

Credit history is also taken into account. If it is damaged, the chance of approval of the application is significantly reduced.

How to increase your chances of approval

The bank may not issue a mortgage during pregnancy in 2020 for the same reasons as when considering an application from another client. The main reasons for a negative decision are bad credit history, low income and high debt load. If a woman is expecting a child, her profile will be checked even more carefully, because the risks are very high. You should be prepared for a possible reduction in the amount, an increase in the interest rate and a long repayment period.

Recommended article: How to get a tax deduction for a co-borrower on a mortgage

How to increase your chances of getting a mortgage approved:

- Contact the bank where you have your salary card. The likelihood of a positive decision here is much higher.

- If you do not plan to report your pregnancy, notify your accounting department and management in advance about a possible call from a banking specialist. If they talk about the upcoming maternity leave, your chances of getting a loan will seriously decrease.

- Involve a co-borrower taking into account his income, this will increase the likely loan amount. This will necessarily be the spouse (), but if desired, you can add parents or other relatives.

- A mortgage during pregnancy at Sberbank should be issued according to the internal program for young families. The main condition is that one of the spouses must be under 35 years old. Subsequently, such a mortgage for a pregnant woman from Sberbank will allow her to receive a deferment of debt repayment upon the birth of a child. In addition, the interest rate will be lower than the standard tariff.

- Choose large, reputable banks that do not work with dubious collection agencies. For example, a mortgage during pregnancy at VTB, Sberbank or Rosselkhozbank will be safer, because restructuring is provided here. Lenders are accommodating, especially when a child is born, and are ready to defer repayment.

Important to know: Mortgage without a credit history – chances of getting approval

Questions when applying for a mortgage

Reasons for refusal of a mortgage: what should borrowers take into account?

Can a mortgage be denied after approval?

Is it possible to take out a mortgage with arrears and court orders?

A mortgage during pregnancy with a second child will allow a woman to subsequently use maternity capital to repay it (). She will also be able to refinance the loan at 5-6% per annum under the state support program for Russian families. At the birth of a third or subsequent baby, you can receive a subsidy in the amount of 450 thousand rubles to pay for a housing loan (). So, getting a mortgage for a pregnant woman with her second child can come in very handy; the main thing is to correctly assess your financial capabilities before government subsidies are credited.

Recommended article: What to do with a mortgage if the developer goes bankrupt

Real estate requirements

Each bank has its own requirements for real estate. The main condition is high liquidity.

To make it easy to sell a home in the event of non-payment of a loan debt, it must meet the following criteria:

- No emergency condition.

- Availability of all necessary communications.

- Concrete, stone or brick foundation.

- Lack of wooden floors.

- No encumbrance, for example, the apartment is not pledged.

- Serviceable doors and window openings.

Also read: Which apartment is suitable for a mortgage and how to find out why the bank did not approve the housing

Alfa Bank

from 6.5% rate per year

Go

- Amount: from 670 thousand to 20.6 million rubles.

- Rate: 6.5 - 9.29%.

- Duration: from one year to 30 years.

- Age: 21 - 70 years.

- Down payment: from 20%.

More details

Gazprombank

from 7.5% rate per year

Go

- Amount: from 500 thousand to 60 million rubles.

- Rate: 7.5%.

- Duration: from one year to 30 years.

- Age: 20 - 65 years.

- Down payment: from 10%.

- Review of the application from 1 working day.

More details

Transcapitalbank

from 7.99% rate per year

Go

- Amount: from 300 thousand to 50 million rubles.

- Rate: from 7.99%.

- Duration: from one year to 25 years.

- Age: from 21 to 75 years.

- You can get a mortgage using one passport.

- You can confirm your income with a bank certificate.

More details

Rosbank

from 7.39% rate per year

Go

- Amount: from 300 thousand rubles.

- Rate: 7.39 - 11.14%.

- Duration: from 3 to 25 years.

- Age: from 20 to 64 years.

- Down payment: from 20%.

- You can attract 3 co-borrowers.

More details

Is it possible to take out a mortgage while pregnant?

A woman can take out a mortgage if she meets the main condition - solvency. It’s better to get a loan for an apartment/house before going on maternity leave. There is no reduction in income. For the request to meet the conditions, documentary evidence of additional income or the woman’s own business must be provided. The husband or father acts as a co-borrower. If the client resolves this issue correctly, it will be inappropriate to refuse the borrower. Taking out a loan will be much easier.

Employees of the creditor bank, during the consideration of the application, have the right to refuse to provide a loan to a pregnant woman without specifying the reasons. Not all organizations are willing to provide loans to this category of the population due to the risks of non-payment of funds. Provided by the following verified organizations:

What documents are needed?

To apply for a mortgage loan you will need:

- Russian citizen passport.

- Certificate of salary level - 2-NDFL.

- Work book or employment contract.

- Certificate of marriage or divorce.

After the initial approval of the application, it is required to present to the bank the title documents for the purchased property (purchase and sale agreement), a certificate of absence of encumbrance, technical papers for the premises, for example, a cadastral passport.

Mortgage for individual entrepreneurs in Sberbank: features and conditions for obtaining

- Buying housing on the secondary market or in a new building. The bank will consider your application on an individual basis. Depending on the documents provided, the percentage may be slightly higher than usual. If you have a simplified taxation system, but have internal accounting, then the chances of a positive answer are also quite high. Having a guarantor will also work in your favor. But even in the most difficult case, when it is not possible to prove a stable income, there is such an option as “Mortgage on two documents”. Sberbank has developed a program that makes it even easier to get a mortgage, but the rate and down payment are even higher. You must immediately pay 50% of the cost of housing.

- Business Real Estate. This is a program for purchasing commercial real estate. The terms will not be as long as when buying an apartment, up to 10 years, the down payment will be from 25%, the interest rate will be from 14.4%. Necessary conditions are a pledge of the purchased property and a surety.

- Business Invest. This is a loan for the purchase of equipment, repairs, etc. Sometimes a company needs very expensive equipment, which will then pay for itself, so it is necessary to take out large loans at low interest rates. The term is also up to 10 years, the rate is 14.81%.

- Business Rent. Sberbank offers a program specifically for landlords. The offer is very profitable, and it does not matter what kind of premises and for what purpose you are buying. The percentage is quite low, starting from 13.75%.

- Express Mortgage. The rate for this mortgage will be higher than in other programs, from 17%. Term up to 10 years, amount up to 7 million rubles (for Moscow). The amount will depend on the duration and income of the client.

These are the basic required documents, but they can be supplemented by the bank if necessary. For example, a financial institution may ask for your driver's license, military ID, higher education diploma, any papers related to marital status: marriage certificate, prenuptial agreement, birth certificates of children.

What mortgage benefits are available for pregnant women?

Many banks offer benefits to pregnant women on their existing mortgage, such as debt restructuring. This service involves increasing the loan term and reducing the monthly payment or obtaining a deferment of repayment of the principal debt for some time. To receive such assistance, you must contact the bank with a corresponding application.

Also read: Mortgage restructuring at Gazprombank: conditions, requirements and reviews

Reviews about getting a mortgage while pregnant

Semyon Koryakin:

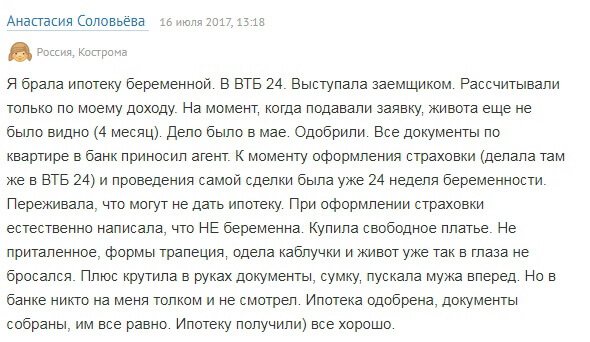

“My wife tried to get a mortgage when she was 5 months pregnant. I contacted VTB and was refused. Then I decided to visit Sberbank, they approved it. I acted as a co-borrower, plus they brought in a guarantor with a good salary. We got it done quickly, although we had to agree to personal insurance.”

Elena Orlova:

“I took out a mortgage from Alfa Bank when I was pregnant. There were no problems, and the conditions were favorable.”

Mortgages for pregnant women are possible with restrictions

Surely in many families during pregnancy there is an urgent need to improve living conditions. Indeed, the upcoming birth of a baby makes you think about whether loans are given in such situations. True, it is necessary to disappoint people by describing the most complex approaches of each bank to such issues. After all, to obtain a loan you will need proof of income, and in view of the future maternity leave, the mortgage becomes a problem.

Mortgage for pregnant women becomes a problem