Non-target mortgage: what is it?

The term “non-target mortgage” refers to a type of banking product in which the borrower has the opportunity to obtain a loan for a long term. A distinctive point is that the client has the right to independently determine the purposes of investing borrowed capital and the client’s property is collateral for the bank. Most standard mortgage products today involve issuing a loan for the purchase of apartments on the primary or secondary housing market, but there is no shortage of proposals for misuse of funds.

Within the framework of non-targeted loans, it is possible to use money for the following purposes:

- purchase of non-standard housing;

- acquisition of real estate for commercial use;

- construction of real estate or carrying out expensive repairs;

- financing of specific expenses.

Some borrowers take out a non-targeted loan to obtain an additional source of funds to pay for treatment, education of children, or long-planned events.

This type of mortgage involves securing the loan with collateral. It is the liquid property of the borrower, that is, property that has a high value and allows for quick implementation when such a need arises. Banks are ready to consider attracting the following types of objects:

- apartments and dachas;

- land;

- private houses and townhouses;

- capital garage boxes.

A separate type of lending is represented by consumer and non-targeted loans for any purpose. The former usually do not require the presence of collateral, but are usually characterized by a high interest rate, a short contract period and a small loan volume. In this regard, they are rarely involved in the process of purchasing housing, as they are associated with a high level of overpayment and insufficient amounts.

It might be interesting!

Is it possible to take out a mortgage for two people and under what conditions?

Non-targeted loan: advantages and disadvantages

The biggest advantage of a non-targeted loan is the ability to independently determine the direction of spending funds and not have to report to the bank. The credit institution also benefits, since the loan is provided at a higher interest rate and is secured by collateral. If the debtor has financial problems, the creditor always has the confidence that he will compensate for the risk of non-repayment of money from the proceeds from the sale of the collateral. The amount of financing usually varies within 70% of the cost of such an object, so the bank always has a safety net.

Attracting a non-targeted loan is associated with the following advantages:

- Obtaining an additional source of financing;

- Variability in the direction of spending funds;

- Acceptable lending conditions;

- The feasibility of the requirements for the borrower;

- Long term of contractual relations.

When contacting a bank, a potential borrower can expect to receive loan funds in the amount of 70-80% of the value of the object being pledged as collateral. The average duration of contractual relationships is 10-15 years, which directly depends on the terms of the banking product. Within the framework of consumer lending, this period is on average 3-5 years, which distinguishes non-target mortgages favorably from such proposals. The very fact of providing collateral acts as a guarantor for the bank, so credit institutions often reduce standard requirements for the client, the source and level of officially received income.

A non-targeted loan has the following disadvantages:

- Higher loan interest rates;

- Inability to fully dispose of the collateral during the term of the agreement;

- The need for additional costs associated with engaging the services of an appraiser and an insurance company;

- The risk of losing the collateral if it is impossible to pay debt obligations.

During the period of validity of the agreement with the bank, an encumbrance is placed on the collateral object. The presence of such status means that the owner loses the right to freely dispose of property. He cannot enter into property transactions in relation to it without the consent of the bank, that is, sell, donate or perform exchange actions.

Such “cunning” terminology

A bank loan secured by real estate can be a mortgage or a non-primary mortgage loan. There is a subtle difference between them based on:

- at the facility and lending procedure;

- in essence, property rights are the sum of three “components”: ownership, use and disposal of property. The absence of any of them is a restriction on the exercise of property rights.

A mortgage involves the transfer of property as collateral to the bank, in which the right to own and use remains with the borrower, and the right to dispose of it is transferred to the creditor bank. If the debtor does not fulfill his obligations, the creditor receives the right to sell the mortgaged property and cover the resulting losses with the funds received. Characteristic features of a mortgage:

- the purchase of housing in both the primary and secondary markets is financed;

- targeted lending is carried out - money is issued for real estate, which is then registered as collateral;

- the buyer will be required to make a down payment from his own funds, the amount of which is 10-20% of the cost of the purchased object;

- A loan agreement is signed with the borrower.

There is another borrowing option - a mortgage secured by existing real estate, or they also say - a non-targeted mortgage loan, a pawnshop mortgage. The borrower, in agreement with the lender, provides any liquid real estate as security. Moreover, the collateral may belong to the recipient of the loan, the guarantor, and the co-borrower. The right to dispose of the property remains with the owner, but is limited by the right of pledge, which is registered as an encumbrance. There is no down payment, but the bank will issue a loan in the amount of 70-80% of the market value of the mortgaged property. The market price is confirmed by appraisal companies.

Recommended article: Rosselkhozbank mortgage without down payment

Banking practice confirms that mortgages are used mainly when purchasing new or under construction housing: an apartment, cottage or townhouse. Non-targeted mortgage lending is used for financing and other purposes: to purchase an apartment or house on the secondary market, buy a car, vacation packages, pay for treatment. In any case, the creditor bank retains the primary right to satisfy claims through the sale of the mortgaged property.

When non-targeted lending is secured by existing real estate, two agreements are usually signed with the bank - a loan agreement and a mortgage agreement.

Sample Mortgage Agreement

The terms of the loan agreement are detailed in the article: Mortgage loan agreement: what to pay attention to when signing

Real estate registration

Registration of a non-target mortgage secured by the borrower’s existing residential real estate today is one of the most common options on the credit market.

The conditions for granting a loan in different banks differ according to the following criteria:

- interest rate level;

- loan terms;

- maximum loan amount.

Substantial requirements are imposed on the collateral object, since it acts as a guarantor for the bank to return funds.

The real estate provided as collateral must meet the following list of criteria:

- have sufficient liquidity;

- belong to the borrower by right of ownership;

- have no encumbrance or seizure;

- physical wear and tear should be no more than 50%;

- availability of engineering structures, including water supply, electrical and other communications;

- list of documents to confirm the legality of the redevelopment.

When providing a non-targeted loan, a banking organization may inquire about the future use of funds, but will not organize a thorough check of the fact of their expenditure.

It might be interesting!

Is it possible to refuse a mortgage and how to terminate the contract correctly

What is a non-target mortgage and collateral in a non-target mortgage

A non-target mortgage is a medium- or long-term loan (usually from 5 to 30 years ) issued against existing real estate . The received loan can be used for any purpose, for example, repairs or large purchases.

Therefore, a non-targeted mortgage can be compared with consumer lending for any purpose, however, the amounts issued under mortgage programs are usually significantly higher than the consumer loan limit, and the rates are lower .

As you already know from the article “Mortgage Lending”, the mortgaged property is the property of the borrower, but remains pledged to the bank until the debt is fully repaid. The bank issues a non-target mortgage, taking into account the price of the offered collateral. As a rule, the loan amount is a certain percentage of the value of the property (different for each bank).

For example, if the cost of an apartment is 3,000,000 rubles. a borrower can receive a loan in the amount of 1,500,000 rubles from one bank, and 2,200,000 rubles from another. etc.

The subject of collateral in a non-target mortgage can be:

- Land

Land plots for which individual housing construction is permitted, with the exception of plots in state or municipal ownership.

- Commercial real estate

Enterprises, buildings, structures and other real estate used in business activities.

- Residential Properties

Residential buildings, apartments and parts of residential buildings and apartments, consisting of one or more isolated rooms. When pledging country real estate, both the building and the land plot on which this building stands are registered as collateral.

What conditions do banks offer?

Today, competition in the financial services market is forcing banks to change their lending policies. Loan conditions are becoming more favorable, and requirements for clients are constantly decreasing. If a couple of years ago it was impossible to imagine receiving a loan without a certificate of income, today applying for “two documents” has become a common and widespread practice. Offers of non-targeted mortgages are presented today in all major credit institutions. Among them, there are options intended for individuals, individual entrepreneurs and heads of organizations.

Sberbank

Sberbank today works with clients both in the traditional way and provides the opportunity for remote interaction. The DomClick.ru service is a convenient and simple tool. It makes it possible to quickly search for real estate, conduct sales and purchase transactions using online mortgage registration in Sberbank. The advantage of this option is the ability to verify, evaluate and register the transaction.

Sberbank is ready to work with clients who are over 21 years old, and the age limit is 75 years. The credit institution also imposes requirements on the borrower’s overall work experience. At the last place of work, he must be for at least a year, and the total duration must be 5 years.

A potential borrower can count on the following conditions:

- loan amount up to 10 million rubles;

- minimum loan size is 500,000 rubles;

- interest rate from 11.6%

- The contract period is from one to 20 years.

When applying to Sberbank under the non-targeted lending program, a borrower can count on receiving 60% of the value of the collateral for the object.

It can be:

- standard apartment;

- townhouse;

- private residential building;

- residential property with a residential plot;

- land allotment;

- garage along with the plot.

The bank offers the most favorable conditions to participants in salary projects who have agreed to enter into an insurance contract. If the loan is taken out by the borrower while he is married, then the other half automatically becomes with the borrower.

Mortgage secured by an apartment: conditions and requirements

“First-class” collateral - this is the description bankers give to a liquid asset that can be quickly sold if the debtor does not fulfill its obligations. This is how residential real estate is characterized. But in order for the pledged object to quickly “turn” into money, the requirements must be met. Bank conditions, collateral and borrower requirements for mortgages and non-targeted mortgage lending are somewhat different.

A mortgage secured by an apartment is one of the most inexpensive. Today, the interest rate is 11-12% per annum. Its size is reduced for participants of certain lending programs:

- for young families with at least two young children, subject to the attraction of state support funds - up to 6% per year;

- military personnel, participants in the savings mortgage system - up to 9%;

- clients refinancing loans from other banks - up to 9.5%;

- buyers of real estate in accredited new buildings.

A mortgage secured by an apartment places more demands on the borrower: creditworthiness, discipline, good credit history and payment of a down payment. Registration is carried out in the following order:

- the loan applicant submits an application to the bank and a package of documents confirming citizenship, place of work, length of service and income of the family budget;

- after receiving preliminary approval from the lender, the borrower selects the mortgage object;

- conclude a preliminary contract for the purchase and sale of real estate, which contains a clause requiring the buyer to make a down payment;

- the bank finalizes the loan and transfers funds to the seller;

- The purchase and sale agreement and the mortgage are registered by Rosreestr.

Recommended article: How to apply online for a mortgage at Sberbank without a down payment

A mortgage secured by existing housing is issued at 12-14% per annum, and also has the following advantages:

- the borrower can buy housing on the secondary market, completely ready to move in, often with furniture and household appliances;

- you can take out a non-targeted mortgage secured by an apartment or other real estate owned by relatives or guarantors;

- variety of objects - city apartment, mansion or country cottage, townhouse.

The lender's requirements for the loan recipient are no less strict than with a target mortgage, and are complemented by close attention to the property, both purchased and transferred as collateral:

- title documents are carefully checked, attention is paid to the composition of those registered, avoiding registration of minors and incompetents;

- absence of encumbrances for any reason;

- have a negative attitude towards property rights formalized by a court decision;

- the lender is “picky” about the technical condition of the collateral and the presence of unauthorized alterations. The “age” of real estate should not exceed 30-40 years from the date of construction.

As borrowers, the bank prefers clients with well-paid positions; lends to private entrepreneurs with caution, avoiding using loans for business purposes. It is mandatory to insure the collateral, the purchased property and the life of the borrower.

The procedure for issuing a non-targeted mortgage loan is similar. But upon registration, a down payment is no longer required. Instead, the buyer may pay a deposit to the seller as confirmation of serious intentions. If the value of the pledged property is much higher than the price of the purchased property, then the bank will give 70-80% of the valuation of the pledge and then even a deposit is not needed. This kind of lending is called a mortgage secured by existing real estate without a down payment.

Alfa Bank

Alfa-Bank is traditionally included in the list of the most reliable Russian banks. Clients have the right to choose the option of submitting an application, since the organization provides the opportunity to use the service online.

Non-target mortgage assumes the following conditions:

- loan amount up to 50 million rubles;

- relationship duration is up to 30 years;

- minimum down payment amount 15%;

- interest rate from 9.39%.

The bank imposes standard requirements on clients in relation to the property serving as collateral. A distinctive point can be considered that the building must have a reinforced concrete, stone or brick foundation.

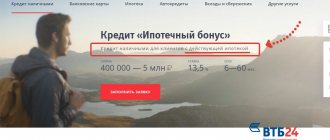

VTB 24

For several years in a row, the bank has been considered one of Sberbank’s main competitors, which forces the organization to constantly improve lending conditions and expand its line of banking products. Non-target mortgage VTB 24 today allows you to obtain a significant amount of lending to finance large expenses with the provision of an apartment as collateral.

Conditions for granting a non-targeted loan:

- pledge of real estate, which is located in an apartment building within the city and a bank branch operates in the zone;

- starting rate from 11.4%;

- the contract term is up to 20 years;

- the volume of lending is 50% of the value of the collateral, but not more than 15 million rubles.

A special feature of the VTB 24 program is that the mortgaged housing can be owned by the main borrower, his spouse or family members. In this case, the owners of such real estate act as guarantors under the agreement. The organization does not provide any fees for processing loan documents and early repayment of the loan.

A non-targeted mortgage gives the borrower greater opportunities to choose where to spend funds. In return, banks offer more stringent lending conditions, which inevitably entails an increase in the total overpayment for the use of borrowed funds. Before contacting a credit institution, experts recommend carefully familiarizing yourself with the requirements that the financial institution imposes on the collateral.

Overview of targeted mortgage loans

We should begin our review of targeted mortgage loans operating today with the traditional Sberbank offer. They offer a record 7.4% per annum for the purchase of housing in new buildings. Less than 10% will cost a mortgage to buy a home on a secondary fund. You can also take out a targeted mortgage loan secured by existing real estate, but at an increased interest rate (approximately 12.5%).

It is worth paying attention to a targeted mortgage loan from Sberbank, which provides the possibility of using funds under a regional and federal certificate for maternity capital. This program offers a reduced interest rate and the ability to make these funds as a down payment or as early repayment of a portion of the borrowed amount.

Rosselkhozbank offers favorable conditions for targeted mortgage lending - there is no need to collect a large number of documents. High level of positive decisions. A mortgage is issued to several co-borrowers, including those who are not related to each other. Here they provide targeted mortgages to pensioners and large families who have received land plots for building a house.

Quite interesting conditions are offered at Alfa Bank, in particular, these are 9:% per annum, a minimum package of documents and a rather loyal attitude to the issues of life insurance and the borrower’s performance.

If you have doubts about the correct choice of a financial institution, we recommend that you seek advice and legal assistance from AHML (Home Mortgage Lending Agency). Here you will not only be selected the most optimal and profitable mortgage lending program for your individual conditions. All documents will be completed here. Here you can sign all agreements with the bank.