Requirements for borrowers and real estate

To receive assistance from the state to pay part of the loan, the characteristics of the real estate taken into the mortgage are taken into account:

- The mortgaged apartment is the only registered housing. It is also permissible to have no more than 50% of the ownership in another object and category of real estate.

- A square meter of an apartment taken on a mortgage cannot have a price higher than 60% than the average cost of the same housing in the borrower’s area of residence.

- Legal “purity” of housing.

- Living space for 1 person (lives alone) cannot exceed the limit of 50 m²; for 2 - 35 m², and for 3 - no more than 100 m² for all.

The bank that issued the mortgage to the borrower can provide detailed advice on all issues of writing off 20% of the mortgage

However, it is important that this financial structure cooperates with the government program. On site, you can also clarify the full list of documents that will be needed for each individual case.

- A copy of the work record;

- Any certificates of income received and benefits;

- Certificate of the amount of pension payments issued by the Pension Fund;

- Certificate certifying the state registration of an individual entrepreneur;

- An extract from the local employment service if any family member is unemployed.

The right to apply for mortgage write-off is also given by such documents as:

- Birth or adoption certificate for each child under fourteen years of age;

- A copy of a certificate confirming the disability group;

- A combat veteran's certificate, which gives the right to a 30% write-off;

- A certificate from the educational institution confirming full-time study.

A very important nuance is compliance with the requirements for receiving a refund on a mortgage from Sberbank. One of them is family income. The right to benefits is available to those citizens whose income level over the past three months has been reduced by thirty percent or more compared to what it was when concluding an agreement with the bank.

The conditions also affect some characteristics of the property purchased with a mortgage. The new rules set restrictions on the square footage of a purchased apartment. Thus, the borrower can receive a payment only if his living space does not exceed 45 square meters for a one-room apartment, 65 square meters for a two-room apartment and 85 square meters for a three-room apartment.

Requirements for mortgage real estate

To receive assistance from the state to pay part of the loan, the characteristics of the real estate taken into the mortgage are taken into account:

- The mortgaged apartment is the only registered housing. It is also permissible to have no more than 50% of the ownership in another object and category of real estate.

- A square meter of an apartment taken on a mortgage cannot have a price higher than 60% than the average cost of the same housing in the borrower’s area of residence.

- Legal “purity” of housing.

- Living space for 1 person (lives alone) cannot exceed the limit of 50 m²; for 2 - 35 m², and for 3 - no more than 100 m² for all.

Interesting video:

Second phase

The encumbrance on the property will be lifted at the Rosreestr branch when the entire debt is written off. After receiving a certificate confirming the absence of debt obligations under the loan agreement, the borrower pays the state fee for removing the encumbrance, attaches the bank bond and submits documents to the registration authorities. Within five days, Rosreestr authorities must make changes to their databases and issue a document confirming the absence of encumbrance on the loaned object. Until recently, it was a Certificate of Real Estate. In 2020, borrowers receive a certificate from the registry indicating that they have no debt.

Contacting the insurance company is one of the last steps. A mandatory condition for a mortgage at Sberbank will be life insurance of the borrower and the loaned property, especially in the first year of the loan. If insurance is not taken out, the interest rate may be increased in the future by at least 1%, which is why many turn to one or another insurance company.

https://www.youtube.com/watch?v=56l-WOPJA6UVideo can't be loaded because JavaScript is disabled: Mortgage SBERBANK. How NOT to pay interest on NDP! Early payment (https://www.youtube.com/watch?v=56l-WOPJA6U)

Mortgage Principal Debt Write-off Program

Who can participate?

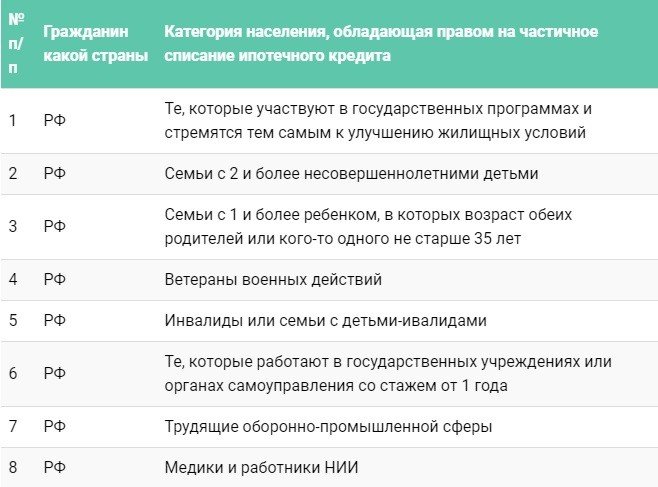

First, let’s determine which categories of citizens can take part in the state program. The borrower must belong to either one or several categories from the list below:

- a young family with one minor child;

- family with 2 children;

- having a disabled child or one of the parents having a disability;

- the presence in the family of a dependent under 24 years of age who has no official income;

- civil servants or mid-level officials;

- workers of a city-forming enterprise or factory;

- participants in a special program subsidized by the state;

- employees of the innovation cluster;

- former combatants;

- employees of organizations established by the Russian Academy of Sciences, members of the Academy of Sciences, scientists.

Requirements for mortgage real estate

What conditions are included in this list:

- The apartment taken on a mortgage must be the only home. Or no more than 50% shared ownership in another real estate property for the whole family is allowed.

- The price per square meter in a mortgaged apartment should be no more than 60% of the cost of an average apartment in the real estate markets in the area where the borrower lives.

- The apartment must be clean from a legal point of view.

The property must meet the strict squaring restrictions set out in Government Decree No. 373. The conditions are as follows. For a person living in an apartment alone, the total living space should not exceed 50 m2.

For two people living, the limit is 35 meters for each resident, i.e. the total area does not exceed 70 meters. When 3 or more people live, the area should not exceed 100 square meters for all family members.

What are the requirements for the borrower's income? Since 2020, innovation has appeared in this area. According to it, in order to receive benefits under the state program, the borrower must have a decrease in income either individually or within his entire family.

The minimum cost of living in Moscow is:

- 17 thousand rubles for an adult working citizen;

- 13 thousand rubles for a child;

- 11 thousand for a pensioner.

Also, the borrower applying for state support should not have bankrupt status assigned in court.

There are also a number of requirements for the features of lending:

- A loan for an apartment must be of a targeted nature.

- The delay must begin from 30 to 120 days, but not more than the specified period.

- As of 2017, there are no longer any other requirements for mortgage lending.

Date of conclusion of the contract

In the first edition of Resolution No. 373, only borrowers who entered into mortgage agreements before January 1, 2015 could receive state support. In the further edition this parameter is not fixed. Only the period from the moment of concluding the contract until applying for debt restructuring is taken into account. It must be at least a year.

Writing off the principal debt on a mortgage - the rules of the law

The legislation provides for a law that provides for the write-off of mortgage debt. We are talking about Government Resolution No. 373, effective from July 23, 2020. Subsequently, the law underwent several amendments, and in December the next edition was introduced, put into effect by the President of the Russian Federation (decree number 1331).

The essence of the program is to write off mortgage debt by 0.6 million rubles. It is also possible to change the lending currency (at the Central Bank exchange rate) or reduce regular payments for up to 1.5 years.

Debt reduction process

The mortgage upon the birth of the first child will not be repaid immediately with budget funds. Mortgage payments from the state reimburse the price of 18 m2 of living space. The subsidy for a mortgage at the birth of a child is calculated based on the cost of 1 m2 of residential real estate. Government assistance in writing off principal debt varies by region.

Documents for repayment of part of the loan should be submitted to the municipal authorities. A compensation scheme has been developed for young families. The law on writing off mortgages upon the birth of a child puts forward certain requirements for borrowers. If the parents comply, then the state will provide non-cash funds, which will be used to partially repay the loan. Russians who decide to take out a mortgage under the scheme for young families have the right to turn to the authorities for help if their income decreases.

The developed state program assumes that applicants must provide:

- parents' passports;

- a certificate confirming the birth of a child;

- document on family composition;

- information about place of residence;

- certificates of solvency confirming the ability to pay the mortgage Young family.

To provide state assistance in repaying a mortgage, the following is provided separately:

- mortgage agreement;

- documents for the premises;

- house book (extract).

State subsidies for mortgages are provided by transferring funds to the financial institution where the mortgage was issued and the contract was concluded. When a second child is born, the mortgage is paid off faster. The state issues compensation for 2 children for the next 18 m2. For 3 newborns, compensation for the mortgage at the birth of the child often occurs in full.

Regions of the state help young families with the birth of children and large families whenever possible. At the regional level, additional benefits are established for families with many children, and compensation is provided for mortgage loans. Adoptive parents have the right to receive a subsidy to pay off their mortgage. Mortgage benefits for the birth of a child are the same as for adoption.

State assistance in writing off the principal debt on a mortgage

A mortgage is a targeted loan that is issued for the purchase of housing. Its repayment occurs at the expense of funds credited by the borrower to the loan account.

Accordingly, debt repayment is carried out at the expense of the payer himself. Therefore, banks require the provision of documents on wages and encumber the purchased housing with collateral. This is done in order to guarantee repayment of debt on the main loan.

We advise you to read:

- ✅ How to reduce the current mortgage interest rate in Sberbank?

- ✅ Conditions for providing a military mortgage in 2020

- ✅ Mortgage with state support: conditions, features

- ✅ Do they provide maternity capital for 3 children?

At the same time, the state has developed and is implementing a number of measures aimed at providing assistance in repaying debts and reducing debt on such loans. These measures consist of providing funds to write off the underlying loan.

The amount that can be provided by the state is 600,000 rubles. But to receive this assistance, you must meet a number of conditions.

373 resolution on writing off the principal debt on a mortgage

This Government resolution was adopted in 2020 due to complications in the financial situation and a decline in the standard of living of Russians. Many families find themselves in a situation where they are unable to repay the principal debt with their income, since the amount of such income has decreased significantly.

To ensure that citizens do not lose their purchased housing for reasons beyond their control, the government has provided the possibility of subsidizing loan repayment and writing off 600,000 rubles of the loan.

This resolution contains a list of conditions under which citizens will be able to take part in this program:

- The basis for participation in the program is a serious reduction in income. It is necessary to prove that the current amount of earnings is one third less than it was when receiving the principal debt;

- The calculation takes into account the quarterly period before applying for subsidies. That is, you must submit documents for the past quarter on earnings;

- The decrease in income should also be justified with a salary certificate for the quarter that preceded the receipt of the mortgage.

Accordingly, if the difference between incomes during the specified periods of time is 30% or more, then the applicant will become a participant in the named government program.

Write-off of mortgage debt upon birth of a child

The birth of a child inevitably increases expenses. Accordingly, there will be less available funds and repayment of the principal debt on the mortgage will be more difficult. Therefore, upon the birth of a child, it is possible to receive government assistance in writing off and repaying the loan.

To do this, it must be proven that the payer repaid the debt on schedule and had no delays - he fulfilled his mortgage obligations in good faith.

But due to the birth of a child, increased expenses do not allow repaying the debt on time and in full. With written confirmation of a change in material well-being, it is possible to write off part of the mortgage loan at the expense of public funds.

Debt write-off conditions

At the same time, in the case where there are at least two or more young children in the family, one of the parents has a disability group or supports a disabled child as a dependent, and also, if we are talking about a combat veteran, then these categories of citizens have the right to receive 30% for writing off mortgage debt. However, this amount cannot be higher than 1.5 million rubles.

Government Decree No. 373 regulates the conditions under which the borrower can count on partial repayment of the debt. Depending on the content of the contract, the applicant will have to confirm the following circumstances:

- change in income – it is necessary to prove a decrease of at least 30% over the last quarter;

- the amount of income for each family member should not exceed two times the subsistence minimum (this indicator is approved quarterly at the level of the constituent entities of the Russian Federation);

- an increase in the monthly payment on a foreign currency mortgage by more than 30% compared to the date of execution of the agreement;

- social status - only families with children, disabled people or families with disabled children, as well as combatants.

An additional general requirement for all categories of borrowers is the deadline for applying for debt write-off - no earlier than one year from the date of concluding an agreement with the bank.

Only citizens who have purchased economy-class residential premises can obtain a write-off. When checking this condition, the following indicators are taken into account:

- standard for the number of rooms and living space - for a one-room apartment no more than 45 sq.m.; for a two-room apartment – no more than 65 sq.m.; for a three-room apartment - no more than 85 sq.m.;

- the price of the purchased housing cannot exceed the average market value of similar apartments by more than 60%;

- the above restrictions do not apply to families with three or more minor children.

Confirmation of these conditions occurs by contacting a bank accredited to participate in the federal program through AHML. To date, more than 80 banking institutions engaged in mortgage lending to citizens are accredited.

The algorithm for writing off debt is as follows:

- the citizen submits an application and a package of documents to the bank with which the mortgage agreement is concluded;

- after a preliminary check of the papers, they are sent to AHML to make a decision on the allocation of funds to repay the debt;

- After a positive decision, the funds are transferred to the bank, and a debt restructuring agreement is drawn up with the borrower.

These support measures cannot be reused; this benefit is a one-time type of assistance. This rule does not apply to filing tax deductions.

When repaying the principal debt for large families, the market value of housing is used - no more than 18 sq.m. must be paid. living space for each family member. This rule is applied simultaneously with the payment limits approved by the regulations of the constituent entity of the Russian Federation. The term of the loan agreement does not apply in this case; upon the birth of children, you can apply for payment at any time.

Is it possible to write off part of the mortgage debt after marriage?

I took out a mortgage for an apartment in 2020. And I got married this year, is it possible to somehow write off part of the debt under the financial assistance program for young families? Or in some other way?

Lawyers' answers

Kuznetsov Denis

Legislation and assistance programs for young families do not provide for any payments upon marriage. Such payments to young families are provided in some regions only at the birth of children. Young families (without children) can only be provided with preferential terms for obtaining a loan, with a smaller down payment and lower interest. However, changes to the programs are constantly being made; I recommend studying the current programs on the websites of the administration of your city and region.

The first and most important condition for participation in the state mortgage restructuring program must be that the borrower belongs to one of the categories established by law.

There must be evidence that the borrower is not bankrupt.

When receiving assistance for debt restructuring, the area of housing, the number of people living, and the purpose for which the loan was taken are taken into account.

How to participate in the mortgage loan forgiveness program?

Can everyone have their mortgage debt written off? The list of groups of citizens who can take advantage of the state program is presented below:

- Families with two children;

- Young families with one child;

- Employees of the innovation cluster;

- Former combatants;

- Scientists and members of the Academy of Sciences;

- Workers of a factory or city-forming enterprise;

- Government servants or officials;

- Families with a dependent under 24 years of age without income;

- Families where a child or one of the parents has a disability.

See also: Eviction from an apartment for mortgage debts

Real estate for which the principal mortgage debt can be written off must also meet a number of requirements:

- Be the only residence;

- Be “clean” in legal terms;

- The price per square meter should not exceed 60% of the average cost in the area.

Since 2020, there are also requirements for the debtor’s income - it must decrease (either for the borrower himself or for the family as a whole). The balance of money after paying off the monthly mortgage loan payment should be no more than two minimum subsistence levels per person, so that the family can take part in the government program and write off the principal mortgage debt.

Citizens who have gone through bankruptcy proceedings and are declared financially insolvent by the court cannot take advantage of this benefit. Also, a loan for an apartment or house must be targeted, and the overdue period must be no more than 4 months and no less than 30 days.

Refinancing or restructuring

Now you know what restructuring is. Let's find out its differences from refinancing. Refinancing is refinancing with another bank on more favorable terms. Typically, banks use refinancing of mortgages and car loans. If you have a loan agreement with a rate of 17%, and another bank has a program with 11.4%, and this is the real rate for a mortgage program with state support, then why not reissue this agreement?

After a positive decision from the bank, a new loan is issued to repay the previous one. And you pay less.

It’s difficult to say which is more profitable. Depends on the specific situation. If you find a good refinancing program with a significant difference in the annual interest rate, then the benefits are obvious

It is important that the new bank you choose approves your application. And for this, credit history is important.

Restructuring is a real way out of a difficult situation for a person who is faced with financial problems. Changes in exchange rates, bankruptcy of enterprises, layoffs at work, reductions in wages - all these troubles are very relevant, unfortunately, for most borrowers. Especially in recent years.

Loan debts began to grow like a snowball. Bank clients picketed branches, demanding changes to lending conditions. Considering that easing mortgage conditions is the only reasonable way out in a crisis, the banks agreed to meet them halfway. Mortgage restructuring is a necessary reality. Moreover, there are no more state-supported mortgages.

Today, it has become possible to restructure a mortgage, even with current debts and, as a result, a damaged credit history. In addition, the state came to the aid of people in difficult life situations.

Basic provisions of the law

Download Resolution 373. Resolution No. 373 dated April 20, 2015 provides the main list of organizations, a list of required documents, as well as the established procedure for processing write-offs.

The changes apply only to certain parts of the current law, which will certainly please a large part of debtors.

The decree states that in order to be able to provide assistance in writing off mortgage debt, the total regular income of the family must be less than 30%, when comparing the amount with the last 12 calendar months. This trend must be repeated for at least 3 months. After this, it is possible to submit an application to the relevant structures in order to receive support under the approved program.

The total amount of a one-time subsidy allocated to repay only one share of the mortgage loan should not be more than 10% of the total value of the remaining debt. Under existing conditions, it turns out that only people who have direct obligations to financial organizations in the amount of more than 6,000,000 rubles can count on financial support.

Which banks offer subsidies for mortgage repayments of 600 thousand?

It is necessary to understand that by writing off part of the mortgage loan debt to the client, in this case the bank does not incur losses. And by receiving 600 thousand rubles in mortgage compensation from the state, the borrower does not spoil the relationship with the bank. This also does not in any way affect his credit history. Therefore, the vast majority of banks issuing mortgage loans participate in the program under consideration.

But in any case, before you start preparing the documents necessary to receive assistance, you should check with bank employees about the possibility of receiving compensation when working with this financial institution.

The list of documents that must be provided to participate in this program to return 600 thousand on a mortgage from Sberbank or another credit organization may differ in each individual case (depending on the terms of the loan, the size of the mortgage and other factors), so this question should be check directly with employees of the bank whose client is the borrower.

A significant part of the adult population of Russia has a mortgage. It is problematic to pay off a loan debt on your own, especially during a crisis.

To help citizens cope with housing problems and reduce the amount of mortgage debt, the state offers the opportunity to participate in one of the special programs. Their main goal is to improve the living conditions of the population.

Currently, there are 2 main programs used to pay off mortgages at the expense of the state.

They have certain nuances and can only be applied to certain categories of citizens.

Thus, there are 2 main programs of state support for the population aimed at improving living conditions:

- providing a certificate for maternity capital to families with several children, adopted or natural (from 2 children or more);

- restructuring of a mortgage loan if citizens have problems with its payment (assistance is provided by a specially created agency - AHML).

You can determine whether you are suitable for one of them through consultation with the municipality of your locality, as well as after reading this article.

Program for writing off the principal debt on a mortgage at Sberbank

To receive compensation under the state program, you will need to go through the following steps:

- Visit a Sberbank branch

- Get advice from the employee about the possibility of receiving benefits and the appropriate method for this. And also get from him a sample application and a list of required documents.

- Fill out the application and collect all the necessary papers.

- Complete all certificates, some of which will not be free.

- Bring the collected package of papers to Sberbank.

Wait for AHML approval.

If approved, the agreement with the bank is rewritten and new conditions are added. Next, the mortgage is adjusted together with Rosreestr and the bank.

What documents will the bank need?

In addition to the application, the borrower will need to provide the following package of documents:

- Passport or other identification document.

- Financial documentation confirming the right to participate in the state program. This includes certificates showing the income of all family members. Certificates must be issued 3 months before taking out a mortgage for an apartment, as well as 3 months before submitting an application to the bank to order debt restructuring.

- A certified copy of the employment contract or work record book.

- Certificate of marriage or divorce.

- Child's birth certificate.

- Documentation for the property subject to mortgage - a cadastral passport of the apartment and a registration certificate.

- An agreement for participation in shared construction or a mortgage agreement.

- An extract from the Unified State Register, issued no more than 90 days before filing an application for debt restructuring.

The list of required papers may be subject to change. As an addition, it may also include:

- documents on the borrower's disability;

- documents on the disability of the borrower's children;

- ID card of a combat participant, etc.

What other federal programs exist?

Since 2011, citizens of the Russian Federation have had the opportunity to use a federal program that provides debt restructuring for young families. In this case, a reduction in the financial obligation of a young family to the bank is available.

To participate in the state program, several conditions must be met:

- The age of the borrower at the time of applying for a mortgage should not be more than 35 years. Applies to single-parent families as well.

- For each family member, housing should be allocated no more than 15 square meters. From this it follows that the program is valid only for economy class.

- The household must have enough funds to fulfill loan obligations on time.

- The family will need to prove the need to participate in receiving social benefits. hiring This means prioritizing the solution of housing problems within the framework of the actions of local self-government bodies.

Receiving compensation for mortgage payments through the federal program can be a significant help for both the family and the individual borrower. And despite the fact that for some of them the amount of compensation will be “a drop in the ocean” compared to the full cost of living space, the use of this state program helps save hundreds of thousands of Russian citizens. Therefore, it is worth asking in advance whether you have the right to take advantage of this benefit, and immediately take care of drawing up the appropriate mortgage loan agreement.

Dear readers! If you need expert advice on credit, debt and bankruptcy issues, we recommend that you immediately contact our qualified practicing lawyers:

Moscow and region

St. Petersburg and region

Options for writing off mortgage debt

First, we will tell you how you can legally write off mortgage debt. You need to choose which one is right for you based on the circumstances and characteristics of the situation in which you find yourself.

1. State program with the write-off of mortgage debt in the amount of 10% or 20% of the principal amount.

The state can compensate part of the debt. Until 2016, it was 10% of the principal debt, according to Government Resolution No. 373, but since December 2020 it was decided to compensate 20%. In other words, if with a mortgage loan of 5 million you have 2 million debt left, the state can compensate 20% - that’s 400,000 rubles.

This relief can be used up to 600,000 rubles. This is a threshold that cannot be exceeded under the current terms of the regulation. In order for you to take advantage of this government program, the apartment must cost more than 8 million rubles.

See also: Seizure of funds - what to do if your salary or pension has been seized?

2. Write-off of mortgage debts for large families.

There are certain benefits that come with having children. When the first child is born, the family has the right to compensate the cost of 18 sq. m. of housing. When the second child is born, the state covers the same amount. The third can completely help you write off 100% of your mortgage debt.

To completely eliminate mortgage debt, you need to contact the Pension Fund of the Russian Federation with a package of documents. You will need to bring:

- Certificate of maternity capital;

- Mortgage agreement with a credit institution;

- Marriage certificate;

- Birth certificates of three children;

- Documents confirming ownership of real estate with a mortgage;

- Certificates from the bank about the amount of debt remaining at the time of application.

First, you can submit copies of documents; you will be asked to provide the originals at the reception. After verification, the debt will be written off and the mortgage loan will be closed.

Important! To take advantage of this benefit, you must have a mortgage lending agreement under the state program with the bank. If this is not the case, you must first renew it, and only then contact the Pension Fund branch.

3. Write-off of mortgage debt when earnings decrease.

To write off part of the principal debt on a mortgage due to a decrease in income, you need to document this. To achieve this, wages must be reduced by more than 30%. After this, 3 months must pass before you can apply for debt restructuring.

A similar situation is possible if the mortgage loan is in foreign currency. In this case, if the exchange rate changes and the monthly payment increases by more than 30%, while maintaining the level of wages, the debtor can apply to write off the principal debt on the mortgage.

Resolution 373 on writing off the principal debt on a mortgage

This decree, issued by the government, was put into circulation on July 23, 2020. The federal mortgage principal debt forgiveness program contains a number of criteria by which citizens can take advantage of these benefits.

These are those categories of the population whose families have a minor child, families in which there is a disabled child, families in which one or more members are participants in hostilities, and employees of government agencies also enjoy a similar advantage: health employees, scientific research employees, and so on.

The body responsible for this aspect is the housing mortgage lending agency.

Conditions for writing off the principal debt on a mortgage

To receive assistance in this program, family income must decrease by more than 30% compared to the previous twelve months. This trend must be observed for three months, after which it is possible to apply for support in this program.

The second option of contacting an agency in order to receive subsidies from the state contains the following conditions: after the borrower has paid the monthly mortgage payment from the general budget of one family, his savings must be less than two subsistence minimums for any family member.

The cost of living is set by our state, depending on the economic situation in the country, as well as on the level of inflation. The cost of living is based on the consumer basket; it can change several times a year.

Borrowers facing financial problems cannot get money in their hands. Because the loan officer carries out a restructuring of the mortgage, and only after this the state compensates for the funds.

The limit for the amount of debt write-off in number is 600 thousand rubles. In the first edition of such a resolution, the maximum write-off amount was 200 thousand rubles, then the state decided to improve the conditions under the federal program in order to help the country's population, especially young families.

A one-time subsidy for repayment of one share of a housing loan should not exceed 10% of the total value of the remaining debt. According to these conditions, it turns out that only those citizens who have obligations to the bank of more than six million rubles are entitled to apply for financial assistance.

Such assistance to citizens is not provided in one day; this program is a very long process. To submit an application to the agency, the loan obligations must be at least a year old.

Who is entitled to write off loan debt?

State assistance in writing off the principal mortgage debt is provided to those categories of the population that:

- They take part in the regional program “Affordable Housing for Young Families.” Many Russian commercial banks create loan products under similar names, so you should be careful when choosing a bank and what it offers. Because credit products of commercial and savings banks do not provide any subsidies for citizens, but only provide more or less favorable conditions for repaying the debt amount;

- They live permanently in an area where some of the mortgage loans, subject to the birth of a child, are actually compensated.

The state plans to introduce several more similar projects in the future. For example, the state undertakes to repay about 10% of the cost of the mortgage for the birth of the first child, with the second child about 30%, when about 40% are born. These programs are only in projects; it is unknown when they will be implemented.

Sberbank writes off the principal debt on a mortgage up to 600 thousand rubles

As we already know, the maximum assistance from Sberbank can be 600 thousand rubles, which is more than twice the original limit of 200 thousand rubles. Along with increasing the limit, the government decided to ease the circumstances for mortgage lending. According to the new standards, an apartment taken on a mortgage must be a single living space that is in the possession of the owner. Also, an applicant for subsidies from Sberbank has the right to own other housing in Russia, but so that their total share in no case exceeds 50%. Receiving the treasured 600 thousand rubles. possible in several ways:

- The first option is a one-time payment to the borrower’s current account, in which case the amount is written off instantly;

- The second option is to reduce the monthly mortgage payment to 18 months.

Write-off of the principal debt on a mortgage - government program

The most popular is the state program intended for families with two children, young families with a child under 18 years of age, if there is a disabled child or dependent under 24 years of age without official employment. In addition, the program works for workers of a number of factories and enterprises, database participants, employees of companies under the auspices of the Russian Academy of Sciences, and so on.

You can write off your mortgage debt if you meet a number of requirements:

- To the property. The apartment should not be classified as elite, and the area for one-, two- or three-room housing should not be more than 45.65 and 85 square meters, respectively. The price of one “square” of real estate purchased with a mortgage should not exceed the cost of sq.m. of typical real estate in the region by more than 70%.

The price of typical apartments is determined by the Federal Social Insurance Fund of the Russian Federation on the day of signing the mortgage loan.

- By the date of execution of the agreement, Resolution No. 373 states that the program is available for mortgage loans issued before the beginning of 2015. In subsequent versions, the limit parameter is not fixed. Only one requirement is specified. In particular, from the date of execution of the contract to the writing of the restructuring application, 12 months or more should pass.

- To the income of participants. At first, writing off mortgage debt was available only when there was a delay. According to the new version of the law, an application is allowed to be submitted before the debt arises. This approach allows you to maintain an ideal credit history. To receive the service, family income must decrease by more than 30% compared to previous data.

Having a mortgage debt to the bank is not a problem if you use one of the options offered.

You can also consult with specialists and decide on a suitable solution. Debt consultation

Write-off of part of the mortgage debt under the federal program “Affordable Housing for Young Families”

This federal project has been operating since 2011.

Its feature is the possibility of writing off part of the financial obligations for a young family, as well as the cost of 18 m² upon the birth of the first or second baby. If during the period of servicing debt obligations 3 children were born in the family, then the state fully repays the targeted loan. To participate in the program, citizens must meet the following requirements:

- Age at the time of applying for a mortgage should not exceed 35 years. This requirement also applies to single-parent families.

- Each family member should have no more than 15 square meters. This means that the program applies only to economy class real estate.

- The family's need to receive a social mortgage must be proven, that is, it must be in line for a solution to the housing problem in local governments.

- The household must have money to fulfill loan obligations in a timely manner.

The procedure for writing off part of the mortgage for a young family

As part of the program, citizens are given a state subsidy for the purchase of housing on the primary real estate market or participation in shared construction. It amounts to up to 30% of the cost of the apartment for households without children and up to 35% if the borrower has one child at the time of applying for a mortgage.

To write off part of the mortgage, a young family must provide the following documents to the municipal housing committee:

- passport of each spouse;

- child’s birth certificate (if the borrower has a minor child at the time of applying for a mortgage);

- certificate of family composition (document in form 9);

- information about the family’s place of residence for the last 5-7 years;

- certificates confirming the solvency of the household (certificate in form 2-NDFL for 6 months, statement from a deposit account, etc.).

Ways to write off mortgage debt

They depend on the direction of state aid and the region of residence of the debtor. The main thing is to confirm the grounds for providing assistance. We list the main support measures.

Foreign currency mortgage

If you take out a mortgage in a foreign currency, you can count on:

- application of a more favorable rate than that existing on the foreign exchange market;

- transfer of the principal amount into Russian currency at a preferential rate (the value of the exchange rate difference below the current rate is used);

- application of a reduced interest rate after transferring the loan to rubles - up to 11.5% per annum;

- repayment of the principal debt in the amount of up to 600 thousand rubles, if due to exchange rate differences the monthly payment amount has increased by 30%;

- writing off part of the mortgage debt;

- temporary reduction in the monthly payment amount (up to 50% for a year and a half).

Ruble mortgage

For citizens who have taken out a housing loan in rubles, the following measures are available:

It is understood as a change in the payment schedule - the loan term becomes longer, and the monthly payment becomes smaller. At the same time, the overpayment on the loan will increase.

- Repayment of part of the debt at the expense of the state

The federal program provides for the possibility of repaying up to 10% of the balance of the principal debt, but not more than 600 thousand rubles. In this case, you will have to document that the amount of income per family member has seriously decreased.

- Interest rate reduction

If you are a young family, pay attention to the special conditions provided by local bank branches. Families with children whose second or third child was born in 2020 can count on loan refinancing at a rate of 6%.

- Receiving a tax deduction

You can return part of the personal income tax paid at the place of employment. Typically they return 13% of the previous year's income. It is important that you are officially employed, and that your employer regularly pays taxes to the treasury.

The law allows you to return part of your personal income tax under the following conditions:

- you can refund the entire amount of interest you paid for the past year;

- the amount of compensation cannot be higher than 13% of the personal income tax actually paid for the previous year;

- You can receive a deduction annually.

To take advantage of government assistance, you need to contact the bank that issued the mortgage. You will need to submit an application and collect a package of documents confirming your difficult situation.

You can use several types of help at once.