Refund of mortgage insurance - three ways in 2020

The ability to return money for an insurance policy depends on the type of contract, the term of the loan and the circumstances under which the borrower decided to refuse insurance. Before you start the refusal procedure, you should weigh the pros and cons. You definitely need to think through your actions in case an insured event does occur. After all, then the borrower can only rely on himself.

Mortgage loan insurance

Obtaining a mortgage loan involves taking out several insurance policies. If a bank takes real estate as collateral, it must be under financial protection. This is a mandatory type of insurance, with the exception of land plots. Buildings and apartments are insured against structural damage due to unforeseen events (fires, floods, aircraft crashes, etc.).

Another thing is financial protection of the client’s health and life. It is not necessary to formalize it; the bank does not have the right to impose it, much less threaten to refuse to issue a mortgage. If this happens, you can safely complain to the Central Bank of Russia about the unlawful actions of the lender. Although banks have now begun to act differently, the terms of the mortgage product stipulate an increase in the interest rate in the absence of life insurance. In terms of the long-term loan term, the result is a considerable overpayment, so it has become even profitable to arrange financial protection, because its cost turns out to be less than the amount of overpaid interest.

The mortgage client should be aware that this type of insurance protects his family from paying off a huge debt if he were to suffer an accident. In the event of the borrower's death or disability, the insurance company will cover the bank debt, and the apartment will remain the property of his relatives.

Another voluntary type of insurance is title insurance. It is recommended to register it within three years after registering a real estate transaction. This period was not taken by chance; the law determines it for filing a statement of claim to annul the purchase and sale. After this period, there is no point in having title insurance.

To save money, you can take out a comprehensive policy that includes two or more insurance risks. Payment is made every year or for the entire loan repayment period, it all depends on the conditions of the insurance company.

Types of mortgage insurance

Credit insurance can be divided into two types:

- Voluntary, in case of illness, loss of income or death.

- Mandatory, is insurance in case of unforeseen circumstances. In this case, the purchased housing becomes the collateral property of the bank.

Payment can be made in the following ways:

- Single payment. You can pay the entire amount at once or spread it over months.

- Annually. In this case, the client reissues the policy every year. Banks often allow refusal to renew insurance after a certain loan period.

This is important to know: Application for inclusion of documents in the case materials under the Code of Civil Procedure of the Russian Federation

Can I get my mortgage insurance back?

According to legislative norms, each borrower has the right to return the funds spent on insurance. In this case, part of the amount will be withheld. The amount of the penalty will depend on the term and conditions of use of the policy.

The client can receive the full amount if the mortgage agreement has not yet entered into force.

If the borrower wrote an application immediately after concluding the contract, then the repayment period is no more than three months. In this case, only part of the insured amount is returned.

Three ways to return insurance

The return of insurance largely depends on the conditions specified in the contract and the period during which the policy was used.

There are three insurance return options:

- If no more than a month has passed since the conclusion. If the contract came into force from the date of signing, then the amount is paid minus the days used. If the contract is deferred, the entire amount is returned in full.

- If 1 to 3 months have passed. Part of the insurance amount is returned. In this case, the bank sets the size of the retained share at its discretion. In some organizations, the amount of the penalty can reach 50%.

- Starting from 3 months of using the loan until full repayment. In this case, an amount is paid that is a multiple of the remaining loan term.

Thus, the insurance can be returned at any stage of using the loan. It is important that when an insured event occurs, the obligations between the borrower and the organization are considered fulfilled. In this situation, a refund is not possible.

General information

This condition is specified in the text of the loan agreement itself and its violation entails certain financial sanctions. You can find out what may happen in the event of a delay under the insurance agreement in the terms of the mortgage agreement itself.

More often than not, delays under an insurance contract occur due to the carelessness or forgetfulness of borrowers. But there are cases when contributions under an insurance contract are stopped intentionally, due to lack of money, in the hope that no sanctions will follow, out of a desire to save on additional expenses for the mortgage.

Typical delay situations:

- Forgot to renew the contract

- They deliberately did not renew it after the expiration of its validity period, if it was concluded for a period less than the term of registration of the mortgage,

- Forgot or missed another insurance payment.

Missing an insurance payment or not renewing it may well go unnoticed by either the bank or the insurance company, and the borrower may not even receive notification of a delay. This scenario is especially likely if the borrower pays the mortgage on time and there is no reason to doubt his solvency. But this doesn't happen often.

As a rule, insurance company representatives are the first to respond. They act proactively, warning in advance about the next payment or the need to extend the contract. In case of delay, the information is transferred to the bank that issued the mortgage. And it is from the bank that sanctions may follow in this regard.

Sanctions that can be applied by the bank in case of delay in insurance:

- Penalties (0.5-1% of the overdue amount), fines, increased interest rates (up to 20%) and other financial sanctions,

- Assignment of the amount of the penalty in the absence of a concluded insurance contract for the property,

- Write-off of the monthly mortgage payment to pay for the insurance, so the debt will accumulate on the mortgage, and not on the insurance,

- Requests for early repayment of the loan balance,

- Reducing the amount of insurance payment upon the occurrence of an insured event,

- The bank's appeal to the court for violation of the essential terms of the contract, which includes insurance of the collateral or the life/health of the borrower.

The imposition of any sanctions is possible only if they are specified in the text of the lending agreement. In most cases, banks limit themselves to imposing additional fines or changing the terms of the loan. The bank will apply to the courts only in case of significant delays, otherwise the legal costs will significantly exceed the benefit received.

How to get your mortgage insurance back

Since, when applying for a mortgage, the home remains pledged to the bank, many believe that the insurance cannot be returned. The bank and insurance company are also in no hurry to inform the client on this issue. Therefore, first of all, you need to familiarize yourself with the terms of the contract, it is worth paying attention to the presence of a clause on the possibility of returning funds paid. There are a number of circumstances in which refusal of insurance has its own nuances.

In case of early or planned repayment of the mortgage

If the loan is repaid on time, according to the payment schedule, then all obligations between the parties are considered to be fulfilled. In this case, claims for the return of insurance are unfounded. In case of early repayment, you can return the insurance amount in proportion to the number of unused days of the loan.

To return the insurance in this case, it will be enough to contact the insurance organization with a corresponding application. Documents confirming loan repayment will need to be attached to the application.

After the death of the borrower

In the event of the borrower's death, all mortgage obligations pass to the heirs. They need to inform the bank about the event as soon as possible. All issues related to payments, as well as re-registration, are suspended until the entry into inheritance rights.

If life and death insurance was previously taken out, the money goes to pay off the mortgage. Refunds are not possible in this case.

If life insurance has not been issued, then all obligations on the loan are assumed by the heirs. In this case, both the loan itself and the mortgage insurance are reissued. In this case, all previously paid funds are taken into account.

This is important to know: How to get money back for consumer credit insurance

The new owner can refuse the insurance policy if he does not agree with its terms. To do this, you need to contact the insurance company with a free-form application. The money will be returned in an amount proportional to the unused time of the loan.

When refinancing

Mortgage refinancing involves re-issuing a contract on new, more favorable terms. Accordingly, the insurance coverage becomes invalid. In these cases, the borrower can choose one of the following options:

- You can extend the policy. If the contract is renewed in another bank, then it is necessary to clarify whether they work with this insurance organization.

- Close the contract and return the remaining funds. The operation is only possible if the new bank is unable to cooperate with the insurance company.

Thus, repayment of the mortgage upon refinancing is possible. But since when concluding a new contract, a mandatory condition will be the conclusion of a new insurance agreement, it will not be possible to return the funds.

In order to close an insurance contract you need to:

- Contact the bank with a notification of your intention to carry out the refinancing procedure with another organization.

- Write an application to the insurance company to terminate the agreement and return unused funds.

- After refinancing, renew the insurance contract with the new organization.

To receive a refund, you do not need to wait until the renewal of the contract is completed. These procedures can be carried out in parallel to each other.

Unilaterally, if a service has been imposed

You can get your money back in situations where the bank took out insurance against the client’s will. To do this, you may need proof of imposition of the service.

To terminate the contract, you need to write an application for the return of the amount of money. As a reason, you can indicate the fact of imposing a service. If the answer is negative, file a lawsuit.

Imposing a service is considered an activity contrary to the legislation of the Russian Federation. As a rule, claims in court are satisfied in favor of the plaintiff. But due to the fact that it is difficult to prove the fact of compulsory insurance, the full amount can be returned only if the contract has not entered into force. In other cases, you can only count on part of the funds.

How to justify refusal during registration?

Undoubtedly, the client has the right to refuse life insurance immediately when applying for a mortgage.

In this case, the bank offers the borrower a different lending program, which contains more stringent conditions for issuing borrowed funds. As a rule, they are associated with an increase in mortgage rates.

In addition, the borrower

has the opportunity to refuse life and health insurance immediately after purchasing a home using a mortgage.

This can be done during the so-called “cooling off period”, which lasts 14 days from the date of conclusion of the contract.

In this case, the policyholder will be fully (if the insurance contract has not entered into force) or partially (if the insurance has entered into force) refunded the amount of the insurance premium.

If the policyholder decides to refuse life insurance a significant time (1 year or more) after the conclusion of the contract, this can have very negative consequences.

But, we must take into account that the bank may significantly increase the mortgage lending rate or even require repayment of the loan ahead of schedule.

Features of military mortgage insurance ►►

Causes

It should be noted that the borrower is not at all obliged to indicate the reasons for refusing life and health insurance under the mortgage, since the acquisition of this type of policy is carried out on a voluntary basis. No one has the right to force a client to take out such insurance.

In most banks, in the application form for refusal of life and disability insurance, there is no column at all in which it is necessary to indicate the reason for reluctance to take out insurance.

Legislation to help

At the legislative level, the borrower is not required to provide life and health insurance when applying for a mortgage.

This procedure is entirely voluntary.

In accordance with paragraph 2 of Article 31 of the Federal Law of the Russian Federation “On mortgage (mortgage of real estate)”, the borrower must insure only the mortgaged property itself , that is, the mortgaged property.

Terms and conditions of the mortgage insurance contract ►►

Therefore, if the bank forcibly insists on issuing a life and disability insurance policy, the borrower has every right to write a complaint to the appropriate authorities, where he argues for the right to refuse mortgage insurance.

What will you need?

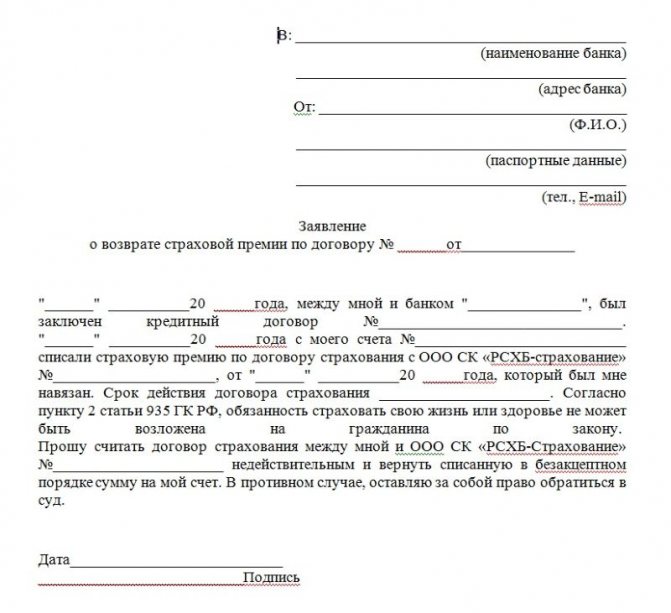

To contact an insurance company you will need the following package of documents:

- Passport or other identification document.

- Insurance policy.

- Application for return in two copies.

- A bank statement confirming that the mortgage was repaid ahead of schedule.

- Mortgage agreement.

- A document confirming that the encumbrance on the property has been lifted.

Depending on the circumstances under which the borrower wants to terminate the contract, the company may require additional documents.

Algorithm of actions

The procedure for returning mortgage insurance is usually straightforward. The collected package of documents can be sent to:

- by personally contacting the insurance company;

- by sending by registered mail with notification;

- by email.

Expert opinion

Alexandrov Dmitry Petrovich

Practicing lawyer with 15 years of experience. Specializes in family law

The review period is 3 months from the date of receipt of the application. You can submit an application through bank employees without visiting the insurance company. The possibility of such a service must be clarified at the branch where the loan was issued.

This is important to know: Complaint against a decision on an administrative offense: sample

What types of insurance are issued for a mortgage?

A mortgage is a special type of loan. When applying for it, there is no way to refuse insurance, since the collateral for the loan is real estate. Banks, of course, are unprofitable if something happens to the collateral. Concerns regarding insurance maintenance fall on the client's shoulders, but if situations stipulated by the contract occur, he will be able to receive compensation. Read about how to use the loan insurance service here.

Current offers

| Bank | % and amount | Application |

| Alfa Bank Mortgage | 6.5% Up to 45 million rubles. | Direct application |

| Rosbank Quick solution | 6.39% up to 25 million rubles. | Direct application |

| Bank Otkritie Large amount | 6.5% Up to 150 million rubles. | Direct application |

Loan without refusalLoan with arrearsUrgently with your passportCard loans at 0% Installment cardsEarning money from home

Mortgage insurance can be taken out for the entire term of the loan or renewed annually. In both cases, it is allowed to initiate the return of unused funds upon early repayment of the mortgage. This link tells you the best way to pay off your debt ahead of schedule.

Loan without refusalLoan with arrearsUrgently with your passportCard loans at 0% Installment cardsEarning money from home

Later in this article:

Dangerous turns from insurers, or how to protect yourself

There can be many pitfalls when applying for a mortgage. One of them is credit insurance. A standard contract is drafted with the help of lawyers, which allows companies to make terms favorable to insurers rather than clients.

The law provides for the borrower's right to introduce his own terms into the contract. In practice, the client most often faces the bank’s refusal to take such action. Therefore, before resolving such issues, it is worth using the services of lawyers. The specialist will also help you wisely avoid the procedure of imposing insurance.

Another obstacle may be the refusal of insurance. The client may be convinced that this is impossible, or they may charge illegal fees and fines. In this case, an effective way would be to go to court.

At the pre-trial stage, you can try to resolve the issue by filing a complaint with Rospotrebnadzor or the prosecutor's office.

Borrower's actions in case of insurer's refusal

It happens that there are all reasons for a return, but nevertheless an unfounded refusal occurs. In such a situation, you can send an appeal to the insurance company asking for justification for the refusal.

The letter must indicate the reason for termination and attach the following documents:

- Passport or ID.

- Mortgage agreement.

- Insurance policy.

- Payment schedule.

- Documents for purchased housing.

- Confirmation of early payment of the mortgage.

- Details of the current account to which the funds must be returned.

If the amount returned is less than expected, you should request a calculation of the insurance invoice.

If the insurer refuses to refund even if you apply again, then the next step will be to go to court. In addition to the basic mortgage documents, written responses from the insurance company should be attached to the claim. As practice shows, the chances of a positive decision are usually quite high.

To complete the application you will need

- passport;

- mortgage agreement;

- payment schedule;

- certificate of absence of debt on the loan;

- insurance contract;

- policy (if available);

- documents for the apartment;

- account details for transferring money.

What salary is needed to get a mortgage at Sberbank ⇒

When submitting an application, you must ensure that it has been accepted. To do this, an employee of the insurance company must put an acceptance mark on the paper. If the application is refused, it must be sent by registered mail with notification.