How to reduce the mortgage rate at Sberbank? Conditions for obtaining a mortgage at Sberbank

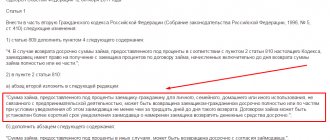

- Convince the bank that the funds requested by the borrower will be guaranteed to be returned.

- Find out about all the necessary nuances, including current agreements and internal policies of the organization (the availability of a mortgage loan with a lower rate, for example).

- Compose and submit an application, for which you need to consult with the manager.

As a result of these checks, it will be decided whether or not to issue a mortgage loan to each borrower individually. If a client is denied a loan, he must keep in mind that the funds spent on processing the application are not refundable. The final cost, of course, is unlikely to exceed 5-10 thousand rubles, but the client should always understand what risks he is taking when contacting the bank.

Methods for removing collateral

After repaying the mortgage, many citizens try to quickly carry out the procedure for removing restrictions from the apartment in order to be freed from obligations and have unhindered actions with the property. You can make a withdrawal in several ways:

- through a bank branch;

- contact multifunctional centers;

- submit an application through the State Services website or DomClick.

Official confirmation of the lifting of the ban on housing is provided by the state body - Rosreestr. As soon as the debt is repaid and the documents are collected, the application will be considered and the client will be given a certificate of unlimited rights to the property. It is worth knowing that if the sale of an apartment occurs before the mortgage is repaid, the encumbrance is removed only after the rights are transferred to the new buyer.

Thanks to the development of technology

Through the MFC or the State Services website

When opening additional organizations for the provision of public services, citizens can carry out the procedure without contacting a bank branch. If the client has access to the State Services website, then he can submit an application from a desktop computer connected to the Internet. When contacting the MFC, the list of documents listed above is provided, and the employee himself carries out the sequence of actions. The services’ algorithm is easy to use and does not require specific skills.

Using DomClick

In addition to standard methods of removing encumbrances, Sberbank clients have access to the DomClick service. To do this, you need registration data and an Internet connection. The process goes like this:

- After full repayment, the borrower must wait 30 days.

- In the second month, if the encumbrance is not removed, the client can use the DomClick service.

- The application is submitted on the website in a special category. Thanks to modern developments, the borrower will be able to track the status of the application at any time.

- Consideration and satisfaction of requirements takes a certain time, after which the applicant will receive an official response about the lifting of restrictions in the form of SMS information.

The application is popular, but can only be used by clients who have registered with this service.

Exchange of mortgage apartment

- Repay the loan in full. This solution is not suitable for everyone, since the amount of the one-time payment is quite large.

- Transfer the debt to a third party. Banks are reluctant to undertake such a procedure, as this significantly worsens the quality of the loan to the Central Bank of the Russian Federation.

- Replacement of collateral. That is, an exchange of a mortgage apartment.

- Part of the mortgage loan should already be repaid without delays. As a rule, banks allow exchange after 4–5 years of regular payments.

- The new apartment should be 20–30% cheaper than the first collateral. That is, the cost of the new collateral, taking into account interest on the loan, should be lower.

- New housing should not be located “in a bad corner.” The bank will never allow you to buy an apartment in a region that is not serviced by this bank.

Is it possible to exchange an apartment with a mortgage and how to do it

- The exchange involves replacing the existing collateral, that is, re-issuing a mortgage on another property.

- The bank may give its consent to replace the collateral, but it is not obliged to do so.

- The replacement process is regulated not so much by the loan agreement concluded with a specific borrower, but more by the internal provisions, instructions and regulations of the bank (some lenders may allow an exchange only after the debt has been repaid for more than half of the loan term, others are not strictly tied to the date of the transaction).

- Exchange of one apartment for another is possible only if the client has a positive credit history (no long-term arrears).

- The purchased property must cover the balance of the debt (including accrued interest) with a discount of at least 20-30%.

- title papers (certificate of ownership);

- an extract from the house register indicating all those registered in a particular property;

- cadastral passport of living space;

- a certificate from the governing body confirming that there are no debts for housing and communal services (for example, a certificate from a HOA);

- real estate appraisal report completed by an accredited appraisal company.

Please note => How to calculate the average salary per year calculator

Sberbank standard mortgage agreement 2020

- possibility of early repayment of debt (no moratorium or fines);

- penalties (the bank does not have the right to levy fines from the borrower for actions that were not specified in the concluded agreement - for example, an illegal requirement to pay a fine if money is not written off to the loan account through no fault of the client);

- the opportunity to refuse to purchase an insurance policy (we are talking about comprehensive insurance, including insurance of property, health and life of the borrower).

The main reason why a prenuptial agreement is needed for a mortgage transaction is that one of the spouses does not meet Sberbank’s requirements for a borrower (bad credit history, problems with the security service, foreign citizenship, insufficient solvency, etc.)

How to reduce the mortgage interest rate at Sberbank

This saving option is best suited for the initial stage of using a mortgage loan using the annuity method of making payments, when they are made monthly and the payment amount does not change throughout the entire loan term. Given the differentiated nature of mortgage payments, the interest rate reduction is relevant throughout the entire loan period. A win for the borrower is possible here if there is a significant difference in the rates.

Other factors influencing the advisability of refinancing are the absence of restrictions in the Sberbank loan agreement with the client in the form of a temporary moratorium on early repayment of an existing loan and the moment when the difference between the rate of the existing and newly concluded loan agreement is no more than one or two percentage points. The overpayment must be reduced by an amount greater than the amount of additional costs for changing the current agreement with Sberbank.

Agreement for the purchase and sale of an apartment under a Sberbank mortgage

6.3.13. If there are minors, incapacitated persons and persons with limited legal capacity, who in relation to the purchased Apartment will be co-owners of the Buyer-Pledgor or members of his family, submit the consent of the guardianship and trusteeship authorities to transfer the Apartment as collateral and its possible alienation in the event of failure to comply with the terms of the Credit Agreement agreement.

Gr. , passport: series, No., issued, residing at: , hereinafter referred to as “Seller”, on the one hand, and gr. , passport: series, No., issued, residing at the address: , hereinafter referred to as the “Buyer”, on the other hand, hereinafter referred to as the “Parties”, have entered into this agreement, hereinafter the “Agreement”, as follows:

How to change an apartment with a mortgage to another

Housing loans are usually issued for quite a long time, for tens of years. During this period, changes may occur in the borrower’s life (the birth of children, an increase or decrease in income, etc.), which will lead to the need to exchange the apartment under the mortgage. However, due to the fact that the housing is pledged to the bank, the procedure is complicated.

- Passport (copy and original)

- Statement

- Marriage certificate (if available)

- Loan agreement

- Copy of personal account

- Extract from the house register

- Written consent of those registered in the apartment

- Title documents for the second apartment

- Documents that confirm that payments were made on time

- Other papers.

Please note => How many times does an individual entrepreneur pay taxes per year?

Exchange of an apartment with a mortgage: 3 ways to move

In this case, the procedure becomes even more expensive and time-consuming. You will have to simultaneously submit an application for approval of the sale of your mortgage home and an application for pre-approval of a new loan. Often such approval occurs according to a simplified procedure, if there are no problems with repayment under the current agreement and the quality of the new collateral is satisfactory to the lender.

If the situation when it is necessary to exchange an apartment is related to the direct transfer of a military personnel to another city for service, then the agreement provides for an exchange under the “Moving” program. The procedure is similar to that described above for an equivalent exchange; the collateral is changed. The only requirement is that the housing chosen for moving must be similar to the collateral property and be located at the place of service of the person liable for military service.

What exchange options there may be: their pros and cons

You can change your apartment mortgage using several options, each of which has its own characteristics, pros and cons. Let's look at each in detail.

Removal of the bank's encumbrance on the collateral property and its sale with the purchase of a new one

This mortgage housing exchange option will be preferable for those borrowers who plan to buy a new apartment with a larger area and, accordingly, a higher cost.

In this case, the transaction will be carried out by paying off the balance of the debt using your own funds or attracting a regular consumer loan. In order to sell an apartment pledged by the bank, you must obtain its permission for such a procedure and, additionally, to remove the encumbrance from it.

Read also: Payment for Krasnoyarsk transport card

As practice shows, banks are reluctant to undertake such operations due to increased risks. The benefit here is only for the client who improves his living conditions.

The process of removing encumbrances from collateralized real estate and its sale with the simultaneous acquisition of a new one includes the following steps:

- Obtaining permission from the creditor bank to sell the encumbered property and simultaneously applying for a new mortgage.

- Repayment of the remaining debt under the current contract and subsequent removal of encumbrances from the property.

- Searching for a buyer for an apartment and concluding a purchase and sale agreement.

- Search for a new apartment (a sales contract is concluded in a similar way).

- Conclusion of a new loan agreement.

- Encumbrance of a new pledge with the registering authority.

For the buyer of an old apartment there will be no disadvantages, since he is purchasing the property without any encumbrance.

Read more about whether it is possible to sell an apartment with a mortgage and how to do it.

Replacement of collateral with the approval of the bank for another

An alternative option for exchanging an apartment with a mortgage for another is a simple change of collateral by concluding an exchange agreement. The conclusion of such an agreement will be relevant only if the cost of the two objects is almost identical. This fact is established by the interested creditor bank.

The process of replacing the collateral in this case will be carried out in the following order:

- Obtaining the bank's consent.

- Providing a complete package of documents for a new living space.

- Assessment of new living space and clarification of mortgage terms for the upcoming transaction.

- Signing the exchange agreement.

- Transfer of a new apartment as collateral to the bank.

- Removing encumbrances from old real estate.

Such a transaction has a number of difficulties in its implementation, since among the owners of real estate there are few people who are ready to agree to exchange an apartment pledged by the bank.

Sale and purchase of an apartment in one bank with a mortgage

This method of exchanging mortgage real estate is the most preferable for the bank, as it has minimal risks. In simple words, the borrower sells existing real estate with the permission of the bank and buys a new one, also using borrowed funds (with an additional payment through a mortgage).

The procedure consists of the following steps:

- Obtaining official consent from the bank and applying for a new mortgage.

- Putting an old apartment up for sale and concluding a purchase and sale agreement with the buyer.

- Search for the apartment to be purchased (a purchase agreement is also concluded).

- Registration of a transaction for a new mortgage loan.

- Removal of the old encumbrance and transfer of a new apartment as collateral.

That is, there is a simultaneous process of selling an old apartment and buying a new one. To reduce possible risks, you can use safe deposit boxes for payments.

Organizationally, such a deal can be completed in one day.

Separately, it should be said that exchanging a mortgaged apartment for a cheaper one will be extremely difficult. In this case, it will be almost impossible to obtain permission from the bank, since not a single bank will agree to deliberately reduce the liquidity of the collateral.

You can get out of this situation with the help of a double purchase and sale agreement for both real estate properties, when the first apartment in the mortgage is sold after the encumbrance is removed. This was discussed above.

How to reduce your mortgage rate at Sberbank

- Reducing the interest rate is not the responsibility of the bank. He can do this not only in the name of the client, but also so that he is not lured to another bank.

- It takes at least 7-10 days to process the application. In practice, this period can reach 120 days. You need to find out about the status of your application yourself. The most convenient way to do this is through your Sberbank Online personal account.

- The size of the interest rate reduction is different for everyone. The new rate will not be set below 12%. But for some, this difference can be 2%, and sometimes more.

Also read: Is it possible to arrest the property of a woman with a young child?

After reviewing the application and the rest of the package of documents, a Sberbank specialist informs about the decision made. Usually the entire procedure takes about 8 – 10 days. In this case, the lending conditions must comply with the standard conditions of the bank. For example, the loan term cannot be more than 30 years.

How to reduce your mortgage interest rate

- Find out all the necessary nuances about the organization’s internal policies (for example, the availability of future mortgage loans at lower rates) and existing agreements.

- Compose and submit an application. For these purposes, you need to contact the manager.

- Be sure to comply with all requirements stated by the lender.

- Provide the necessary guarantees that the requested funds will be returned.

Firstly, the new bank also checks the solvency of the potential borrower. In this case, the positive payment history of another lender is not taken into account. Secondly, a similar check is carried out for the real estate provided as collateral. And the fact that another lender already reviewed it some time ago is also irrelevant.

Mortgage in 2020 in Sberbank

The basic programs are practically no different from each other. There are no fees for signing and maintaining the agreement; the rate depends on the loan term and the amount requested by the borrower. Individual benefits are provided for persons receiving a pension/salary from Sberbank. All programs include a fine/penalty for late payments.

The most advantageous offers are reflected in special mortgage programs. Thus, a family with children in which one of the spouses has not reached the age of thirty-five can count on participation in the “Young Family” program. According to it, the down payment amount is ten to fifteen percent, and parents can be involved as co-borrowers. For program participants, all types of income are taken into account, not just officially confirmed ones. If, after signing a mortgage agreement, a child is born in the family, the bank provides a deferment on loan repayment for a period of one year.

How to remove an encumbrance from an apartment in Sberbank: procedure

Cases when the encumbrance is lifted:

- in the event that the borrower cannot pay the mortgage loan and sells the apartment (the collateral) in order to pay off the debt to Sberbank;

- after full payment of the mortgage loan;

- when selling an apartment before the loan is fully repaid, when the buyer (new owner) fully repays the debt of the seller (former owner);

How this happens : according to the contractual relationship between a credit institution (Sberbank) and an individual, after full payment of the loan amount for the purchase of an apartment, the bank cancels the mortgage record in Rosreestr.

Documents for carrying out the procedure at Sberbank:

- identification document (s) of the borrower (s) - passport;

- extract from the Unified State Register of Real Estate (Certificate of state registration of property rights (with a copy);

- a certificate from Sberbank confirming full payment of the debt;

- credit (mortgage) agreement;

- Sberbank mortgage with a note indicating full payment;

- receipt with a copy of payment of the state duty.

Is it possible to replace the collateral in a mortgage?

Also, the collateral has to be changed due to unfavorable circumstances. If you use another property as collateral, not an apartment purchased on credit, and you have lost ownership of such real estate, then the collateral, of course, will have to be changed. The same applies to the case when the mortgaged apartment was damaged or seriously lost in value.

The first such situation is the need to formalize ownership of housing purchased on credit. As long as it is collateral in the bank, you cannot be its full owner. And after changing the collateral, even not fully paid for housing can already become yours.

06 Jul 2020 stopurist 714

Share this post

- Related Posts

- Why they refuse a mortgage with maternity capital

- Are Chernobyl survivors provided with Land Plots Out of Queue for St.

- Pass your license without a driving school in 2020

- Sample appeal of a decision on an administrative offense

Buyer's risks when purchasing an apartment with encumbrances

The buyer and the bank are interested in a legally competent purchase of a mortgaged apartment. For this reason, the lender is involved at every stage of the transaction and controls the entire process. But still this does not relieve the buyer from possible risks:

- Other encumbrances may also be imposed on the apartment. This happens when there is a large debt to a bank or to government agencies (for example, the sale of an apartment purchased with a military mortgage has a number of features).

- A share of the property is allocated to children when purchasing an apartment using maternity capital. And if you do not control the process of alienation of children’s property rights, then in the future they will have the right to residential meters.

- The apartment has significant drawbacks. In general, the sale of real estate is always associated with some compelling reason (cockroaches, dysfunctional neighbors, thin walls).

- The money will be transferred, but the loan will not be repaid. It is impossible to remove the encumbrance from an unpaid apartment, even if the owner changes.

To reduce risks, you need to carefully approach such a transaction.