This article will discuss in detail the question of what a delay on a mortgage at Sberbank can lead to, as well as what to do if for some reason difficulties arise with making regular payments. In practice, the liability measures applied by the bank directly depend on the duration of the delay, the reasons for its occurrence, as well as on the interaction of the client with the bank.

What happens if you don't pay

The Sberbank loan agreement contains the debtor’s obligation to pay the mortgage debt to the lender on a monthly basis. Payment dates, monthly amounts with interest, and the remaining total debt are indicated in the payment schedule.

Payment must be made strictly on the specified dates. But in reality, a situation may arise when by the date specified in the payment schedule, the debtor does not have the money to repay the debt, resulting in arrears on the loan. And in this case, the creditor has the right to apply to him the measures of liability established in the agreement.

Consequences and amounts of fines for late mortgages depending on the duration

There is no clear answer to the question of how long a mortgage can be overdue, and it varies for everyone. In any case, penalties begin to be applied immediately on the first day of non-payment according to the schedule specified in the contracts, unless its terms provide otherwise. Sberbank sets penalties for late mortgages immediately upon concluding an agreement with borrowers. Carefully read all documents you sign at the bank before you receive money.

What should you do if your mortgage is in default? First of all, the consequences depend on the period of delay in payment. 1 day of late mortgage is not as critical as, for example, 3 months of non-repayment of the loan.

Debt 1 day

1 day of late mortgage seems to be an insignificant violation of the terms of the agreement with the bank, for which there will be no penalties, but this is not always the case. Delay on a Sberbank mortgage by 1 day already in most cases becomes the reason for the accrual of penalties.

There are also exceptions in such situations. If the day indicated in the repayment schedule falls on a Saturday, Sunday or holiday, the bank will postpone it to the next one. This must be stated in the agreement. Otherwise, the borrower may still be charged interest for late payment.

Penalties are calculated automatically by the banking system. Even if the client manages to explain his situation to the manager, he will not be able to influence the penalties applied. For this reason, it is important not only to make payments on time, but also to take into account possible delays in money transfers when making payments. If the loan amount is large, the penalty may be significant, even if the mortgage with Sberbank is only 1 day overdue.

See also: Will they give a mortgage if there have been delays on loans?

Debt 10 days

A delay in mortgage payment of 5 or more days already forces the bank to connect a collection service. The client will be called with a notification and asked to urgently close the debt. Before this, only SMS messages are received.

After 10 days of no repayments, the borrower’s issue will be dealt with by the security service. He may be invited to the bank to discuss the possibility of repaying the debt. If 1-2 days of delay do not affect your credit history, then a delay of more than 10 days will already be included in it.

Debt 30 days

Lack of payments for more than 1 month already makes the borrower unreliable. This is done by a special department of the bank.

Important : if you are in arrears on your mortgage and you don’t know what to do, check your loan agreement first. Is there a condition there that the bank has the right to charge an additional fine, which is 0.5% of the outstanding amount of debt for violating your obligations? A month after the missed payment date, you may be charged such a fine if you do not contact Sberbank.

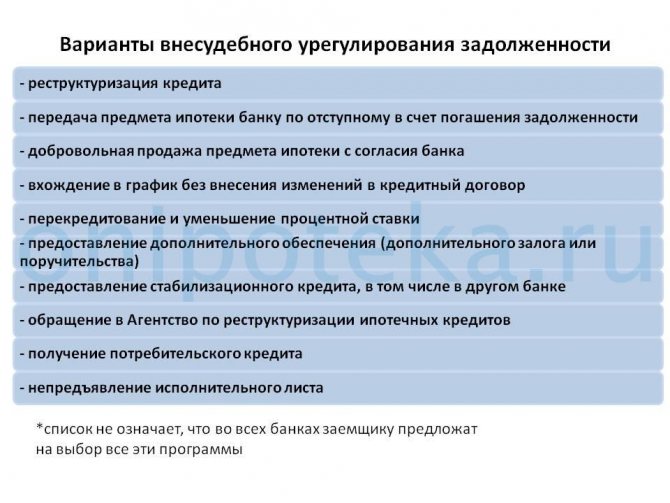

It is very important to respond to bank requests and not try to hide or ignore calls from the collection service or internal security service. No matter how late the mortgage is, the consequences can be worse if you refuse to solve the problem together with the bank. If you explain the situation and provide all the documents confirming valid reasons for the lack of repayment, you may be offered debt restructuring (change in the amount, payment terms).

Debt 90 days

After 3 months of delay, the bank changes tactics and can already sue to seize the collateral. In this case, it is very easy to lose your apartment with a mortgage. In addition, Sberbank will also add compensation for expenses to the statement of claim.

Being 90 days or more late on a mortgage payment already has serious consequences. If the bank nevertheless goes to court, there are two options for the development of events:

- Conclusion of a settlement agreement (which is most preferable for both parties);

- The property will be arrested and seized, while the accrued fines will not go away, and penalties and legal costs incurred by the bank will be added to them.

See also: Declaration of bankruptcy - how to achieve official debt write-off?

It is precisely because of the possible second outcome that a settlement agreement is the best option for both the client and the bank. So, if you are in arrears on your mortgage, which can be long-term, the first thing you need to do is negotiate with the bank and consider ways of repayment. A lawyer can help in this matter, who will ensure that the terms of the agreement are met on the part of the creditor. Also, a lawyer can challenge part of the penalties, thereby reducing the total amount of debt.

90 days is how long a mortgage can be overdue before serious consequences occur, not counting a damaged credit history and accrued penalties. The mortgage loan will have to be repaid one way or another.

One day late

Many debtors believe that a delay of just one day will not entail any consequences, and the bank will simply turn a blind eye to it. But this is a wrong belief. The fact is that the penalty is calculated not by bank employees, but by an automatic system that calculates and issues the penalty starting from the next day of the appointed payment date.

The exception is when the payment date falls on a weekend. In such a situation, you can pay the debt amount on the first business day following the payment date.

The debtor usually learns that a penalty is being charged on the debt from SMS messages, also sent automatically.

It might be interesting!

What is the mortgage payment schedule and can it be changed?

Can mortgage arrears lead to property loss?

As an extreme and most unpleasant measure, banks may resort to foreclosure of mortgaged property. This is unprofitable for Sberbank itself. They are more interested in the payment of debt and interest by the borrower, while the seizure of property entails legal proceedings, and in the future - putting up housing for auction. How long can a mortgage be in arrears before there is a risk of losing your apartment?

See also: Anti-collector - professional help for those who have fallen into a debt trap

You can lose your collateral housing if:

- Mortgage debt from Sberbank is not repaid for more than 2 months;

- The bank receives information that the borrower’s financial situation has deteriorated significantly;

- Late payments account for more than 5% of the outstanding debt.

The bank can initiate the procedure for depriving a client of collateral property only if it is sure that the debt will not be repaid.

Overdue from 7 days

Approximately a week after the date of fulfillment of the payment obligation, the creditor’s employees may begin to call the debtor with a demand to repay the resulting debt.

After 10 days, employees of the security department begin communicating with the debtor, who invite him to come to the bank branch to discuss the reason for the debt and find a way out of the current situation. But the main negative consequence of violating the obligation to make a payment for a period of more than 10 days is the bank reporting information about the debtor to the credit history bureau. This means that even such a small delay can ruin the defaulter’s credit history for a long time.

What will be the consequences

Each bank adheres to established measures and procedures in relation to debtors in accordance with its policies. Dealing with overdue and problem debts is the responsibility of employees of the credit, legal departments and security services.

Standard procedures when a borrower is in arrears are as follows:

- Notifying the debtor about the delay by means of a call to a mobile phone, SMS or email newsletter.

- Accrual of penalties or fines from the day following the date of the current payment. The amount of such sanctions is clearly stated in the loan agreement.

- A personal conversation with the debtor from security officers with explanations about the possible consequences of non-repayment of the debt (if the client is ready for dialogue).

- Filing a statement of claim demanding the collection of debt to the bank.

- Foreclosing on the collateral.

The last two procedures are extreme measures that lenders resort to in relation to unreliable clients with long delays and evasion of contacts.

The consequences of failure to timely fulfill your obligations to the bank may include:

- serious deterioration in the quality of credit history (up to and including blacklisting);

- excess expenses (together with the monthly payment, the client will need to pay the amount of accrued penalties);

- loss of mortgaged housing (in the event of a corresponding court decision, the bank will sell the borrower’s property and pay off the mortgage loan debt from the proceeds).

Since the mortgaged property is sold at auction, prices for it may be significantly lower than market prices. For any borrower, such a procedure will be extremely unprofitable. Therefore, it is better not to lead to such events in any way.

What to do if a creditor goes to court?

If the creditor goes to court, the debtor should take all measures necessary to minimize the negative consequences.

Such measures include:

- An attempt to resolve the issue out of court;

- Preparation of a response to the statement of claim containing a detailed description of the valid reasons for the delay, as well as the impossibility of resolving the issue with the bank;

- Taking part in a court hearing;

- Application for a settlement agreement.

At this stage, the debtor's attempts to hide from the bank or court may lead to the seizure of the mortgaged apartment, its seizure from the debtor, and further sale at auction.

It might be interesting!

How is the legal regulation of mortgages, judicial practice

Help from the bank

The bank will offer the client its terms for solving the problem, but these conditions, to put it mildly, will not satisfy everyone. Among such proposals are the following:

- Reducing the monthly payment with a one-time increase in the mortgage term (loan restructuring). Such conditions are most likely suitable for young borrowers who are still far from retirement; the bank will most likely refuse older clients.

- Take a break. This provides for stopping loan payments for a certain period. It seems like a good option, but there are some pitfalls here too. In some banks, even if payments are suspended, interest will be charged on the principal debt, which will ultimately increase the payment amount itself. Of course, this is not beneficial for everyone.

If all of the above proposals from the bank did not satisfy you or did not help at all, perhaps the only possible way out of the current situation remains, this is the sale of the mortgaged apartment. It is worth noting that credit apartments are bought very reluctantly, so in most cases it is possible to sell it only by reducing the cost, that is, less than the market price. Here you should also understand that by selling the apartment you will be able to pay off the entire debt to the bank, otherwise there will be no point in this operation.

A mortgage is a big responsibility that falls on the shoulders of the borrower, so before taking such a step, it is better to think again and understand how the debt will be repaid, so as not to get into difficult situations in the future and end up with nothing.

The bank does not want to restructure the debt

If things are really bad for you and you don’t see any way out, you can start personal bankruptcy proceedings. This law came into force on July 1, 2020), the court may oblige the bank to restructure your debt. To do this, he must be sure that after restructuring the bank will receive significantly more than if it immediately sold your home. Read more about the bankruptcy procedure in our article “What is bankruptcy. Bankruptcy procedure for individuals and legal entities”

The bank sells the apartment for debts

If your mortgage debt exceeds 500 thousand rubles (this means overdue debt on all debts (loans) that you have), you are required to apply to the court for personal bankruptcy. If the court understands that you cannot pay even under the simplified scheme, your property will be sold for debts - including your apartment. You can act differently: try to sell the apartment yourself. To do this, you need to obtain the bank's consent. Pay off the mortgage debt with the proceeds from the sale.

This is my only home

An apartment purchased with a mortgage can be taken away for debts, even if it is the only home. This provision is clearly stated in the Civil Code, and in the law on mortgages, and in the amendments adopted with the law on personal bankruptcy.

What to do if you have nothing to pay your mortgage at Sberbank

If such a life situation has arisen, as a result of which there is no money to pay the mortgage, it is recommended to take one of the following measures:

- Restructuring. The best way out of a difficult financial problem may be to change the terms of debt servicing. The bank may provide the debtor with one of the following restructuring options: Credit holidays - providing a period during which the debtor has the right not to make payments on the loan;

- Installment payment – reducing the amount of monthly payments by increasing the term of the contract.

- You can also ask the bank for a Temporary suspension or cancellation of penalties;

- Changes in mortgage interest rates;

- Changing the loan currency.

- Reducing the interest rate;

It is important to know! Before selling an apartment, you must obtain permission from the bank.

What should you do first?

If the client does not transfer the mortgage payment on time, he will have to pay a penalty in the amount of 0.1% per day of delay. Citizens who do not repay the debt within 30 days will pay a fine at an increased interest rate (2-3% per day of the loan amount). Do not forget about timely payment of the insurance premium. If the borrower does not renew the insurance policy, the mortgage rate may increase significantly. A borrower who avoids communicating with a loan officer will have to talk to debt collectors. Collection department employees will call not only the debtor, but also co-borrowers. Some will have to communicate with debt collectors in person.

A prolonged absence of payments (90 days) will lead to the bank filing a claim in court. The collateral property will be seized. After this, the apartment will be transferred to the bank’s balance sheet and will be sold during special auctions. Some bank clients refuse to voluntarily leave the seized premises. In this case, they will be forcibly evicted from their housing. An attempt to counteract the bailiffs may result in the calling of a special forces unit that will use special equipment and weapons.

You should not avoid contact with bank employees. It is better to visit the bank office and honestly talk about your problems. Bankers are interested in a person repaying his debt in full. They will definitely accommodate the borrower and offer a debt restructuring program.

The credit committee may extend the loan term and temporarily reduce the monthly payment. The borrower can also become a participant in the “mortgage holiday” and receive a deferment to replenish the mortgage account. During this time, a person can find a new job and additional sources of income. Many banks have loan refinancing programs that reduce the cost of borrowing. A borrower wishing to use this service must provide the following documents to the bank:

- A completed application form;

- Original passport;

- Certificate of income in the form of a bank or 2-NDFL;

- Tax return in form 3-NDFL (for persons with additional sources of income);

- Extract from the Unified State Register;

- Certificate of unemployment benefit amount (issued by the employment service);

- Certificate of absence of debt to utility companies;

- Salary card account statement;

- A copy of the insurance contract and a receipt confirming payment of the insurance premium;

- Papers confirming disability or loss of ability to work.

Refinancing is carried out on the basis of an application in the established form. To re-register a mortgage, the consent of Sberbank is required. If the borrower is unable to repay the mortgage in the medium term, then he should sell the mortgaged apartment or house (with the consent of the bank).

How can you defer interest payments?

In order to defer interest and defer payments of the principal debt, you must apply to the bank. Along with the application, the bank employee must provide documents confirming the deterioration in the debtor's solvency.

Such documents include:

- Certificate confirming the salary reduction;

- Work record book with a record of dismissal from the last place of work;

- Child's birth certificate;

- Certificate of divorce, etc.

As a rule, banks in such situations meet their clients halfway and sign an additional agreement with them in order to get out of a difficult situation.

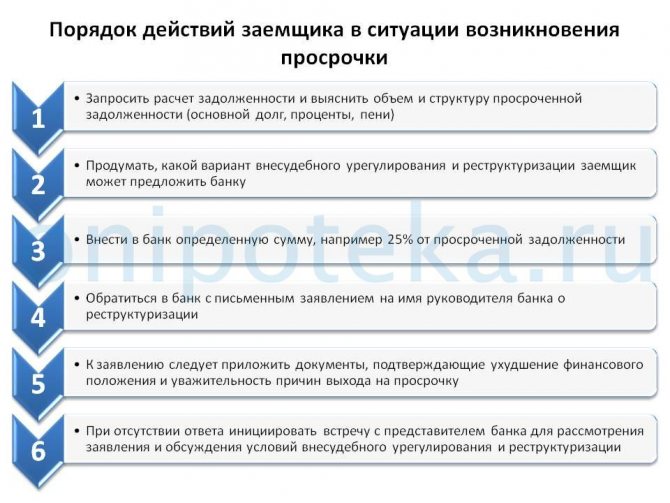

If difficulties arise with payment, you should never hide from the bank. In this situation, you should perceive him not as an enemy, but as an ally. And the most correct action of the debtor will be to appear at the bank and report the difficulties that have arisen. Only in this case will it be possible to jointly find a way out of the current situation and make it painless for both parties.

What to do?

What to do if you are in arrears on your mortgage with Sberbank? First of all, you need to contact the collection service or security service. In addition, it is important to explain in a timely manner the reasons for the lack of repayments. Of course, you won’t need to do this if you delayed payment by only 1 day or even a week. However, if the deadline is approaching a month, and you still have not solved your financial problems, this is a reason for active action.

Timely seeking legal assistance will allow you to:

- Find ways out of a difficult situation;

- Challenge illegally accrued fines and penalties;

- Agree with the bank faster;

- Reduce the debt if there are violations of the contract on behalf of the creditor;

- Restructure debt.

The specialist will communicate with the collection service and achieve the best solutions for the borrower. If your financial situation is completely hopeless, you are in arrears on your mortgage with Sberbank or another organization, and you don’t know what to do, your lawyer may recommend going through bankruptcy proceedings and writing off your debts.

How to calculate 90 days overdue

To determine from what day the counting is carried out, you need to study. If the borrower is 90 days late on the mortgage, there are two options:

- Missing one payment for up to three months from the date of its payment according to the schedule.

- Or several facts of payment in violation of deadlines, the amount of which reached 90 days within six months.

The method of calculation is determined based on the situation. But any missed payments are counted for the last 180 days. Another question arises: how to count 90 days of arrears on a mortgage if the borrower has several contracts. In this case, the facts of non-payment are summarized for each of them for six months. If there is only one agreement with the bank, the period of violation of deadlines is determined based on its provisions and schedule.

What to do if the loan payment terms are missed

Non-payment and violation of the schedule can lead to serious troubles if left unchecked. When you have to fall behind on your mortgage payment, do not wait for a call from the bank, contact the lender yourself and explain the reason. What you shouldn't do is hide and turn off your phones. There are several possible solutions:

- credit holidays;

- restructuring;

- home sales;

- contacting the insurer.

Important to know: What to do if you don’t have money to pay your mortgage

You can only understand what to do if your mortgage is overdue based on the situation. If financial difficulties are caused by job loss or illness, take advantage of credit holidays (the right is specified in). You will be given several months to improve your financial situation by returning to the payment schedule. The overall term of the contract will extend for this period, but you will avoid litigation and seizure of the property.

Recommended article: What to do if your apartment rent increases

If your mortgage is one day overdue, there is no need to worry. When it comes to 30 days or more, you should try restructuring:

- contact the bank with an application;

- discuss a new schedule;

- sign an additional agreement.

The loan term will increase, but the payment amount will decrease.

The sale of living space is permitted only with the consent of the mortgagee. It is necessary to resort to such a measure as a last resort, when the bank has already taken the apartment when the mortgage is overdue. It is better to use insurance if the situation that led to a violation of the schedule is covered by the policy. Otherwise, the creditor will definitely file a claim with the courts.

What to expect from the bank when you miss a payment

There are standard procedures carried out in case of violation of loan payment deadlines. Much of the implementation of such measures depends on the period of non-payment. Let's take a point-by-point look at what the bank does when a mortgage is overdue.

- At the first stage, the debtor is notified of the violation. This could be a call or an email.

- Penalties and penalties are assessed. Typically, such a measure is effective from the day following the delay.

- The case is then transferred to the security department. The debtor is scheduled for a personal meeting where possible solutions to the problem are discussed.

- Mortgage arrears affect your credit history. Information about the violation is sent to the BKI within five days.

- If none of the actions bring results, the bank files a lawsuit (). As a result, the housing is sold at auction, and the funds are used to pay off the debt.

Recommended article: Mortgage without a credit history - chances of getting approval

Extreme measures are used in case of really serious violations of deadlines, and if the borrower does not make contact. Most often, the bank offers restructuring or refinancing to ease the client's financial burden. Understanding the dangers of mortgage arrears, you should be careful about fulfilling your obligations under the contract. If this occurs, it is better to contact the lender yourself.

How will missing a payment affect your credit history (30, 60 and 90 days)

According to federal law (), any bank issuing loans is required to cooperate with BKI and transmit here information about the borrower’s violations. The deadline for sending information is clearly limited: no more than five days from the moment the mortgage payment was late. Even if the delay does not exceed one day, within the next five working days the bank is obliged to send information about this to the BKI.

There are two options for missing deadlines: active and historical.

- in the first case, we are talking about outstanding arrears that are still valid.

- secondly, about non-payments that occurred earlier.

If there is a slight delay in the bank's mortgage (up to 30 days), this will not greatly affect the approval of loans in the future. The most dangerous are absences of 90 days or more. If there are any, loan applications will be denied for several years. But you still need to learn to determine when deadlines are missed.

Recommended article: Refusal of mortgage holidays - reasons and grounds for refusal, where to complain

In any case, it is better to check your credit history.

Why was there a delay on a military mortgage?

The peculiarity of this type of lending is that funds for the purchase of real estate are allocated from the federal budget, and payments are made by Rosvoenipoteka (). Despite government guarantees, military personnel also encounter problems with non-payment of loan payments. There are arrears on a military mortgage in two cases:

- Lack of indexation of savings according to the NIS.

- Dismissal from the borrower's service.

If savings are not indexed, after updating the payment schedule, a debt may arise. As a rule, a serviceman learns about it after dismissal or the end of the loan term. Usually there is no indexation when there is a crisis in the country, like the one that happened in 2014-16. Currently, measures have been taken to prevent such situations.

The second case of why there was a delay on a military mortgage is associated with the borrower’s early dismissal from service. As a result, the loan agreement is violated, and the former serviceman is obliged to return to Rosvoenipoteka what has already been paid (), continuing to pay the loan. However, here you need to take into account the total duration of service and other nuances. But if the mortgage is overdue, the consequences will be negative in both cases. In such a situation, it is important to understand what the borrower should do.