What is a mortgage and what are its different types?

In simple terms, a mortgage is a transaction between an individual (or individual entrepreneur) and a bank when a mortgage collateral agreement is signed. According to it, you receive money in the required amount and undertake to pay the bank monthly the amount specified in the agreement. In this case, the real estate that is pledged under the agreement falls under the mortgage.

You can pledge:

- House;

- dacha;

- plot of land;

- apartment;

- other real estate objects.

If the borrower ceases to comply with the agreement, then the credit institution becomes the owner of the property pledged as collateral. Real estate can be sold so that the financial institution does not suffer losses. These are the fundamental conditions of the mortgage market in Russia. The main document that financial institutions follow when drawing up a mortgage agreement is the Federal Law “On Mortgages (Pledge of Real Estate)”, adopted in 1998.

Main parameters of a mortgage loan:

- issued for a long term (5–50 years);

- has a clear purpose;

- low interest rates;

- strict compliance with the law “On Mortgages” during registration.

The real estate that is provided as collateral belongs to the borrower, but until the loan is fully repaid, he does not have any rights to dispose of this property. If problems arise with repaying the debt, the credit institution has the right to choose how to use this property at its discretion.

There is competition between financial institutions. To attract clients, credit institutions develop and implement various mortgage programs, the names of which reflect the purpose or method of obtaining a mortgage loan.

In everyday life, a mortgage is usually used to refer to money that the bank gives as collateral, and then it must be returned, otherwise you will be deprived of the mortgaged property.

You can choose a mortgage:

- For the purchase of housing on the secondary market. Main advantages: optimal interest rates, fast processing, flexible contract terms. Distinctive feature: mandatory title insurance is required.

- For real estate that is under construction. If the developer is approved by the bank, then housing can be purchased at the construction stage. The amount under the contract will be less, since it is valued lower, but the interest rates on the loan will be the highest.

- To purchase a plot of land. In this situation, the bank takes real estate as collateral, which will be equivalent to the acquired land. And the borrower begins new construction on the site. Until the debt is repaid, the bank will have as collateral everything that the borrower built on the acquired land.

Who gets a mortgage?

A mortgage is a loan for a long period and for a large amount. Banks analyze each future contract separately, and in case of high risks, refuse to issue.

Pensioners, people without permanent employment, disabled citizens, workers with low incomes and who do not have ownership rights to any expensive property have a low chance of getting a mortgage.

Such borrowers have a high risk of having their mortgage application rejected, especially if they have a bad credit history.

An increase in the likelihood of approval of an application should be expected if the borrower has guarantors or the ability to secure expensive property as collateral. In such circumstances, you can hope to obtain a mortgage loan, but the procedure will become a little more complicated.

Socially vulnerable groups of the population have the right to obtain loans under special programs with preferential terms.

These groups include:

| Young families | mortgages are provided for young families with minor children |

| Military personnel | the loan is provided to military personnel who have served for more than 3 years |

| Young teachers and lecturers | special program for employees in educational institutions |

| Persons entitled to maternity capital | Contribution of maternity capital as an initial payment |

| Loan for public sector employees | Regarding doctors, teachers, etc. |

Which bank to choose for a mortgage in 2020: top 5 most profitable

The financial services market is diverse, so you should know how to choose a bank for a mortgage and what to look for. It’s easy to get confused among such an abundance of offers from all kinds of credit institutions. Each tries to advertise its services from the most advantageous angle. To choose the right bank for a mortgage in 2020, you can use information about the top 5 best financial institutions for a mortgage loan. Experts analyzed various data and compiled a rating of banks.

- Bank opening"

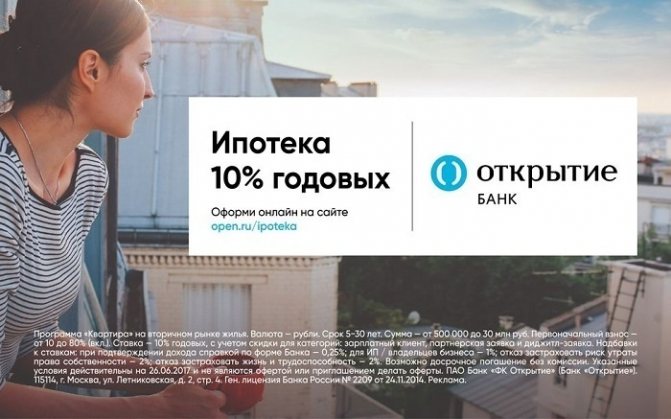

This financial institution is worth taking a look at the programs it has developed for its clients. Very favorable conditions were provided for the mortgage. The client can choose one of several programs depending on his capabilities and needs.

If you decide to choose Otkritie Bank, then pay attention to what types of mortgage programs it offers:- Buying an apartment in a new building.

Buying an apartment on the secondary market.

- Refinancing mortgage loans from other banks.

- Military mortgage.

- Real estate for maternity capital.

- Mortgage lending for the purchase of large apartments.

- Tinkoff Bank

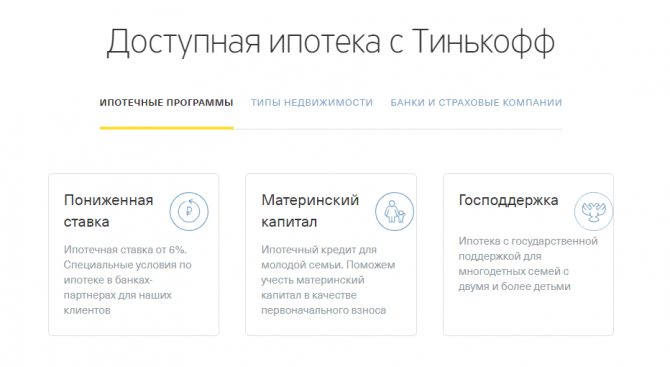

Tinkoff Bank offers you the opportunity to consider the proposals of several credit institutions by submitting just one application. At the same time, you do not need to go to various banks yourself and waste time studying lending conditions. You just need to leave an online application on the Tinkoff Bank website, and your personal manager will do the rest for you.

The applicant's application form will be reviewed by partner banks. Once the application is approved, all you have to do is choose a financial institution based on the most favorable conditions. There is a nice bonus: when applying for a mortgage at Tinkoff Bank, you receive a discount on the interest rate of up to 1.5%. If you take into account the loan amount, such a discount will help you save significantly.At the moment, the minimum mortgage rate for the purchase of housing in a new building is set at 6% per annum. The maximum term of the loan agreement is 25 years, and the amount can reach 100 million rubles. Not only individuals, but also individual entrepreneurs can submit an online application.

- BJF

The Housing Finance Bank is also attractive for its mortgage lending program. Even borrowers with a bad credit history in the past have a chance to become a client of this bank. Choosing BJF will be the right decision. The main requirement is that at the time of submitting the application there should be no overdue payments on loans from other banks. This credit institution is one of the few where they will not refuse a loan due to incomplete trustworthiness of the client. According to BWF statistics, 82% of applications are approved by representatives of the financial institution.

If you have chosen the “Housing Finance Bank”, then the main conditions for providing mortgage lending will be the following:- To draw up a mortgage agreement, you only need 2 documents (passport and a second document - SNILS, Taxpayer Identification Number, driver's license).

There is a program that allows you to get a loan without certificates on the day of application.

- If you confirm your official income, you can lower the interest rate and increase the loan limit.

- The process of registering the transaction and ownership of the apartment takes place within 3 days.

- A mortgage loan is issued directly from the bank, without the participation of agents, intermediaries and commissions.

- Residents of the following cities can submit an online application for a mortgage: Moscow and the Moscow region, St. Petersburg and the Leningrad region, Volgograd, Yekaterinburg, Kazan, Krasnodar, Krasnoyarsk, Nizhny Novgorod, Saratov, Novorossiysk, Novosibirsk, Omsk.

- VTB Bank

VTB does not lag behind in the rating of banks and offers to choose one of the profitable mortgage programs:

- The minimum interest rate starts at 10.2%.

Low initial contribution – 10%.

- You can draw up an agreement on the terms of crediting maternity capital against the advance payment.

- Sberbank

Sberbank is the largest bank in the country. He is also active in mortgage lending. The bank acts as a lender for both borrowers and developers. Interestingly, the financial institution easily lends even to people of retirement age. There is a condition: repayment of the debt must occur before the borrower turns 75 years old.

Depending on the chosen program, the interest rate on the loan will differ. The minimum is 8.9%. But this rate is only available when purchasing an apartment in a new building or when taking out a military mortgage. It is very convenient that the down payment is only 10% of the value of the purchased property. The loan term does not exceed 30 years. A mortgage can be applied for online.

Using the services of VTB, you can choose the “Mortgage Loan with State Support” program. Families who had a second or third child after January 1, 2020 are eligible for preferential lending: with a down payment of 20% or more, the loan rate is set at 6% for some time.

The financial institution offers to choose a profitable program when purchasing an apartment of 65 square meters or more. “More meters - lower rate” - the name speaks for itself.

What determines the bet size?

A mortgage is a long-term debt obligation. In addition to the principal amount of debt, the payer undertakes to repay accrued interest determined by the rate established by the bank. The minimum mortgage rate will help significantly reduce the amount of the final payments for the recipient.

In practice, the percentage is calculated based on a number of parameters. The most important of them are the following:

- The credit history of the borrower - the absence of outstanding debts or their presence will largely affect not only the amount of interest accrued, but also, in general, approval for issuing a loan;

- Volume of the down payment – the larger this amount, the lower the interest rate;

- The period for which the amount of money is issued - the sooner the borrower undertakes to pay, the lower the rate.

The lowest mortgage percentage in modern conditions fluctuates at 4.5-5% per annum under the “Mortgage for families with children with state support” program. The upper limit can reach 15% or more. The exact calculation is made in each specific case, based on the applicant’s data.

Tips on how to choose a bank for a mortgage

You have decided that the best opportunity to purchase your own home is a mortgage. Which bank is better to choose is a difficult question. It is worth studying all the nuances in depth. This approach will help you choose the right financial institution.

- Wishes and possibilities. First of all, you should understand that the same lender will have different conditions for purchasing a secondary home, an apartment in a new building, or a private house. Restrictions can be various technical criteria: year of construction, number of storeys of the house, material of walls and ceilings, and much more. The conditions for issuing a loan will even be influenced by where the house is located - in Moscow or the regions.

The second step is to study information about the size of the down payment, since the loan amount will depend on this. You need to understand that when buying a home with a mortgage, there are many other mandatory expenses. This means that you cannot fully count on the fact that you will spend all the money that is available only on the down payment.The third stage involves a realistic assessment of your financial capabilities. You need to realize how much you will need to pay to the bank every month for several decades. If the size of this payment every month forces you to be on the brink of survival, then you should think again about whether you need to burden yourself with a mortgage loan.

At the fourth stage, you can think about your attractiveness to the bank. The higher the official income, the longer the work experience and the more attractive the credit history, the lower the interest rate the bank offers to the borrower. Age also matters. Typically, the bank indicates in the conditions for issuing a loan the maximum age of the borrower at the time of repayment of the debt under the agreement, and not at the date of its conclusion. Therefore, age may become a barrier to obtaining a mortgage loan.

The final stage is to select the financial institution that will provide the most favorable conditions.

- Stability and reputation. At this stage, you should seriously think about how to choose a bank for a mortgage. A loan is taken out for a long time, which means you need to choose a bank with a good reputation and extensive experience in the financial market. Loan rates from such financial institutions most likely will not be the lowest, but the borrower is unlikely to have to face unpleasant situations while obtaining and servicing the loan. In the financial world there is no 100% guarantee that the bank will not go bankrupt in the future, but with large credit institutions this risk is less.

It is worth considering choosing small lending institutions that specialize in issuing mortgage loans. Most often, they can offer several programs, among which you can choose the one with the most favorable conditions. Such banks usually review the application, approve and issue a loan in a fairly short time.

The following nuances also help you make a choice in the direction of a specific financial institution: the credit institution’s specialists have developed a large number of mortgage programs and established business relationships with developers and realtors. There are banks that even have their own databases of housing for sale. This demonstrates the long-term purpose for the existence of a financial institution.

Customer reviews can help you decide which bank to choose for a mortgage. You can find quite a lot of them on the Internet in a short time. But you should understand that both good and bad reviews can be false. Positive comments may well be left for a reward. A bad review can be written by competitors or an offended client if he did not fulfill the terms of the contract and sanctions were imposed against him. To choose a financial institution, it is better to collect reviews from real clients who have accurately taken out a mortgage loan and can tell in detail about all the nuances of the transaction.

- The real cost of the loan. Of course, advertising is replete with the most favorable conditions. A potential borrower, when he wants to quickly choose a credit institution, may simply not notice or not pay attention to the preposition “from” next to the interest rate. Thus, the minimum percentage is easily tempting, but in reality the figure will be different. Before choosing a bank for a mortgage, your task is to find out the real cost of the loan.

And it depends on various factors:

- the size of the interest rate on the loan;

availability of the main and amount of additional commissions;

- the amount of insurance payments;

- schemes for calculating the repayment schedule.

Typically, a bank can provide the lowest interest rate on a loan to its existing client, especially if there were no questions about the credit history. Therefore, to begin with, you can choose a financial institution where you have already been served before or of which you are currently a client. Perhaps this is where the most favorable conditions will be.

Most often, the credit institution does not give the client the opportunity to choose a loan repayment schedule. There is an annuity schedule - this is when the borrower pays the same amount every month, regardless of the debt balance; differentiated repayment method - when the bank client pays the principal amount monthly in equal installments. Interest is calculated on the outstanding balance. It is better for the client to choose the second option. It is very profitable, since the monthly payment amount decreases as the loan is repaid.

But the bank benefits from the annuity schedule option, so most often it is used by default. If the borrower cannot afford such a schedule, it is necessary to clarify the possibility of using a differentiated loan repayment scheme.

In accordance with current legislation, when concluding a mortgage agreement, exclusive real estate insurance must be taken out. Often financial institutions require life and health insurance, as well as title insurance. The borrower can refuse optional types of insurance, but in this case the bank increases the interest rate on the loan.

It is worth taking into account all such additional payments when choosing a credit institution, since all these nuances make the loan more expensive. Often the client cannot choose the insurance company himself. It is mainly imposed by banks. For the borrower, the conditions of such insurers are usually extremely unfavorable.

To attract new customers, banks periodically hold promotions. The conditions can be quite attractive, but it is worth analyzing all the terms of the contract, since there are probably pitfalls that may run counter to the borrower’s capabilities. For example, a high commission amount or a ban on early repayment.

If you plan to buy an apartment in a new building, even if it is still at the commissioning stage, then you can find out the opinion of the developer: construction companies often use loans themselves, so the lender, after putting the house into operation, can offer potential borrowers a mortgage loan on favorable terms so that they can buy the apartment you like.

The clause on the amount of penalties for failure to comply with the terms of the mortgage agreement is very important. It is clear that conscientious borrowers plan to repay the debt exactly on time every month, but in life there are different situations. Even a few days of late payment can result in large expenses. It is worth familiarizing yourself with the procedure of a financial institution in case of non-payment of a loan. It is better to choose an institution that provides the opportunity to restructure debt, in particular providing credit holidays.

Before you finally select a financial institution, it would be a good idea to get a preliminary calculation of the payment schedule and additional costs in writing in advance. It is useful to study the loan agreement. For individual or unclear points, you can consult a lawyer.

5 more recommendations on how to choose a bank for a mortgage

- Pay attention to the “salary” bank. You can count on more favorable terms from the bank if the borrower is a participant in the salary project in this particular institution. In this case, the application will be reviewed much faster, fewer documents will need to be provided, and there is also a chance for preferential loan rates. In addition, you can count on reducing factors for mortgage rates under standard programs. Typically this is from 0.25 to 0.5%.

- Don't ignore commercial banks. You should not agree to less favorable conditions just because you have known this credit institution for a long time. You can choose a suitable organization among many commercial banks that offer truly favorable conditions. Often there are quite flexible conditions that are beneficial to both parties. Raiffeisenbank provides one of the lowest rates under programs with state support: with a down payment of 50% or more, the loan rate is 11%, in other cases 11.5%. But Metallinvestbank offers 13.5% with a down payment of 10% under a standard lending program.

- Special programs for individual entrepreneurs.

If an individual entrepreneur or the owner of his own business wants to get a mortgage, then the bank you should choose is the one that issues loans under programs with simplified consideration of borrowers. It is much faster and requires less paperwork than standard programs. Some financial institutions do not accept applications from entrepreneurs using a single tax on imputed income. In this situation, it is much more difficult to trace the real income of a potential borrower.

What does it mean: profitable mortgage? How to get a mortgage profitably?

Each borrower has his own opinion regarding the profitability of a mortgage . Therefore, this concept is relative.

Some people believe that a profitable mortgage is a loan with a minimum interest rate. Others think it is an opportunity to take the maximum amount possible. Some people find it beneficial to get a mortgage without a down payment.

Therefore, there is no specific definition of what a profitable mortgage is . When choosing a suitable lending program, you need to pay attention to conditions such as: interest rate, down payment, insurance payments (and their number), etc.