Repayment of a mortgage with maternal capital at Sberbank and other large credit institutions became possible thanks to the development and implementation of a social project, within the framework of which Russian families today can receive support from the state. Using certificate funds to purchase real estate requires going through a certain procedure, and knowledge of the nuances will simplify the process of building relationships with the bank.

How to pay for a mortgage with maternity capital?

The concept of “maternity capital” was first introduced into use in 2007, representing a measure of state support for Russians. Certificate holders receive the right to spend funds for purposes that are directly defined by law.

Families have the right to count on the subsidy after the birth of a second child or the fact of his adoption, and the social program has been extended until 2021. Currently, parents have the right to count on financial support in the amount of 453,026 rubles.

One of the possible ways to spend family certificate funds is mortgage lending, and using this option allows borrowers to reduce their loan burden.

According to the current rules, maternity capital can be used to repay:

- previously issued mortgage;

- newly taken out housing loan;

- repayment of the down payment.

The advantage of using a certificate to pay off a mortgage is that there is no need to wait three years. Using maternity capital funds, you can repay the advance, accrued interest or principal debt on the loan. It is prohibited to use the balance to calculate fines and penalties associated with late repayment of the loan.

The procedure for using maternity capital funds is strictly regulated, and in order to be able to use the balance, the certificate holder is required to obtain permission from the regulatory authority. Today, the PF acts in this capacity, and approval is possible if a complete package of documents is provided and there are no complaints from the organization’s specialists.

How to pay off your mortgage?

At Sberbank, a mortgage using maternity capital funds is quite possible, so the client can use it for a down payment and for early repayment of the principal debt.

However, it is premature, before paying for the mortgage with capital, it is necessary to obtain permission to dispose of these funds from the Pension Fund.

Pension Fund employees base their decision on the possibility of using public funds for the purchase of housing under Federal Law No. 256 of December 29, 2006.

This is where it is written about the procedure for using mat. capital, possible reasons for refusals, the required package of documents and the mechanism for transferring money to the bank.

Depending on whether you use maternity capital as a down payment or to pay off a mortgage loan, the package of documents will change.

Read more about repaying your mortgage with maternity capital here.

Loan programs at Sberbank

There are four main programs for taking out a mortgage using maternity capital:

- Acquisition of land allocated for the construction of individual buildings. According to this program, the client can purchase a plot of land that is allocated by the municipality specifically for private development.

Here the bank's risks are quite high, so the lending conditions are not the most attractive. However, compared with other banks, this program is one of the best. - Purchasing housing on the secondary real estate market. This can be either an apartment or an individual house.

The conditions at Sberbank for this program are attractive, but the package of documents is quite large. It's worth collecting it to save on loan collateral.In other banks, similar programs are 2-3% more expensive

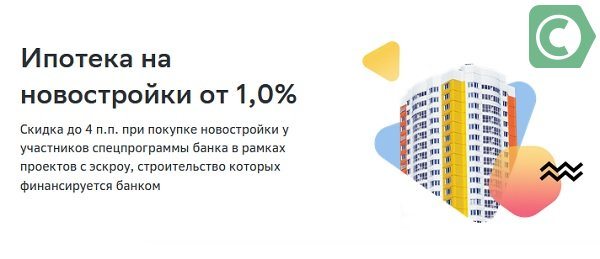

- Purchasing an apartment in a building under construction. If you take out a mortgage on a house that is under construction, you can get a preferential interest rate.

The lending conditions are the same as for purchasing real estate on the secondary market. - Purchasing housing in a new building. Here you can also get a preferential interest rate if you buy an object in a house that was built with money from Sberbank.

Moreover, Sberbank takes into account maternal capital for mortgages, and also works with a number of other government subsidies.

Therefore, if you are eligible for a subsidy from the state, this money can be used to pay off debt or as a down payment on a Sberbank mortgage.

One of the most popular programs is the “Young Family” program, which provides a minimum interest rate. To use it, you need to contact the administration of your district in which you are registered. You will need a housing department. Since reception is not held every day, it is better to call there in advance.

Read about how to buy an apartment with maternity capital and a mortgage here.

Interest rate

The interest rate for all types of loans is approximately the same. If you get a mortgage from Sberbank and use maternity capital, you can use the “Young Family” program - only 11.5% per annum.

The maximum rate is 14% per annum, it is provided for the acquisition of land for construction.

It is worth noting that the rate also “floats”, depending on the size of the down payment: the larger it is, the cheaper the loan will be. It is also affected by overall length of service, income level, number of guarantors, availability of insurance and much more.

Without insurance, the loan becomes more expensive by 1%. The duration of the loan agreement also affects the cost of the loan. The larger it is, the higher the bank’s risks and the more expensive the loan security.

Salary card holders and employees have their rates reduced by 1-2%. Thus, it is difficult to say in advance what your rate will be. You can calculate your mortgage at Sberbank individually.

How to get a loan: procedure

At the first stage, you need to choose a credit institution for future cooperation, decide on the basic parameters of the loan and the type of housing to be purchased. A guideline can be the offers of the largest Russian banks, in the range of which you can find options for purchasing real estate in the primary and secondary markets.

Sequence of actions if you want to use maternity capital funds to pay off your mortgage:

- preparation of documents for PF;

- applying for a permit;

- obtaining bank approval;

- selection of real estate;

- concluding a credit transaction;

- registration of ownership.

The list of documents to be submitted to the Pension Fund is standard, but may differ slightly from the circumstances of the disposal of maternity capital. If the application is submitted by a representative, then a power of attorney is additionally required. The decision is made by PF specialists on whether such a procedure is legal.

What documents are required

To purchase an apartment on a mortgage using maternity capital, you must obtain permission from the Pension Fund, which will confirm the possibility of using the balance to repay the loan. Today it is possible to register electronically for services, which allows applicants to save time and plan a visit.

The list of documents for obtaining the opportunity to spend family capital includes the following papers:

- passport;

- SNILS;

- birth documents of children;

- marriage certificate;

- a copy of the loan agreement;

- contract of sale;

- notarized document on the allocation of a share;

- extract from the Unified State Register of Real Estate.

One of the mandatory conditions is confirmation of the parents’ intentions to allocate a share of ownership to each family member. The document is in writing and notarized. The size of ownership for each owner is determined individually, but, according to current recommendations, its total value should be approximately equal to maternal capital.

Pension Fund employees will consider the application within 30 days, after which the organization will send a notification of the decision. It may consist of approval or refusal of the possibility of using funds to repay a mortgage loan. The method of receipt depends on the option of submitting documents, which today includes contacting a branch of the Pension Fund, MFC, or using the capabilities of your personal account.

It might be interesting!

Mortgage and child’s share: how to allocate and arrange

Required documents

In order to receive a certificate for maternity capital, you need to submit to the Pension Fund:

- Passport of the owner – applicant;

- SNILS card;

- Certificate of registration with the Federal Tax Service at the place of residence (TIN);

- Certificates of marriage or divorce;

- Birth certificates of all children;

- A certificate from the house management about the number of family members;

- The obligation of the certificate owner, certified by a notary, to register all children in the mortgaged housing after the repayment of maternity capital.

In addition, a birth certificate must be presented. Pension Fund employees will review the application within a month; if the issue is resolved positively, the certificate can be received by the owner who presents the passport.

Then an application is written to transfer funds to pay off the mortgage.

The following must be attached to this application:

- Passport of the main mortgage borrower;

- If the owner of the capital and the borrower are not the same person, then a marriage certificate;

- Mortgage loan agreement with all annexes, including payment schedule;

- Title documents for housing (since March 2017, certificates have not been issued; the rights of owners are confirmed by an extract from the Unified State Register of Real Estate Rights);

- Bank details for transfer of maternity capital.

Sample application

An application for the use of maternal capital is drawn up as follows:

- The owner's full name is indicated;

- The status is indicated - (mother, father, child);

- The fields for date of birth and SNILS certificate are filled in;

- The details of the certificate are entered: series, number, full name of the PFR unit, date of issue;

- The fields on passport data, place of residence, date of birth or adoption of children are filled in;

- If a document is drawn up by a representative, the necessary information about it is indicated;

- Next, you need to indicate the amount to be transferred, emphasize whether the mortgage will be repaid in full or in part, and note the purpose of using the maternity capital funds.

- Then you need to put signatures in several columns to confirm the absence of a criminal record, cancellation of adoption, court decisions on deprivation, restriction of parental rights, or removal of a child.

- The final stage of filling out will be confirmation of familiarization with the rules for sending maternity capital, the rules for refusing to send funds, as well as the authenticity of the application data, with a handwritten signature.

you can follow the link:

Reviews from existing borrowers

There are a large number of banks on the financial services market today, which include offers with the participation of maternity capital. A significant portion of Russian citizens prefer to apply for a mortgage loan to the leaders, which traditionally include Sberbank and VTB.

The advantages of this choice are:

- reliability and security of the transaction;

- absence of “pitfalls”;

- transparency of contractual terms;

- favorable interest rates.

Clients recommend paying attention to the possibility of reducing rates and offers from developers. Participants in salary projects and employees of bank partners receive the most favorable conditions.

Additional benefits in the form of a reduction in the standard rate can be obtained using the following options:

- conclusion of a personal insurance contract;

- using the option of remote document submission;

- engaging a secure payment service.

Some banks are ready to reduce rates for certain categories of citizens, so before applying, it is recommended to find out about the availability of such opportunities. Belonging to the category of young families or “reliable” clients will be an advantage.

Current borrowers note that the procedure for using maternity capital within the framework of mortgage lending today is quite transparent and understandable. To reduce the risk of refusal and to be able to choose from a larger number of offers, it is recommended to submit several applications to different banks, and as a result give preference to the most profitable option.

When purchasing housing on the secondary market, it is recommended to warn sellers in advance about plans to use borrowed funds and a certificate. Some owners are not ready to cooperate on such terms, and an unexpected failure of the deal can result in a loss of time and the expiration of the permitting documents.

Repaying a housing loan

Repaying a mortgage using maternity capital at Sberbank is the most profitable investment of a budget subsidy. Parents can sign a contract without waiting 3 years after the birth of the child. According to the law, funds can be cashed out before the expiration of this period only for housing loans: as an initial payment or final payments.

You might be interested in:

Conditions of a loan for capital

You need to contact the Pension Fund with an application for disposal of money no later than six months after the loan is issued.

Conditions for purchasing new housing

Another condition is registration of shared ownership of the apartment by all family members.

The borrower needs to know that if there is child capital, when repaying a mortgage with Sberbank, according to the condition, the client receives the right to a tax deduction. It is 13% of the loan repaid. To receive a deduction, you must visit the tax office and collect the necessary documents:

- statement,

- declaration 3-NDFL;

- certificate 2-NDFL

- a certificate confirming the costs of purchasing housing.

How to calculate payment

Today, the website of almost every credit institution contains tools that allow you to quickly calculate the basic parameters of a loan.

The following criteria are decisive for the calculation:

- type of real estate;

- duration of lending;

- amount of borrowed funds;

- belonging to a preferential category;

- availability of fees and commissions.

When analyzing calculations and assessing your own financial capabilities, it is worth considering that the schedule data is preliminary, therefore the exact figures of monthly payments are clarified when signing the contract.

Potential borrowers should carefully study the contents of the document, since the terms of standard agreements of some banks require the withholding of fees for processing and servicing a loan, fees for transferring funds and carrying out other transactions.

It might be interesting!

Is it possible to get a mortgage while on maternity leave and in which banks?

How to repay a loan

Repaying a loan with maternity capital involves targeted spending of funds, that is, money is allocated for the purchase of a specific type of real estate. Not all objects meet the bank’s requirements, so it is recommended that you familiarize yourself with the terms of the program in advance. The contract always specifies a repayment scheme, which in most cases involves an annuity method of calculation, that is, making payments monthly in equal amounts throughout the entire term of the loan.

Maternity capital funds require the following features:

- Intended use, with the possibility of repaying the down payment, interest or principal of the loan;

- Cashless payments;

- Transfer of funds from a special account.

A potential borrower must take into account a number of nuances regarding the payment of the down payment and accrued interest. Most credit institutions require a certain portion of the advance to be paid from one’s own savings, since compliance with such requirements indicates the client’s reliability and ability to adhere to financial discipline. It will not be possible to pay off fines for late payments using the certificate, so you should adhere to the approved payment schedule.

State support in the form of allocation of maternity capital funds acts as an additional incentive for many Russian families to decide on the advisability of taking out a mortgage on their home. The procedure for using a subsidy is clearly regulated, and the use of remote document submission and secure payment services greatly simplifies the process of building relationships with regulatory authorities and banks.